One of our old flames, a former Contrarian Income Portfolio holding, has pulled back sharply in recent weeks. Time to buy the dip in this 4.3% dividend? Let’s discuss.

Kinder Morgan (KMI) is a blue-chip energy payer that boasts 79,000 miles of pipelines, which transport crude oil, carbon dioxide and other products, though chiefly natural gas. In fact, some 40% of natural gas produced in the U.S. flows through Kinder’s systems. It also has 139 terminals that store petroleum products, chemicals, renewables, and more.

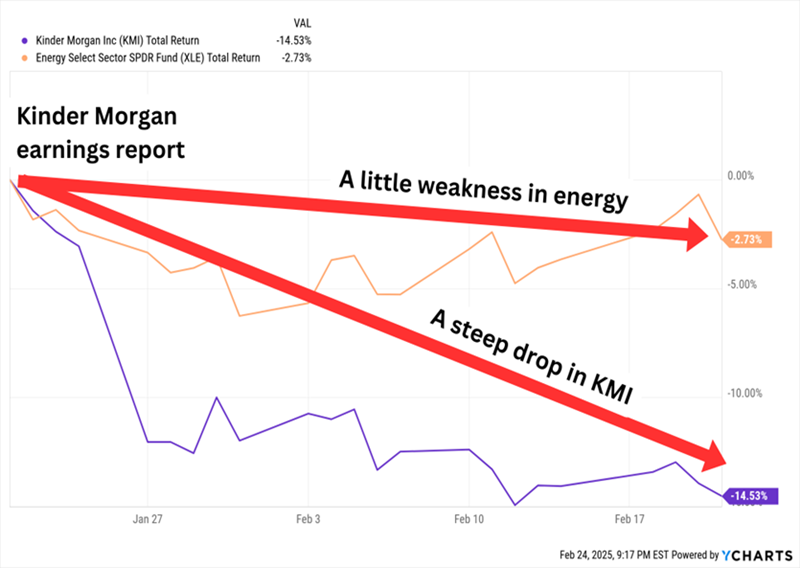

But venerable though it might be, Kinder Morgan is having a rocky start to the year, courtesy of a nearly 15% slide since its Q4 earnings report in January—and this sudden downturn in price has me eyeballing KMI (and a handful of other high-dividend energy names) again.

This Correction Deserves a Little Attention

Why did we jettison KMI from our CIR portfolio back in September 2024? It looked a little hot. My words when we parted ways: “When we sell a stock, it is goodbye for now rather than forever. We may buy KMI back someday on a dip.”

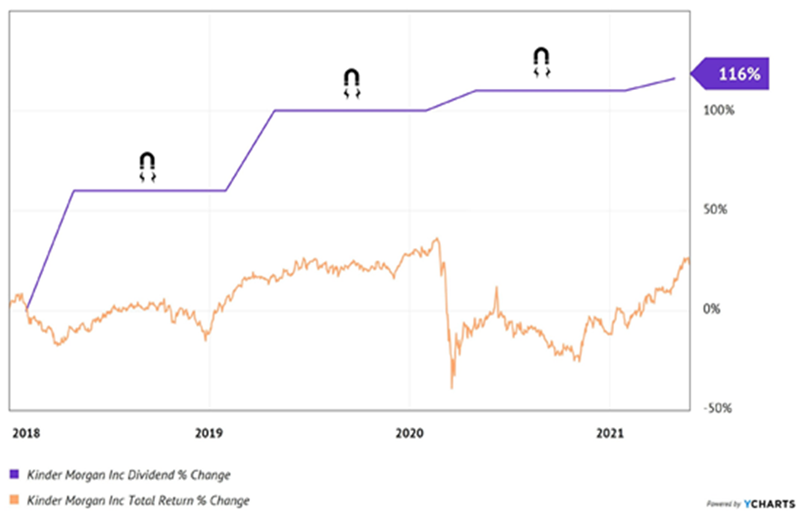

We originally bought Kinder Morgan in the summer of 2021. The energy bull run was just beginning, and the “dividend magnet” was really only starting to pull on shares.

The Original Dividend Magnet Setup for Our KMI Buy

The old Wall Street saying is that bull markets climb walls of worry. KMI was supposedly at risk of a dividend cut. But the math didn’t add up, and at the time, I wrote:

“The firm’s net debt levels are just four times EBITDA. Management’s goal was to work debt down to four-point-five-times EBITDA, so it has already exceeded the plan that was put into place six years ago.”

