With the S&P 500’s current yield at just 2%, we have to go beyond the blue chips and search some unpopular sectors to find meaningful dividends.

Sometimes the negative “first-level feelings” on the dogs are justified, and their big payouts are merely yield traps. Other times, we’re rewarded with dividends that are “higher than they should be” thanks to the negative sentiment

Few sectors are as unloved today as energy and natural gas. That’s where I recently uncovered three pipeline plays that are paying high yields that are funded by actual profits.

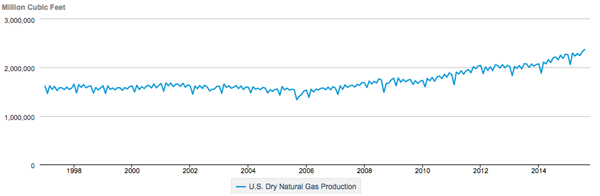

The case against natural gas has been piling up lately. Production is at all-time highs, with the last August EIA report showing a 1.2% increase month-over-month. As a result, stockpiles sit at historic highs. A record 3.9 trillion cubic feet of natural gas – a new record – was reached this summer.

U.S. Natural Gas Production is Still Hitting All-Time Highs…

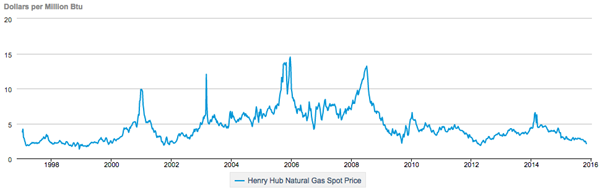

The bull market in “natty” supply has exacerbated the bear market in prices. The current price for natural gas sits at $2.32 – just above the lowest levels since 2002.

… Which Has Prices Near 14-Year Lows

Even the weather seems to be conspiring against natural gas bulls. This year’s El Niño effect – characterized by warmer winter temperatures across the North America – is expected to dampen the need for fuel.

The only positive thing you can really say about much of the natural gas industry right now is that it doesn’t seem like it can get any worse.

Perhaps adding insult to injury, a recent article in the Houston Chronicle suggested that no one expects natural gas to recover for a decade. A first-level investor might read this far and assume that the entire segment of natural gas should be avoided for years. They’d be wrong – and likely late to an “earlier than expected” recovery.

The Natty’s Cure is Here Already

As they say with nearly every commodity, the cure for low prices is low prices. It’ll be no different here with natural gas. The production growth will eventually slow and reverse course.

Drilling for natural gas is a complex endeavor, which is why firms are stubbornly choosing to continue their operations in the face of these record-low prices. They can’t just turn it off like a faucet, because it’ll take significant time and money to fire up again. When low prices finally do impact production, it’s likely to be a multi-year roadblock.

Plus, money managers are currently short a record 230,000 futures contracts. When the natty finally rebounds, these speculators will be in a hurry to cover these trades and “buy back” a long contract. That’s plenty of extra fuel for the rebound.

Three Well Positioned Firms Will Pay You To Wait

Regardless of which producers survive, some distributors are currently in a strong economic position, even today. And believe it or not, they’re profitable AND paying dividends to shareholders.

Atmos Energy Corporation (ATO) stores and transports natural gas across the south and Texas. Its business is split between regulated and unregulated markets. The company recently announced 3Q earnings per share of $0.29. This beat street estimates by $0.02.

Atmos currently pays a $0.42 dividend that yields 2.8%. The company has an impressive record of dividend increases. In just the past 20 years they’ve raised their payouts 16 times.

At $61.09 the stock carries a premium with a current price-to-earnings (P/E) ratio of 19.7 and a forward P/E of 18.7. The average P/E ratio in the sector is closer to 11.9. That’s cheap – an indicator of how depressed the industry is.

AGL Resources Inc. (GAS), like ATO, is a natural gas distributor that also stores and sells to additional outlets. AGL is the largest natural gas-only in the country.

AGL reported adjusted 3Q earnings of $0.25 per share. This beat estimates of $0.20 per share and came despite lower revenues. The stock has a current price-to-earnings (P/E) ratio of 18.3 and a forward P/E of 20.4.

The company pays out a hefty $0.51 dividend yielding 3.3%. After a cut in 2011, the firm has raised its dividend five times.

Earlier this year the firm announced it would merge with Southern Company (SO). The $12 billion merger is expected to create one of the leading U.S. electric and gas utilities. Southern Company brings a portfolio of electricity distribution and public utility companies.

When completed in the second half of 2016, shareholders of GAS will receive $66 per share. It’s almost a 7% premium to the current stock price. (And its parent company SO currently pays a $0.54 dividend that yields 4.8%).

UGI Corp (UGI) is another gas distributor and storage firm that operates a number of segments including utilities direct to consumers. However, UGI also includes operations in Europe and overseas. UGI has a tremendous smokescreen of activity that I believe obscures the stock’s value.

The company owns a 25% interest in AmeriGas Partners (APU). AmeriGas is unique because its sales have dropped by almost 10%, but its gas costs have dropped 50%. And its margins have exploded even as revenue is down. APU currently pays a scorching 9% dividend.

UGI recently completed the purchase of French gas firm Finagaz. Acquisition and integration expenses from that transaction will also take time to settle down. The international footprint and impact of currency exchange has impacted UGI’s revenue as well.

All of these things have distracted investors from a strong gas firm which just issued 2016 earnings per share (EPS) guidance in a range of $2.15 to $2.30 per share. At almost 25% more than the current EPS, it could indicate a potential for a 50% increase in the stock price.

That’s on top of the $0.23 current dividend that yields 2.7%. UGI may be the most convoluted of our three gas plays for the next year, but it probably also has the most potential.

There are higher yielding natural gas plays out there, but you’ll find that many of the highest yielders are such because their stock price is collapsing or their financials are a mess. These three firms – ATO, GAS, and UGI, are all succeeding in this challenging environment. They’re well position for higher payouts and prices pending a turnaround in the energy markets.

I like these as potential income opportunities tomorrow – but if you’re looking for one today, I’ve got a better idea. It’s a backdoor healthcare play that’s helping take care of the aging, retiring baby boomers. The stock pays an incredible 7.5% today, and the company should be increasing that payout annually for years to come.

While natural gas prices are likely to go higher, America is 100% likely to get older. That’s why this is my favorite income play today. Click here and I’ll share the ticker along with the “billionaire’s secret” I used to uncover this opportunity.