If you’re retired (or planning your retirement—which, of course, we all are!), I have great news: You can probably take a lot more out of your nest egg every year than you think.

I’m talking about safely withdrawing 8% or more from your portfolio—without the prospect of living a lot longer than your money does!

We can thank an unlikely wealth generator for this turn of events: AI.

Before you ask, no, I’m not talking about putting a chatbot in charge of your finances! I’m talking about a low-key way the tech is helping retirees (and near-retirees) boost both their investment income and their net worth, leading to that huge 8%+ withdrawal rate we just talked about.

To get at the reason why we can do this, let me take you back a bit over 30 years, to 1994. Back then, financial advisor William Bengen released his landmark study showing that most retirees could safely withdraw 4% of their investments every year without the fear of running out of money in retirement.

But as the years wore on, that number turned out to be far too conservative.

Just ask Bengen himself! He later said that new research led him to recommend a different number: 4.7%. Now he says, “The 4.7% rule is the worst-case scenario … designed for only the most conservative person to use in retirement planning.”

AI: Retirees’ New BFF

Why did 4% become 4.7%? One reason is the stock market’s strong long-term performance.

Remember that Bengen released his study in 1994, when the internet was starting to hit the mainstream. Since then, the internet (along with other technologies it’s spurred) has boosted productivity dramatically.

That’s partly why the S&P 500 has soared since then—and it’s a reason that few investors talk about.

How the AI-Driven Productivity Bonanza Will Boost Your Retirement

The internet’s spread through the economy was slow and uneven. AI, on the other hand, is spurring productivity gains right now.

In the second quarter of 2025, productivity rose 3.3%, after climbing 2.8% in 2024. These are huge numbers, especially when you consider that since the Bureau of Labor Statistics started keeping track in the 1940s, productivity has grown about 2% a year.

If productivity stays this high, we should see stronger growth that boosts stocks and makes higher withdrawal rates easier to maintain. But, income investors that we are, we’re not tapping that boost through an index fund. Instead we’re looking to one of our favorite equity-focused closed-end funds (CEFs).

That’s because, thanks to this CEF’s high yield, our withdrawal rate could very well be zero. We’ll build our retirement on dividends alone while letting our nest egg grow as AI supercharges productivity.

The Ticket to Fast Financial Independence

Consider the Adams Diversified Equity Fund (ADX), as members of my CEF Insider service know, holds large-cap US stocks, with a portfolio consisting of tech high-flyers like NVIDIA (NVDA), Microsoft (MSFT) and Apple (AAPL), as well as other strong performers, such as Bank of America (BAC), AbbVie (ABBV) and Visa (V).

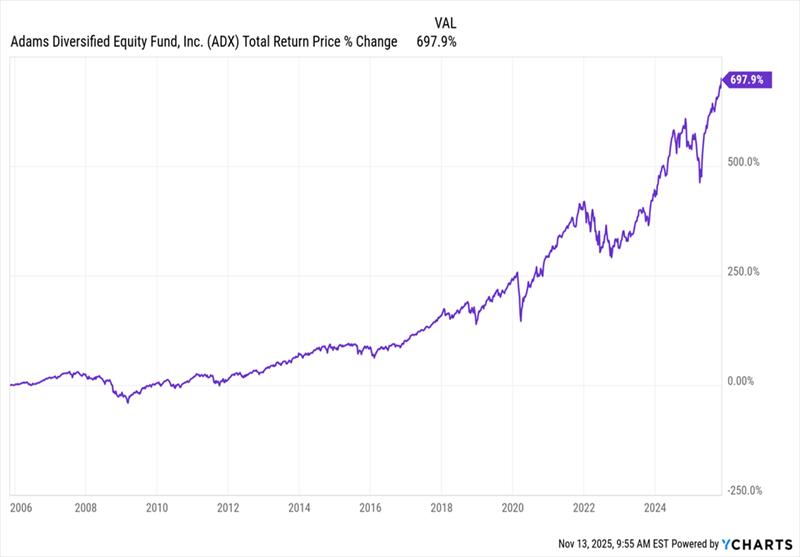

The fund has returned 700% annualized over the last 20 years. That’s pretty close to what the S&P 500 returned, but there’s a twist: ADX has paid a dividend yield that’s regularly been well north of 8% a year, compared to the S&P 500 which only pays in the 1% to 2% range.

