If you have $100,000 to invest, you can easily use it to unleash a dividend stream that pays you $940 a month. That’s $11,280 a year in dividends—on just $100K!

I know you’re probably thinking this sounds too good to be true (and you should be!), especially when 10-year Treasuries dribble out just 0.7%, and the typical S&P 500 stock isn’t much better, with a 1.7% yield.

You’re not retiring on either one of those meager payouts!

But $100,000 invested in a fund with an 11.3% dividend yield (like the one we’ll dive into below) gives you a good start toward clocking out, and on a modest nest egg, too.

The nice thing about this approach is that you’ll still invest in blue chip companies like Mastercard (MA), Deere & Co (DE) and PepsiCo (PEP). That’s the real magic of this strategy: it lets you take low payers like these (PepsiCo is the highest yielder of this trio, at 2.9%) and “squeeze” them for a far bigger payout. Here’s how it works:

Step 1: Open a Brokerage Account

This isn’t really a step for many people—if you’ve read this far, you probably already have a trading account. No matter what kind of account it is, you’re fine to use it (so long as it lets you trade US stocks, of course): there’s nothing exotic about the funds we’re going to target with this strategy. They trade on the major markets, just like stocks.

If you don’t have $100K in your account already, go ahead and transfer it in.

Step 2: Buy a Closed-End Fund

Next, you’ll need to purchase a closed-end fund (CEF). The name we’re targeting today is the Gabelli Equity Trust (GAB). Let’s get into a little more detail on both CEFs in general and GAB in particular.

First, a CEF is like a mutual fund or an exchange-traded fund (ETF), but with some key differences. Unlike mutual funds, whose values are reconciled and unit prices are set after each trading day, CEFs trade during the exchange’s opening hours, just like an ETF or a regular stock.

And unlike ETFs, a CEF has a fixed amount of shares that are established when the fund holds its IPO. While ETFs can, and do, increase their total number of shares outstanding, CEFs do not, which helps keep them small and more manageable. An ETF like the SPDR S&P 500 ETF (SPY) can balloon to have a whopping $278 billion in it, where the biggest CEF has just $4 billion in assets. GAB is much smaller, with $1.3 billion.

GAB is managed by a group of value investors who focus on high-quality, mostly mid-cap and large-cap stocks. This team is headlined by famed value-investing guru (and Warren Buffett disciple) Mario Gabelli. Mario and his team look for companies with reliable cash flow and rising profits, which is why the fund owns Mastercard and PepsiCo.

Unlike ETFs, which usually pay tiny dividends, GAB (like most CEFs) focuses on maximizing dividends to shareholders; it does this by collecting payouts from the companies it holds and rotating assets and occasionally taking profits, which it then gives to shareholders in the form of dividends. That’s one way the fund can sustain a double-digit dividend.

There’s another part to the fund’s strategy, too: a careful use of leverage—by borrowing to invest, Gabelli and his team can enhance their portfolio’s returns, boosting its profits (and your payouts) further. Leverage, of course, also amplifies losses, a risk Gabelli mitigates by targeting companies trading below their intrinsic value and by keeping his leverage manageable—right now, the team has borrowed against roughly 25% of the portfolio.

Leverage is a particularly smart strategy today, with the cost of borrowing essentially at zero.

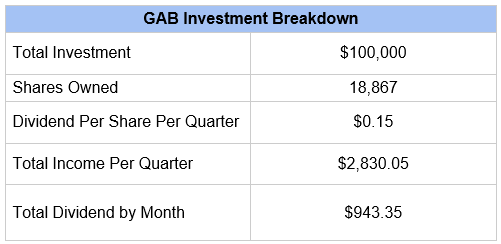

Now let’s take an exploded view of our GAB investment, so we can see exactly what we’ve got on the line here, and how much we’re getting back in dividend cash:

Step 3: Wait Two Months

After we’ve bought our shares, the last part is the easiest: just wait for the checks to roll in.

GAB pays dividends every three months, with the next payout coming sometime around December 14. That means in about two months, an investor who puts $100K in now will have $2,830.05 in time for Christmas.

If you want to set this up as a recurring income stream, all you have to do is set an automatic-payment-transfer from your brokerage account to your bank account for $943.35 every month, and GAB’s dividends will appear in your account—in cash.

4 MORE CEFs That Build Wealth Forever

GAB is a great fund. In fact, it almost made my list of the top CEFs I’d buy and hold forever. The only problem with buying it now is that it trades at a premium to its net asset value (NAV).

That’s another way of saying that the fund’s shares trade for more than its portfolio is really worth. And there’s just no reason to overpay (and cap our upside!) when there are so many bargains in this often-overlooked corner of the market.

This is where the 4 CEFs I have for you today come in. They’re trading at such huge discounts that I’m calling for 20%+ price upside in the next 12 months as these totally bizarre markdowns vanish.

That’s not all, either, because this diversified “4-pack” yields 8.1% today. And those payouts will likely grow as the economy recovers and their managers borrow modestly at today’s ridiculously cheap rates to goose their gains even further.

This upside-and-income combo is what makes CEFs so appealing, especially now. My 4 top buys (average yield: 8.1%!) are waiting for you. Click here and I’ll give you the whole profitable backstory on each of these 4 smartly run funds: names, tickers, complete dividend histories and everything else you need to know.