Is your nest egg way smaller than a million bucks? Do you worry you’ll never be able to retire?

I know: who doesn’t have this fear, right? Especially in today’s twitchy market.

Good news: you absolutely can leave the grind behind. And probably sooner than you think.

You can do it on far less than a million, too—just $490K (and maybe less than that, depending on your circumstances). The best part: you won’t have to sell a single stock in retirement.

Choose Your Own (Retirement) Adventure

Today I’m going to show you two routes to our $490K retirement: if you’re near (or already in) your golden years, you’ll want option 1: a collection of steady dividend payers yielding 7% and up.

If you’ve got 10 years or more before clocking out, you’ll want to look hard at option 2: a set of dividends growing so fast, your income stream (and trading account) could be up triple digits by the day you turn in your office keys.

Let’s start with option 1: it centers on two different types of high-yield plays (and 4 specific picks) that double (and even triple) the 1.8% payout on the typical S&P 500 stock.

Option 1: Start With Closed-End Funds (2 Picks)

Closed-end funds (CEFs) are perfect for today’s jittery market, for two reasons:

- They pay huge dividends: Many CEFs yield 7% or more, and some even higher—like the 9.2%-payer my colleague Michael Foster, the “CEF professor,” recommended last week.

- They’re cheap: Around 80% of the 500 or so CEFs out there trade at a discount to net asset value (NAV, or what their portfolios are actually worth).

Besides serious upside, CEFs’ discounts give us something critical if we see a 2008 repeat: downside protection. After all, it’s tough for these funds to get much cheaper if they’re already cheap in today’s nosebleed market!

To see what I mean, check out the deals on these two high-yield CEFs:

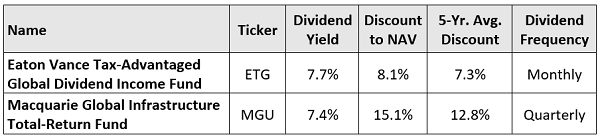

First, ETG: even though the fund has “global” in its name, it holds 59% of its assets here in the US, and its top holdings are dominated by tech and utility stocks like Alphabet (GOOGL), American Tower (AMT) and NextEra Energy (NEE).

MGU, for its part, focuses on utilities and pipelines, with top holdings like Kinder Morgan (KMI), American Electric Power (AEP), Britain’s National Grid plc (NGGTF) and Enbridge (ENB).

Besides their deep discounts and high yields, we want to pick up these two funds for another reason: their huge discounts fuel their outsized dividend payouts.

Let me explain.

When it comes to safe CEF dividends, we really only care about the yield on NAV (or the dividend divided into the per-share value of the fund’s portfolio). And because these funds’ market prices are well below their NAV, this yield on NAV figure is much lower than each fund’s yield on market price.

The bottom line: this makes it a lot easier for management to cover the dividend through gains and income on its portfolio than you might think.

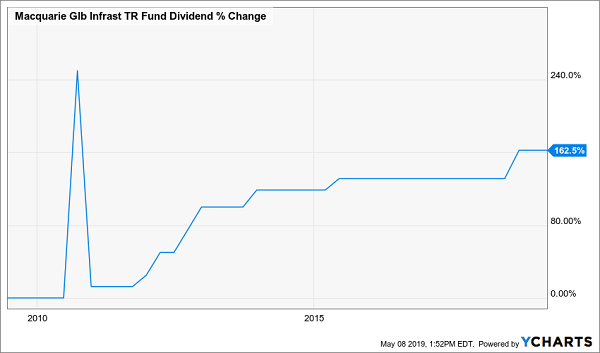

ETG, for example, has a yield on NAV of just 7.1%, considerably less than its 7.7% yield on market price. MGU’s yield on NAV is even lower, at just 6.5%. No wonder this “unicorn” has raised its payout 163% in the last decade (not including a special dividend in late 2010):

MGU: A 7.7% Yield and Payout Growth in One Buy

Next, Move on to High-Yield REITs (2 Picks)

Now that we’ve got two diversified CEFs, let’s add real estate investment trusts (REITs). These landlords—owners of everything from senior-care centers to cell phone towers—are required by law to pay us 90% of their profits as dividends.

The result? Big dividends! And we’re going to tap those payouts in two ways:

- A stout healthcare REIT yielding 5.2% (but primed to hand us a much bigger payout in the next few years) and …

- A REIT-owning fund throwing off an outsized 7.3% payout today.

First up, Ventas (VTR), a nursing-home operator that’s lagged its REIT cousins this year. That’s set us up to grab its 5.2% dividend for a bargain 15-times funds from operations (FFO, a better measure of REIT performance than earnings per share).

VTR: Still a Bargain

A 5.2% dividend may not sound like much compared to the 7%+ payouts on the two CEFs we just discussed, but there are two things you need to know here:

- The payout is safe, accounting for a reasonable (for a REIT) 79% of normalized FFO.

