Today I want to talk about a corner of the market that has been overlooked for far too long despite offering sustainable high yields of 4% or more—with dividends primed to soar even more.

This sector is a distant cousin to a more familiar group of stocks: utilities. Utility stocks were once Wall Street’s best kept secret: high dividends, cheap valuations, sustainable business models, and steady revenues were all reasons why many big investors quietly bought these small regional companies. Sadly, the cat’s out of the bag. Utility stocks are up nearly 14% year-to-date as investors pile into the sector:

Utilities Gone Haywire

Just look at the performance of the SPDR Utility ETF (XLU), which is up massively even after a recent correction from its shocking 22% year-to-date return earlier this summer. But notice the other line in that chart—that’s the VanEck Vectors Oil Refiners ETF (CRAK), a new and tiny ETF that tracks the oil refineries sector. This ETF is new and tiny for one simple reason: the market has ignored refineries even as it has a love affair with utilities.

Anyone looking to buy stocks now would be wise to ignore the herd and consider getting into the best refineries now and waiting before buying heavily into utility stocks. Let me explain why.

Southern Company (SO) and Duke Energy (DUK) are two particularly popular utility stocks, as their year-to-date performance shows:

A Great Year for Utilities

Of course, the problem with this is that their yields are down significantly:

Less Income for Income-Hungry Investors

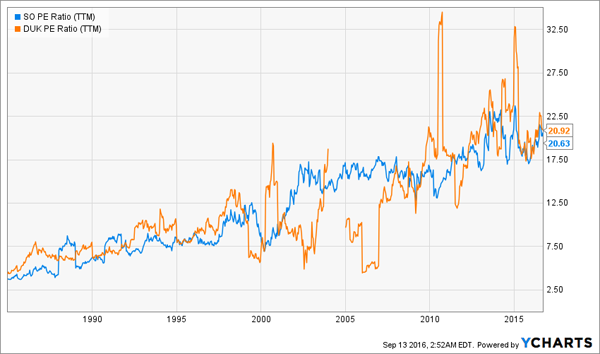

And their P/E ratios are up massively:

Earnings are Pricey

At a smidgen above 20, these utility stocks are massively cheaper than the S&P 500, which has a P/E ratio of about 25. Plus, with yields more than double the S&P 500, investors believe buying utility stocks nets them more income and cheaper earnings.

On the surface, that’s true – but just because something is a relative bargain doesn’t mean it’s actually cheap. We need to dig a bit deeper past this “first-level thinking.” Consider that utility P/E ratios steadily rising for a very long time:

How High Can These P/Es Possibly Go?

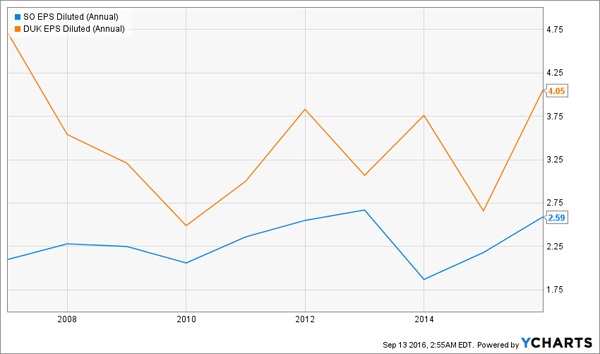

This chart feels like it will keep going up and up, but trends break eventually—and the P/E ratio growth of utilities is set to break soon. Why? Because there’s no earnings growth.

High P/Es But No Profit Growth

There will come a point when investors will realize they are overpaying for utility earnings. There are two trends that could bring us to that point very soon: a massive correction in the S&P 500 could make the P/E ratio of utilities seem relatively high.

Or the falling yields of utility stocks will drop to a point where investors feel they aren’t worth buying for the income, causing demand to dry up and the stocks to crash. In either case, overpaying for earnings is not a wise decision for the long haul.

There’s an alternative that gets us dividends and energy exposure without overpaying: oil refineries. These companies are actually not negatively affected by the fall in oil prices because their input costs decline as their output prices drop.