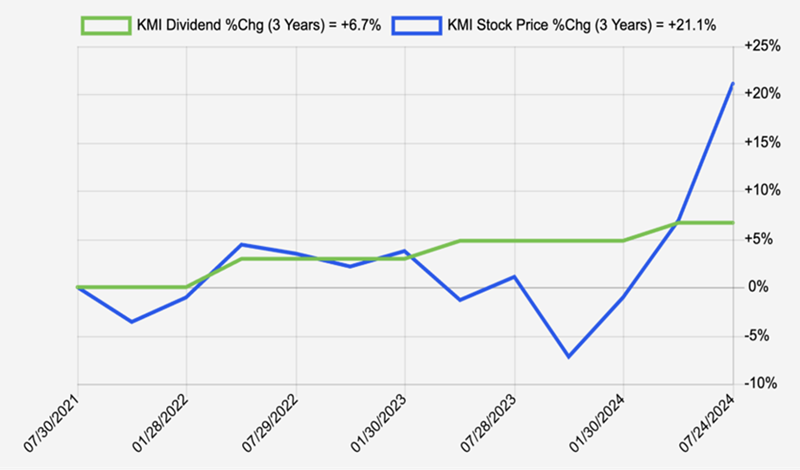

Three dividend hikes and 36% total returns later, we made our exit because KMI’s price was going parabolic:

KMI’s Price Outran Its Payout

With KMI dropping 15% in short order, it’s back on our radar. The drop had less to do with Kinder’s Q4 report (which was a lot more good than bad) and more to do with the fact that KMI shares had roughly doubled for the year heading into it. A small disappointment—in this case, earnings that were up 14% but a penny shy of estimates—was enough to convince a few investors to take some profits.

But there were company updates to like, too:

- Raised 2025 EBITDA and adjusted earnings per share guidance

- A project backlog of $8.1 billion that was 60% higher than Q3 2024

- Anticipates robust demand for natural gas through 2030

- Announced the 216-mile Trident Intrastate Pipeline Project providing roughly 1.5 billion cubic feet per day (Bcf/d) of capacity from Katy, Texas, to an LNG corridor near Port Arthur, Texas.

That project isn’t free, however. Management expects growth capital expenditures over the next three to four years will average about $2.5 billion annually. Which might very well explain why Kinder said it expects to increase its dividend by a (modest) 2% in 2025.

A little dividend growth is better than none, but 2% won’t even keep up with inflation—and it’s slower than I’d like to see given a good-but-hardly great 4.3% yield.

We can do better. And given a host of pricey readings (including a PEG of 2.7 and a forward P/E of 21), it’s likely we can do better on price and yield without any meaningful downturn in Kinder’s business.

Are there similar (but also riper) opportunities in the energy patch?

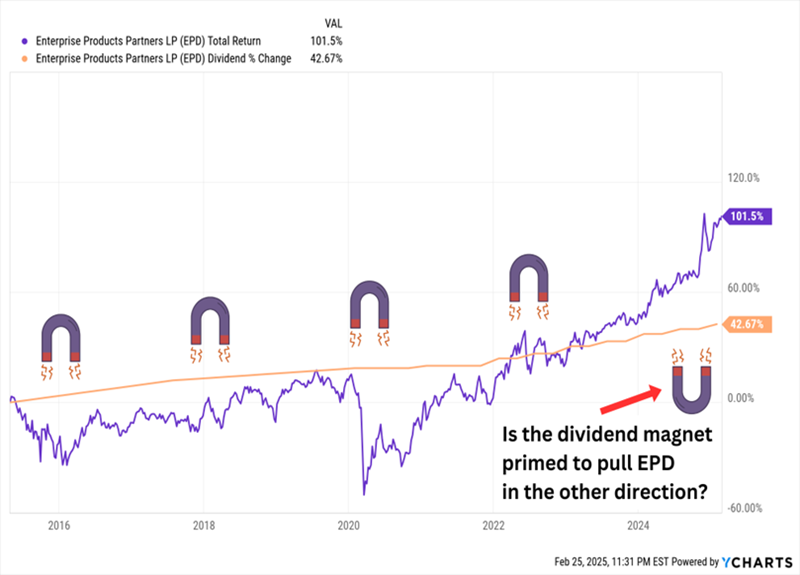

Enterprise Products Partners LP (EPD, 6.4% yield) is one of the bluest energy-infrastructure blue-chips. It has 50,000+ miles of pipeline, 300 million barrels of liquids storage capacity, 26 fractionation facilities, and 20 deepwater docks. It’s one of the most prolific toll-takers out there—and that steady business has enabled it to reach Dividend Aristocrat status, at 27 consecutive years of dividend hikes. One of the most interesting notes from its latest earnings call is that management thinks it can hit $1 billion to $1.1 billion of excess distributable cash flow (DCF) even after fully funding growth capex. That money likely wouldn’t reach the distribution, but would instead be used to retire debt or buy back units—still a good outcome for investors, who already are collecting more than 6% on a well-covered distribution. EPD has lagged some of the better energy MLPs over the past year, but it also trades for just a little more than 9 times DCF, which is at the low end of its valuation.

