Every time Warren Buffett issues his annual shareholder letter, investors ask:

“Will Berkshire Hathaway (BRK.A, BRK.B) ever pay a dividend?”

Uncle Warren’s answer is always the same: Berkshire shareholders are better served when the company’s immense riches (it ended Q3 with upwards of $66 billion in cash) are plowed back into the business.

Still, you shouldn’t take that to mean the Oracle of Omaha is against putting cash in shareholders’ pockets. He just he prefers another way of doing it: through share buybacks.

But here too, there’s a caveat. To keep from overpaying (a key buyback risk we’ll talk about in a moment), Berkshire will only repurchase its stock when it’s trading below 120% of book value. (Right now, BRK.A is sitting at around 131%, so don’t get too excited about a Berkshire buyback just yet.)

A Rare Win-Win for Investors

Under a buyback, a company purchases and essentially cancels its own stock. This reduces the total number of shares outstanding. And it gives each investor a bigger stake in the company and boosts earnings per share (EPS) because total earnings are divided by fewer shares. Higher EPS, in turn, drive higher share prices.

Dividends, of course, are simply regular payments a company sends out to its shareholders, usually quarterly.

Here’s the good news: both dividend payers and share repurchasers have outperformed the market in the long run, so if you hold companies that do one or the other, you’re already giving yourself a better shot at above-average returns.

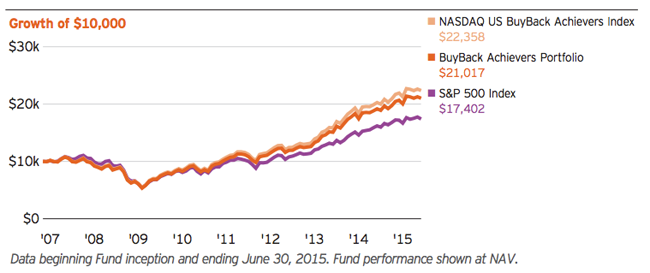

For example, companies that buy back at least 5% of their outstanding shares every year, as tracked by the PowerShares Buyback Achievers Portfolio ETF (PKW), have posted an average total return of 9.5% a year between December 20, 2006, and December 31, 2014, compared to just 7.0% for the S&P 500.

Even “Dumb” Buyback Indexes Outperform the S&P 500

Studies of dividend payers’ performance stretch back a lot further, but the numbers look similar: according to Ned Davis Research, in the 43 years between January 1972 and December 31, 2014, companies that grew their dividends posted a 10.1% average annual return, while those that held their payouts steady returned 7.7%.

One thing you didn’t want to do in that time? Hold a lot of stocks that paid no dividends. They averaged just a 2.6% annual return—barely enough to keep up with inflation.

How a Dividend Fan Learned to Love Buybacks

I’ll be upfront: I love dividend stocks—especially out-of-favor ones throwing off safe yields of 7% and up.

But a high current yield is just a starting point. The key, as the Ned Davis study suggests, is to zero in on companies that also boast a history of large, consistent dividend hikes.

A classic example is Buffett’s investment in the Coca-Cola Company (KO), which he initiated in late 1988 and early 1989, when Coke shares could be had for around $2.80 apiece.

Today, Coke yields around 3.2%, but Buffett is actually yielding more than 45% on his initial stake, thanks to the company’s steady dividend hikes. (Today, Coke pays dividends at an annual rate of $1.32 a share, or about 47% of Buffett’s approximate purchase price.)

Besides the obvious benefit of getting cash in hand, dividends come out ahead for me because they keep management focused, limiting available cash flow and acting as a brake on poorly thought out acquisitions or expansions that don’t make sense.

More important, dividend cuts are the “third rail” of the investment world: touch them and you get zapped. That’s because investors see dividends as a promise, and if a company breaks it, swift punishment—in the form a free-falling share price—will quickly ensue.

Buyback pledges, on the other hand, may quickly fall by the wayside: Whole Foods Market, Inc. (WFM), for example, just added $1 billion to its buyback authorization, bringing its total to $1.3 billion. However, no one will be surprised—or likely even notice—if it doesn’t spend all that cash.

Don’t get me wrong. Just because I’m a big fan of dividends doesn’t mean I don’t think buybacks have a role to play. They absolutely do—and if you zero in on companies that are using them correctly, they can actually amplify your dividend payouts. Here’s how.

A Buyback Afterburner

The key to getting buybacks right is timing. Like any investor, companies should only purchase their shares when they’re a good value. If they’re overpriced, buybacks destroy shareholder value, and management is better off hiking the company’s dividend or investing in the business instead.

Biotech firm Gilead Sciences, Inc. (GILD), which I highlighted a couple weeks ago, offers a good example of a smart buyback plan in action.

In February, Gilead rolled out a $15-billion share-repurchase program to go along with the $3 billion it had remaining on its previous authorization. The company then repurchased $900 million of its shares in Q2 and $3.1 billion worth in Q3.

The move makes sense because Gilead is cheap: right now, it boasts a forward p/e ratio of just 8.9, a nice discount to rivals like Merck & Co., Inc. (MRK) and Abbvie, Inc. (ABBV), at 14.0 and 12.0, respectively. Also in February, Gilead announced its first dividend: $0.43 a share, paid quarterly, for a 1.65% annualized yield.

That buyback could actually boost the company’s dividend payments. Because repurchases cut the number of shares outstanding, Gilead will have fewer shares on which to pay out, leaving a larger slice of the pie for each one.

The bottom line: it pays to look for companies that pay regular—and preferably rising—dividends and buy back shares. But with buybacks, the magic elixir, as Mr. Buffett says, is value.

Remember the Coca-Cola example above, where Buffett is pocketing an unbelievable 47% yield on his initial stake in the company … which he bought 27 years ago?

I’ve just discovered a totally ignored stock that will get you to that type of yield much faster. Right now it throws off a safe 7.3%, and I’m confident its payout will double in 2016.