This, in theory, could sustain a far higher withdrawal rate than Bengen’s 4.7% withdrawal rate, even after we set aside a healthy cushion for inflation.

One more quick point on that dividend: Over the years, ADX has tied its payout to the performance of its portfolio, and has paid the bulk of its yearly payout as a year-end special dividend. More recently, it has shifted to paying 8% of its underlying portfolio value in quarterly installments, making the payout more predictable, even though it still does shift with the portfolio’s value and market conditions.

That slight fluctuation in the payout is more than worth it for us, as it allows management to reinvest more when it spots bargains in the market. And it’s still provided a monster income stream over time.

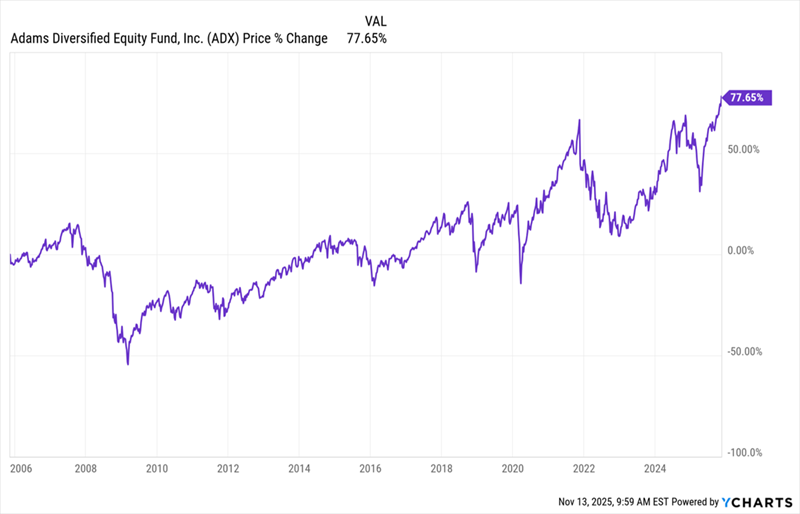

And then there are the price gains. Over the past 20 years, ADX’s price has gained around 78%.

ADX Gains, Even Without Its Dividend Included

In other words, a hypothetical investor who invested 30 years ago not only had a sustainable income stream far ahead of Bengen’s estimates, but they grew their principal the entire time, too!

And unlike, say, an investor holding a low-yielding S&P 500 index fund, they didn’t have to worry about timing their buys and sells. They simply received their dividend payouts every year and used those to pay the bills, while letting their investment quietly grow in the background.

This price-growth-plus-high-income setup is the beauty of CEF investing, and I see it getting even better as AI supercharges productivity in the coming years.

5 “Hidden” Funds (Average Yield: 9.2%) to Buy as AI Ignites the US Economy

In a situation like this, our best play as income investors is to front-run the next big AI gains before they flow out from tech to the rest of the economy. ADX, with its focus on tech and non-tech blue chips, is a good place to start.

Trouble is, the fund is a little over my buy-up-to price now, so it’s not the best option.

But the 5 “Hidden” CEFs I’ll show you right here are much better plays. They hold blue chip stocks, high-yield corporate bonds and shares of companies providing critical infrastructure (including data centers and power-generation facilities) that all stand to gain as AI’s lightning-fast growth continues.

Best of all, these 5 bargain-priced funds pay the kind of dividends that let us retire on our payouts alone: I’m talking about a 9.2% average yield here, with the highest payer of the bunch kicking out a huge 10.9% dividend.