But the Dividend Magnet Phenomenon Could Become Problematic

Energy Transfer LP (ET, 6.9% yield) is another major infrastructure play, with 107,000 miles of natural gas pipelines and another 14,500 miles of crude oil pipelines, 235 billion cubic feet (bcf) of nat-gas storage capacity, and more than 70 natural gas processing and treating facilities. It’s coming off a slight EBITDA disappointment in its latest earnings report, but it also just announced its first natural gas supply contract made directly with a data center—Texas-based Cloudburst. It’s a promising development that has utilities and midstream companies alike riding the AI wave, but also threatens volatility if Wall Street ever sours on the technology. ET’s distribution history isn’t as illustrious as EPD, and it cut deeply into the payout in 2020. But it’s a quarterly raiser that has hiked its distribution by 63% since the start of 2022. And it also trades at an attractive P/DCF, currently less than 8.

Dividend Growth is Slowing, Though

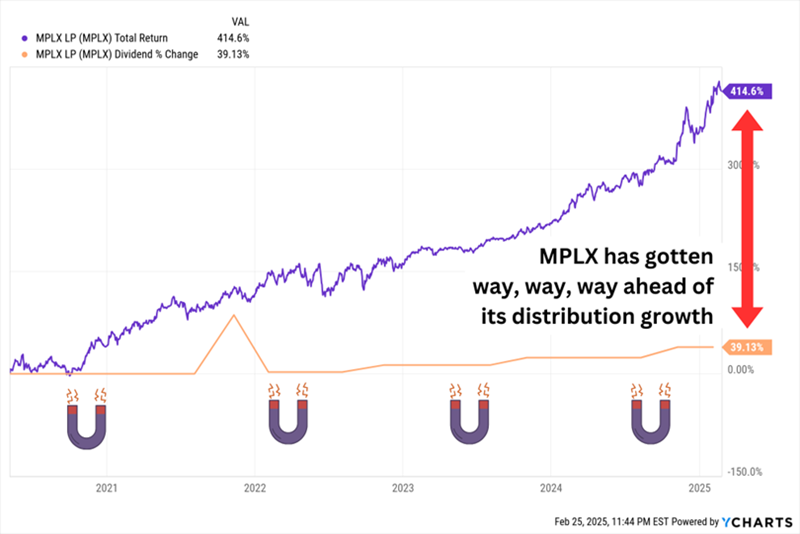

Marathon Petroleum Corporation (MPC) formed MPLX LP (MPLX, 7.2% yield) in 2012 to hold its midstream assets, which are myriad. MPLX has a vast network of assets, including pipelines, refiners, renewable diesel facilities, natural gas processing complexes, asphalt and heavy oil terminals, gathering systems, caverns, marine facilities, and other joint MPC/MPLX assets. MPLX is coming off a good Q4 and announced several new steps in its Permian Basin expansion. MPLX is extremely income-investor-friendly; it yields more than 7% and has increased its distributions by roughly 10% or more over the past three years. Management has outright said the distribution is its preferred method of returning capital, and it expects to continue raising the payout going forward. Despite being one of the hottest MLPs of the past year, and a great start to 2025, it still trades for less than 10 times DCF.

Is This Thing Even On?

Earn 8%+ in Monthly Dividends (Without Angering Your Accountant!)

The tradeoff of those higher yields, compared to KMI, is that they’re MLP distributions. That means these companies will toss you a fussy K-1 form at tax time, which is a hassle for you or the pro who files your taxes. (Trust me, I once got a firm talking-to from my accountant after buying MLPs a few years ago.)

My advice?

Let’s earn a little more yield … with a lot less tax-time drama.

While we’re waiting for Kinder Morgan (and its more traditional dividend) to look more appealing, several of the stocks in my “8%+ Monthly Payer Portfolio” are buy-worthy right now.

Not only do they deliver higher yields than these MLPs, with no K-1 needed, but they also pay us each and every month.

That means when you’re done collecting a regular workplace paycheck, you can quickly transition to collecting a regular portfolio paycheck—one that still syncs up with your monthly bills.

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for all the details, and to download a FREE Special Report revealing the names and tickers of all the stocks and funds in my 8%+ Monthly Payer Portfolio.