Contrarians that we are, we know when we hear things that sound like “common wisdom,” we need to look just a little bit deeper.

Today, that’s what we’re going to do, with a common refrain we’re hearing a lot—that tariffs will lead to a spike in interest rates.

Then we’ll look at a bond play that’s set to benefit from this misunderstood mantra. This smartly run fund pays a dividend that yields 10.4% and comes our way monthly, too.

Tariffs Here, Tariffs There …

To be sure, tariffs have arrived. President Trump has imposed a 10% levy on all products China exports to the US (and 15% on liquefied natural gas and certain types of coal), effective last Tuesday.

Canada and Mexico, for their part, secured 30-day reprieves on the 25% tariffs Trump threatened on each of them after striking border-security deals with the administration.

One thing we can be sure of is that more tariffs are coming. Trump has been talking about tariffs since 1989, when he advocated for a 15% to 20% tariff on imports from Japan because of unfair trade practices.

And at the end of last week, Trump said he would impose “reciprocal tariffs” on many nations aimed at matching tariffs they apply to US goods.

So tariffs—and the higher prices on imports they bring—are naturally going to lead to higher inflation here in the US, right? And of course, higher inflation begets higher interest rates.

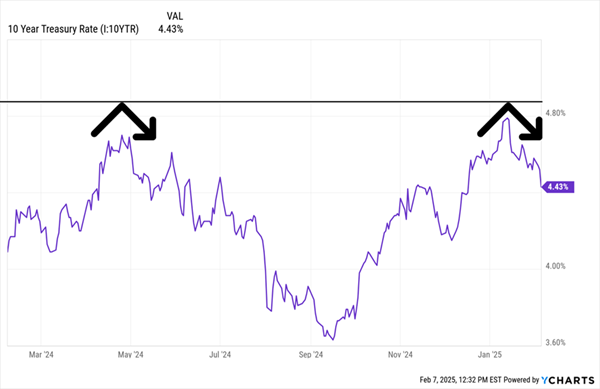

Well, lucky for us, we have a way to gauge that in real time: the movements of the yield on the 10-year Treasury note.

Bond Market Shrugs

If the bond market were worried about tariffs jacking inflation, you’d expect the 10-year Treasury rate—benchmark for the rates businesses and consumers pay for all sorts of loans—to spike. Instead, the opposite has happened.

Just look at the last year, as the possibility of Trump’s re-election gained in probability, then became a reality on November 5:

10-Year Rate Bumps Against the “5% Ceiling” Into (and Since) Election Day

As you can see, each time the 10-year yield gets close to 5%, it hits its head and drops again.

What’s going on here?

Well, contrary to popular belief that these levies are inflationary, a recent study shows otherwise. The Centre for Economic Policy Research found that tariffs do not boost inflation because rising prices depend on a hot economy—and a trade war brings in the opposite, since tariffs are a short-term headwind on growth.

The Financial Times recently reached a similar conclusion. Yes, tariffs compress company margins due to upward wage pressure and higher costs. But these are typically absorbed by the firms—and their shareholders!

All of this sets up a buy window for us in bonds, which are despised now, partly on tariff-driven rate fears. (As rates and bond prices move in opposite directions).

“Despised?” You have our attention, bonds!

Our 2-Part Bond-Buying Strategy (and 1 Ticker to Put It to Work)

When we buy want to boost our bond exposure in my Contrarian Income Report service, we always use a two-part strategy:

- Look below the investment-grade line. This is where the best bargains are, as pensions, for example, aren’t allowed to own this paper. That leaves more room in the bargain aisles for us!

- Buy through closed-end funds (CEFs) so we get most of our return in safe dividend cash, thanks to CEFs’ high yields. We also get our bond holdings managed by an expert (essential in this corner of the market) and the opportunity to get in at a discount.

