Frantic investors are blindly selling the big dividend payers in an all-out “rate hike panic.” But you’ll usually make money buying into panics rather than selling them. And this time it’s no different.

There are high quality stocks that pay yields of 5-6% or better that should be at the top of your watch list. Conventional wisdom says that they’ll perform poorly in a rising rate environment. That’s a lazy blanket statement from “first-level thinkers” that just hasn’t been the case historically.

If you’re a regular reader, you know that I’ve been eyeing Real Estate Investment Trusts (REITs) lately. These are companies that can avoid income taxes by paying out most of their regular earnings to investors. They typically boast high payouts as a result – which has made them a popular option for income-starved investors.

REITs are getting crushed this year, and that’s created some excellent income opportunities. I recently highlighted three REITs that operate in the healthcare sector: Welltower (HCN), Ventas (VTR) and Healthcare Realty Trust (HR).

I like HCN and VTR on pullbacks, as I prefer to buy these issues when their yields are closer to 6%. That doesn’t happen often since these stocks are more commonly in favor than out.

We’re getting that pullback right now, thanks to the increasing likelihood of a Fed rate hike in December (futures traders are now giving it a 70% probability). That’s giving us yields of 5.9% and 5.6% on VTR and HCN respectively. VTR looks particularly attractive – its payout hasn’t been this high since 2009.

But should we be concerned that we’ll lose these yields in price depreciation as rates do rise?

How REITs Really Behave When Rates Rise

Here are the problems that higher interest rates present… according to REIT bears today:

- REITs’ relative yield advantage will shrink as other fixed income investments pay more. This will make them less attractive to investors.

- Their borrowing costs will rise, which is bad for their acquisitions and deal making.

Rather than argue each point with a counterpoint, I turned to the final arbiter – the market itself – to show us what’s likely to actually unfold. And conveniently for us, a similar scenario played out a decade ago.

In June 2004, the original “easy money” Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%.

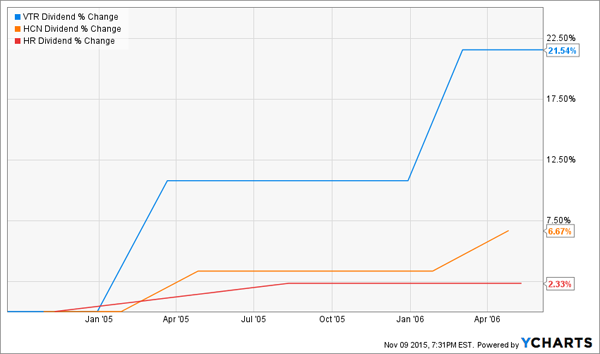

Heading into this time period, VTR was paying 5.8% – about the same as today. Meanwhile HCN was paying a juicy 7.3% and HR was not far behind at 6.8%.

Here’s how these three healthcare REITs fared (along with the Vanguard REIT Index ETF (VNQ) for a comparison with the entire sector):

Some REITs Still Rolled as Rates Rose From 1% to 5.25%

The sector itself (VNQ) did great. So did VTR. But HCN and HR lagged their healthcare counterpart. Why? Because they didn’t increase their dividends nearly as much as during this time span:

VTR’s 21% Dividend Increases Drive 32% Stock Gains

No matter the interest rate environment, income investors want to own stocks that are consistently increasing their dividends by meaningful amounts. I’m not talking about nominal 3-4% increases. I’m looking for gains that’ll double the payout in a decade or less.

That’s exactly what VTR has been able to do for the last 15 years. Its payout is 232% higher today than it was at the start of 2001. HCN has increased its dividend by 41% over the entire period (too slow). And HR’s payout has been slowly chopped in half over time.

The 15-year stock returns mirror this. VTR has returned an amazing 1,320% to investors, while HCN rose 285% and HR just 59%.

The Dividend Drives These Stock Prices

Regardless of Rates, Pick REITs That Grow Payouts

All REITs are on sale today. Those with the potential for dividend growth are tremendous bargains, as they’ve been thrown out with the rest of the sector’s bathwater. And as we saw in 2004-06, it’s likely that REITs as a whole will be just fine.

And the healthcare landlords are my favorite. They’re capitalizing off the biggest demographic shift in American history. Here’s what driving the America-is-getting-older trend:

- There are 77 million Baby Boomers who just started retiring.

- These seniors are living longer than ever – the Society of Actuaries recently amended its mortality tables to give a 65-year-old male a life expectancy to age 86.6 and a 65-year-old woman a life expectancy to age 88.8.

- The 85+ population will triple over the next 30 years.

The longer everyone lives, the more likely it is that they’ll need someone to help take care of them. About 70% of Americans who reach age 65 will need some form of long-term care and for an average of three years.

And while I do like VTR as a way to play this trend, I’m even more excited about a new company in its space that’s actually led by a group of former VTR executives. It’s a direct play on eldercare facilities. The firm pays an amazing 7.5% yield that’s not only safe, but likely to grow significantly with the market in the years ahead.

Get the full details on this “perfect income investment” right now AND the details on how my second-level analysis uncovered it.