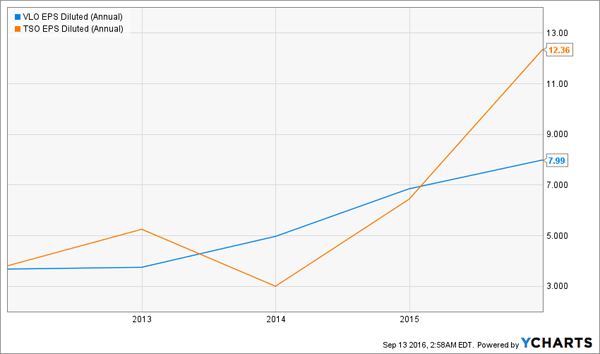

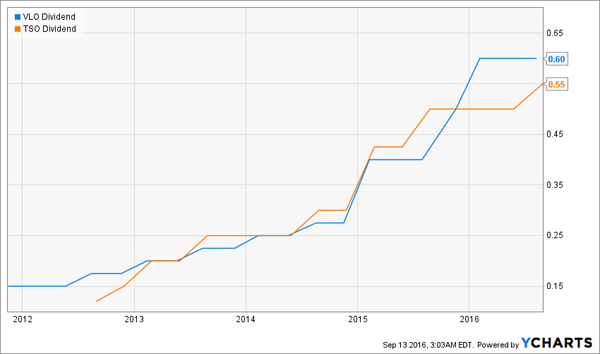

The “spread” is still quite profitable, and the best refineries have shown tremendous earnings and growth. For instance, if we look at the EPS charts for Valero Energy (VLO) and Tesoro (TSO), we see something very different from DUK and SO:

Massive Earnings Growth

Yes, EPS for TSO have almost tripled in the last five years, and VLO has had a decent 150% increase over the same period. But do we have to pay a lot for that big growth?

Hardly.

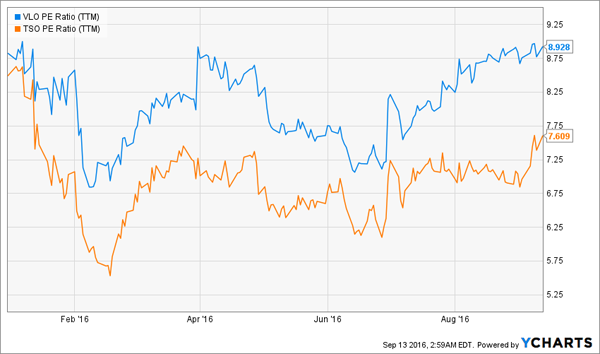

Cheap Earnings

That’s right, P/E ratios for the oil refineries are less than half the utility stocks, and they haven’t been going up this year since the stocks are virtually flat for 2016. We’re getting cheap earnings and we’re timing our buys just right, even in a market that has run up to new heights with more concerns that a correction is around the corner.

What about our income? Admittedly, TSO has a lower yield than most utilities, but its size, earnings growth, and dividend coverage are so good that it’s a great buy even if the income is a bit low. VLO, however, offers dividends on par with the utility sector:

A Good Source of Income

We can also confidently hold these stocks for the long term, since their payouts have been rising for years:

Dividend Increases Mean Raises for Shareholders

With these trends in mind, it makes sense to buy into the best refinery stocks even as many utilities are overpriced.

Does this mean I recommend selling all utilities? Of course not! Some utility stocks are great long-term holds as well, but many are reaching a price point where I think they are too expensive to buy.

Stock selection is the key, and I like one closed-end fund in particular that specializes on infrastructure investments. It buys the companies tasked with maintaining and rebuilding America’s infrastructure – which means they’ll have no shortage of business and profits in the years ahead.

There’s just one problem—it isn’t easy for investors to get their hands on these types of investments. However, the fund I have in mind pays a dividend over 7% and still boasts 10-15% upside.

Want to know more about this ultimate infrastructure investment, and two more favorites of a prominent bond guru? Click here and I’ll share these funds’ massive yields, historical performance, and where you can buy them.