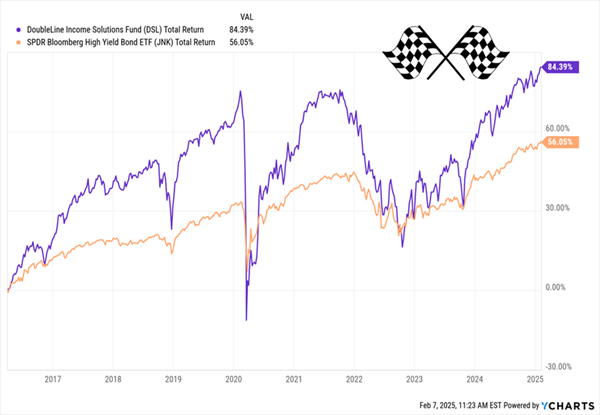

With that in mind, the DoubleLine Income Solutions Fund (DSL) is our contrarian tariff play here. As mentioned, it yields 10.4% and is run by one of the savviest bond minds on the planet—the so-called “Bond God,” Jeffery Gundlach.

DSL’s name might sound familiar to you: It’s a long-time CIR holding, and we looked at DSL’s sister fund, the DoubleLine Yield Opportunities Fund (DLY), in our January 28 Contrarian Outlook article.

Gundlach puts his deep connections to work running DSL and DLY, and the results are hard to argue with. Since we added the fund to our CIR portfolio back in April 2016, it’s returned a tidy 84.4% as of this writing. That was good enough for DSL (in purple below) to smoke the go-to ETF for corporate bonds, the SPDR Bloomberg High Yield Bond ETF (JNK):

DSL Outruns the Bond Benchmark

As you’ve probably guessed by now, DSL does this by investing well outside the investment-grade space, with 75.5% of the portfolio in below-investment-grade bonds. Another 6.2% of its holdings are unrated.

The average duration of these bonds is on the long side: 5.5 years. That means Gundlach has smartly locked in higher-paying bonds, and he (and we) can look forward to those high income streams coming in for years yet, even as rates move lower from here.

He also charts a prudent course on the leverage front, borrowing against about 22% of the portfolio. That’s the “sweet spot”—enough to boost returns while minimizing harm in a downturn. And of course, a move to lower rates (even if it’s not as fast as we thought it would be a few months back) will cut DSL’s already reasonable cost of borrowing.

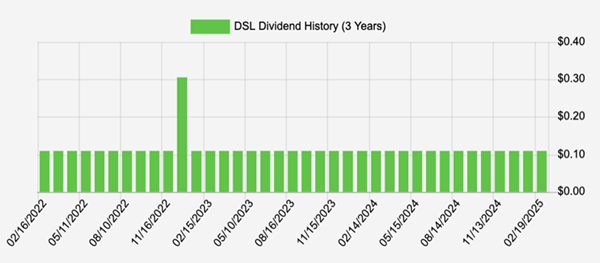

All of this helps sustain that 10.4% dividend, which means we’re getting essentially all of our return in cash here. The fund did trim the monthly payout in 2020 (understandable), but has held it steady since, including through the 2022 nightmare. Gundlach & Co. even threw in a special dividend at the end of that year:

A Reliable 10.4% Dividend? DSL Delivers

Source: Income Calendar

A final word on our buying opportunity here: It may be time-limited. As I write this, DSL isn’t far below my buy-up-to price and trades at a roughly 1% premium to net asset value (NAV). With 10-year Treasury rates contained below 5%, it could pop above that level at any time.

Personal Invite: Your 8%+ Dividend Plan for an Inflation-Rattled Market

I’m Kevin Wallen, Brett’s publisher.

If you’re like me, you’ve been watching the markets daily these last few weeks, to see if the rapid-fire news cycle we’re living through triggers a big selloff.

Maybe you’re close to retirement and simply can’t afford a double-digit drop.

Or maybe you’re in retirement and worried the next selloff could force you to sell at low prices to get the cash you need. That’s a nightmare scenario—stunting your income and your portfolio’s growth potential.

8% Dividends That Pay Monthly, Ease Market Worry

I want to show you how to put an end to worries like these: It comes in the form of a special portfolio Brett has carefully assembled.

It’s his “8% Monthly Dividend Portfolio.” As the name says, it pays you an 8% average yield, with payouts coming your way every month.

That 8% is, more or less, what the stock market returns on average over the long haul. And it’s paid to you in dividends alone!

That monthly payout gives you valuable reassurance, too. After all, no management team would pay monthly if they weren’t sure they could keep doing so.

I’ve put everything you need to know about this unique 8% Monthly Dividend Portfolio right here. I can’t wait to tell you all about it and give you a free Special Report revealing the names and tickers of the stocks and funds inside.