- The dividend is growing, up 55% in the last decade.

In other words, if you’d bought 10 years back, you’d be yielding an outsized 15.5% on your original investment today, thanks to that growing payout!

And with VTR’s low payout ratio and “megatrend” growth potential—thanks to millions of aging baby boomers—I expect the yield on a buy made today to take another big step up well before the next decade passes.

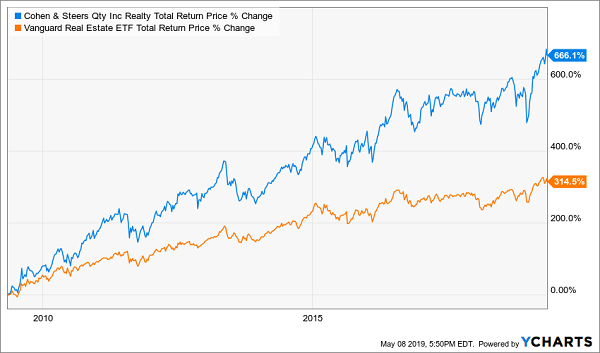

But if you don’t want to wait around for a high REIT yield, I’ve got you covered there, too, with the Cohen & Steers Quality Income Realty Fund (RQI), a REIT CEF I spotlighted three weeks ago.

This “all-in-one” REIT buy, which holds top-notch trusts like apartment landlord Essex Property Trust (ESS), data-center operator Equinix (EQIX) and cell-tower owner Crown Castle (CCI), boasts a gaudy 7.3% yield today.

This little-known high yielder has also crushed its benchmark since the Great Recession:

A REIT Fund That Soars Like a Tech Stock

The kicker? Despite its outperformance, you can still pick up RQI at a 5% discount to NAV—a great deal for a fund that traded near par as recently as April 2018.

Option 2: Go for Dividend Growth (1 Pick)

Now let’s talk about the strategy you should lean toward if you’re more than 10 years out from retirement—or if you just want to grow your nest egg fast, no matter how old you are.

In either case, stocks growing their payouts quickly—way faster than Ventas—are the ticket. That’s because a rising dividend not only increases the yield on your original buy (as we saw with Ventas), but also acts like a magnet on the share price.

I’ve seen it happen over and over again!

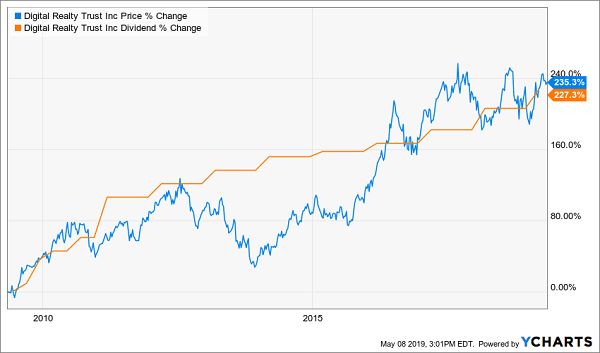

Like with Digital Realty Trust (DLR), a data-center REIT yielding 3.6% as I write. Check out how the trust’s payout has paced its stock higher, almost beat for beat, in the last decade:

Where the Dividend Goes …

With the payout eating up just 63% of FFO in the past year, we can expect more dividend hikes from this “digital landlord,” which counts reliable tech and telecom players like IBM (IBM), Oracle (ORCL) and Verizon (VZ) as clients.

To give you a sense of what that could look like in dollars and cents, let’s conservatively say the payout grows only half as fast in the next 10 years as it did in the last 10. That would still be enough to lift the stock triple digits (around 130%)—and hand you an 8.6% yield on a buy made today.

About That $490K Retirement …

Let’s swing back to that $490K figure I mentioned off the top. How much income would that get us, with a collection of investments like these?

To get the answer, let’s use the average yield on the five stocks in both our options above, which comes out to 6.2%. At that rate, you’d be pulling in about $30,000 in income on your $490K nest egg.

That’s not bad—especially when you consider the strong payout growth you’d likely see from MGU, VTR and DLR. But you’d likely still need another source of income: like a pension, say, or a part-time job. Or maybe a rental property.

We can do better.

Enter the 8% “No-Withdrawal” Retirement Portfolio

To get you over the income hump, I’ve developed my 8% “No-Withdrawal” retirement portfolio.

As the name suggests, it’s set up to let you retire on dividends alone—without having to sell a single stock in retirement.

That’s critical, because if you rely on selling stocks to supplement your income, it’s only a matter of time before you’ll have to sell into a downturn, which seriously stunts your future upside (and your income.)

With an 8% average yield, you can expect your $490K to bring in a lot more: around $40,000 a year—easily enough for many folks to retire on.

And like the income plays we just discussed, the stocks in this portfolio (mainly REITs, CEFs and preferred-stock funds) trade at wide discounts to NAV and FFO, making now a great time to buy.