Plenty of investors see telecom stocks like AT&T Corp. (T) and Verizon Communications (VZ) as cornerstones of any income portfolio. Heck, many even like Comcast (CMCSA) as a dividend-growth staple.

But do they really deserve that honor? And if so, which stock is best for you?

Below, we’ll zero in on a few crucial numbers that tell the tale.

But first, I should point out that none of these three tops my list of favorite dividend-payers now. That title goes to a company throwing off a safe 7.3% dividend yield I’ll tell you about a little further on.

That said, in a head-to-head matchup between AT&T and Verizon, I do have a clear favorite. Let’s start at the top—with dividend yields—and work our way out from there.

Beyond the Dividend Yield

Both telecoms offer healthy yields (5.6% for AT&T vs. 5.0% for Verizon), but Verizon has hiked its payout more quickly than AT&T since 2008, at an average of 4.5% annually vs. 2.8%.

Many first-level investors stop their analysis right here, but that’s a mistake, because even though both companies have long histories of paying—and raising—their dividends, that doesn’t mean they’re safe from a cut. And even the hint of one would send their share prices into free fall.

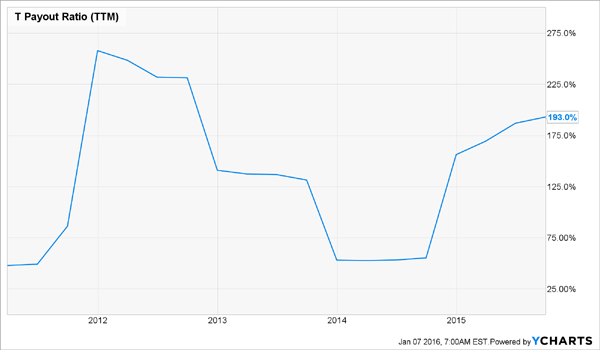

For maximum safety, we need to dig deeper, starting with the payout ratio, or the percentage of earnings paid out as dividends—and that’s where I worry about AT&T investors the most.

As of the end of Q3, AT&T’s payout ratio stood at a whopping 193.0%. In other words, the company was shoveling nearly twice its earnings out the door just to cover its dividend.

AT&T Gives Investors Money It Doesn’t Have

Worse, AT&T has paid out more in dividends than it’s made in profits for three of the past four years. And yet, every year since 2008, management has raised the payout by a penny, just to keep its growth streak—and its coveted spot on the “Dividend Aristocrats” list—intact.

Verizon, on the other hand, has an 83.1% payout ratio. That’s still well outside my comfort zone (I demand 50% or less in the stocks I recommend), but it’s less than half of AT&T’s, and the company’s profits do fully cover its payout.

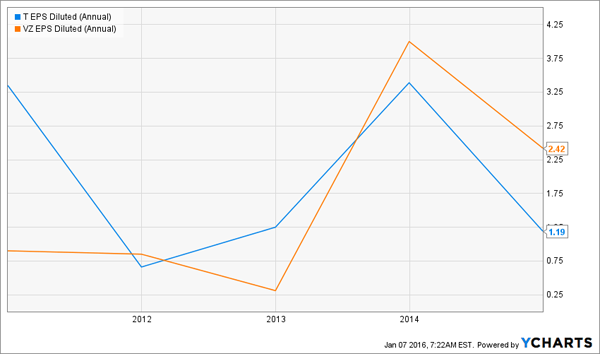

Earnings Growth

If management isn’t willing to cut the dividend to bring its payout ratio in line, the other option is to grow earnings. Here, too, Verizon has had an edge, increasing its earnings per share (EPS) by 41% from 2009 through 2014. AT&T’s results were the opposite of that: a 42% drop.

Opposite Telecom Profit Trends

However, AT&T looks like it could see stronger growth this year, as satellite TV provider DirecTV, which it snapped up for $49 billion last June, starts contributing to its top and bottom lines. The Street is calling for adjusted EPS of $2.81 for 2016, up 4% from an expected $2.70 in 2015. Sales could leap 14.2%, to $169.3 billion.

Verizon, meanwhile, is expected to see meager growth: adjusted EPS of $3.99, compared to $3.98 in 2015, while sales could edge up 0.3%, to $131.9 billion.

If I Had to Pick One…

In the end, these are similar companies with similar prospects, and the market sees it that way, too, valuing both at around 11 times their forecast profits in the next 12 months.

But even so, I still see VZ as the better choice, thanks mainly to its better dividend coverage. It also has lots of smaller, but no less important, advantages.

Its wireless business, for example, boasts stronger customer loyalty than AT&T, with a churn rate (or the number of contract clients who cancel) of 0.93%, vs. 1.16%. That makes it a tougher target for low-cost competitors like T-Mobile US (TMUS) and Sprint Corp. (S).

Its fiber optic TV service, FiOS, is also stickier than AT&T’s offerings, adding 125,000 subscribers through the first nine months of 2015, including 42,000 in Q3. This in a quarter when America’s 13 biggest pay TV providers lost a total of 190,000 clients.

Meantime, DirecTV lost 100,000 subscribers in the US in the second quarter, its last as a separate company. It tacked on 26,000 in Q3, but that was more than offset by the 91,000 AT&T’s U-verse TV service lost as it shifted its focus to DirecTV.

Who Else Wants a Safe 7.3% Dividend Yield?

Now back to that stock I mentioned off the top—the one that’s easily my top pick now.

It really does yield 7.3%, and it’s got plenty of upside ahead, too. More, to be frank, than Verizon or so-called “Dividend Aristocrats” like AT&T. That’s because it’s cashing in on the biggest demographic shift in our history.

With 10,000 baby boomers turning 65 every single day, and people living longer than ever, there is, quite simply, a bull market unfolding that will run for the next two or three decades.

That’s why I like this company so much: it invests in skilled nursing and post-acute facilities. Business is booming, and it’s all but guaranteed to keep thriving in the years ahead. Rising cash flows will power healthy annual dividend increases (I’m talking 5% or 6% annual increases, at a minimum).

Just imagine what that could mean for your own retirement.

So why isn’t it the talk of Wall Street? Because it’s a recent spinoff, so few brokers cover it. But that won’t last long. One major firm just initiated coverage, so it’s only a matter of time before the herd takes notice and rushes in to tap its unshakable 7.3% payout.

That’s why I urge you to lock in this juicy dividend now, while the stock is still cheap. Get the name of this stock and my exact buy advice here.