Floating-rate bonds are supposed to be sailing right now.

So why are they sinking?

Last week we lamented the reason most bond funds are down this year. The runaway long rate is to blame.

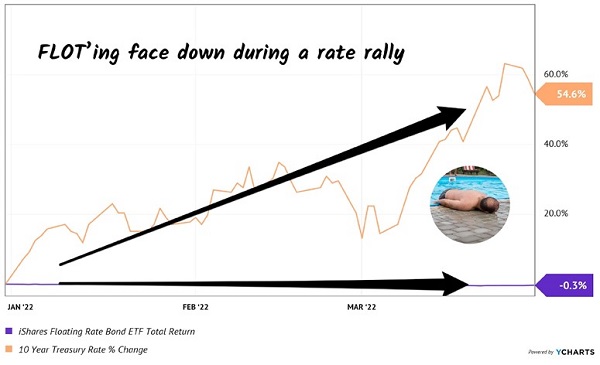

Ten-year Treasury bonds began the year yielding 1.5%. Now, they pay 2.4%, a whopping 60% more in a quarter!

Nobody wants the 1.5% vintage when they can “level up” to 2.4%. So the old 1.5% bonds, while still paying their coupons, lose value.

So do funds that own Treasuries. The iShares 20+ Year Treasury Bond ETF (TLT), one of the most popular bond tickers on the planet, is down 10% year-to-date. Not exactly what retirees are looking for.

Enter floaters. They have variable coupons—interest payments—that are calculated quarterly, or even monthly. Their rates start with a reference rate, such as the federal funds rate and add a defined payout percentage to it. When the reference rate ticks higher, so does the coupon’s payout.

The iShares Floating Rate Bond ETF (FLOT) is the ETF lovers’ alternative to TLT. FLOT buys corporate bonds with floating-rate features.

These bonds aren’t as bulletproof as Treasuries, but they are close, because FLOT only buys investment-grade paper.

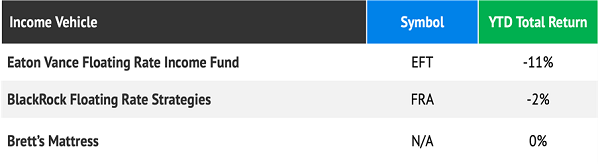

FLOT is doing better than TLT. Unfortunately, FLOT lags the cash stuffed under my mattress year-to-date:

FLOT yields a puny 0.6%. Drop a million dollars into this fund, and we reap just $6,000 in yearly income. Pretty lame for a seven-figure account.

Sure, the FLOT fanboys will point to price upside. But if FLOT’s price can’t float higher under these conditions, when will it rally?

If Not Now, When?

Floating-rate closed-end funds (CEFs) usually beat their comatose ETF counterparts. CEFs benefit from active management. When we let the ETF computers do the fixed-income picking, they lose to my mattress.

My “go to” floating-rate CEFs are Eaton Vance’s Floating Rate Income Fund (EFT) and BlackRock’s Floating Rate Strategies (FRA). Contrarian Income Report subscribers and I have had flings with each during a previous rising rate period.

The yields on EFT and FRA look good today, at 7% and 6.2% respectively. Both funds trade at discounts to their net asset values.

Plus, we like EFT’s manager, Ralph Hinckley. Ralph and his predecessor, Scott Page, have done well in rising rate environments because their loans, on average, reset every 45 days. EFT isn’t stranded when rates rise—Ralph and Scott usually cycle into higher-paying investments.

Time to reconnect with the floating-rate bond boys?

I wish income investing were that easy. Problem is, EFT and FRA aren’t floating either. EFT is down 11% year-to-date, while FRA has shed 2%. Investors who buy these funds for inflation insurance have been disappointed.

We love Ralph but higher rates are coming at him too fast and furious today. He can’t move fast enough.

To paraphrase Western philosopher Peter “Maverick” Mitchell, we feel the need for speed (Top Gun, 1986). We cash-flow focused investors want more than just the inflation insurance promised by floating-rate bonds.

Yes, we want price upside, too.

Inflation-protected payouts? Nah—pour us something stronger. We want inflation-friendly dividends.

I’m talking about yields up to 8.2% per year from my favorite “monthly income funds.” While vanilla investors chase everything from gold to tech shares, they are ignoring corners of the market that can protect us against the coming wave of inflation.

And they can pay us 8.2% dividends while we wait out the financial tempest, too! Let’s get ready for this “50-year retirement storm” and prepare our income portfolio to make some real money from inflation now.