Dividend darling Kinder Morgan (KMI) just reminded us why we need to know what’s funding that payout we love receiving every quarter.

KMI investors who didn’t see the dividend cut coming were flying blissfully blind. Everyone else, meanwhile, saw the business problems from a mile away. They sold the stock down 58% in the six months prior to the actual announcement…

This is the problem with “first-level” income investing. We can’t just buy a stated dividend and trust that it will be there next quarter. Instead, we must employ more nuanced second-level thinking to look beyond the obvious. This way, we can buy bargains the market is missing… and avoid time bombs like KMI.

I’ve got some high yielding bargains that I’ll share with you in a bit. Investors have mistakenly sold some high quality, growing payers down to levels that we can take advantage of.

But first, let’s free up some capital and talk about 10 dividend disasters waiting to happen. If you own any of these stocks, you should sell them right now. And if you hold related issues, take a close look at the underlying business fundamentals – because there are macro-factors that are undermining entire sectors.

Such as $35 oil…

4 Energy Traps: Oil is Going Sub-$30

In April 2014, I warned that then-$103 crude oil was due for a drop. U.S. crude oil inventories were at 5-year highs, yet money managers were net long 319,000 contracts on crude oil futures. They were betting heavily that prices would continue higher in the face of record supply and stagnant demand.

They were wrong, of course. Then again in September, I warned that big oil remained a big dividend trap. Oil was at $45, and my publisher wondered if I had mistyped my forecast for sub-$30 oil.

But money managers remained net long oil by 110,000 contracts. That was enough fuel to drive crude’s continued crash. We’re 20% lower today, and these contrarian indicators are still net long 79,000 contracts.

Oil’s going below $30 – and it’s going to take down many energy dividend payers with it. Let’s discuss four in particular that are in trouble.

A low payout ratio – the percentage of earnings a company pays out to investors – is generally a good thing. I like to see this below 50%, the lower the better. Until that number turns negative, that is.

The only way to get a negative payout ratio is with negative earnings – in which case, management should be suspending its dividend. But that didn’t happen with BP plc (BP), which lost $2.49 per share over the last 12 months while stubbornly paying out $2.40 in dividends for a big yet unsustainable current yield of 7.8%.

How’d it fill the gap? Almost $5 billion in additional long-term debt.

Meanwhile Chevron (CVX) and Exxon Mobil (XOM) – paying 5% and 3.9% respectively – are, to their credit, making money. But Chevron’s payout ratio has ballooned to 94% over the past year, and Exxon’s has increased to an uncomfortable 61%. Considering that these ratios were below 35% for most of the last decade, income investors should be wary.

Chevron and Exxon Payout Ratios “Go Parabolic”

Chevron CEO John Watson says that paying a dividend is his number one priority. He may be able to achieve this – but it’ll be at the expense of all other business priorities.

Marathon Oil (MRO) wraps up the negative payout ratio club here. The company has lost $0.73 per share over the last 12 months, yet continues to pay an annual dividend of $0.84 per share. Unless oil delivers a surprise rally soon, MRO is racing BP to be the “next Kinder” and cut its 5.5% yield.

Choose Your REITs Wisely

Frantic first-level investors, worried about rising rates, have sold all REITs all year long. I believe they’re dead wrong about healthcare REITs, which currently have sky-high yields and a great track record during previous rising rate environments.

Mortgage REITs, on the other hand, should be sold immediately. If history is any guide, rising rates are not actually priced into share prices of these issues sufficiently. Here’s what I mean…

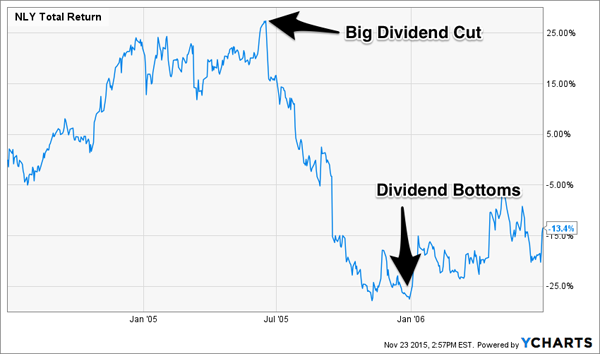

From June 2004 to June 2006, Alan Greenspan boosted rates from 1% to 5.25%. Everyone knew that higher rates would hurt mortgage REITs like Annaly Capital (NLY) because they hold fixed-rate securities that decline in price when rates rise.

However, unlike the forward-looking investors who sold KMI well in advance of its actual dividend cut, they didn’t run for the exits on NLY until after it actually chopped its payout in mid-2005.

Higher Rates Didn’t Hurt Annaly Until After It Cut Its Dividend

If you own Annaly Capital (NLY), American Capital Agency (AGNC), Redwood Trust (RWT), Capstead Mortgage (CMO) or MFA Financial (MFA) for their double-digit yields, you should sell them right now. You don’t want to hold these issues through an actual payout reduction.

And 1 Business Development Company (BDC) to Avoid

Like mortgage REITs, BDCs build and manage portfolios of investments that they hold privately (while their stocks trade publically). They’re also required to distribute most of their income to shareholders, so their yields are often in the double-digits.

As we discussed, not all REITs are created equal, and the same goes for BDCs. One is looking particularly shaky according to the DIVCON screen put together by the income strategy gurus at Reality Shares Advisors.

I interviewed company principals Eric Ervin and Ted Meyer a few months back. They explained to me that according to backtests of their screen, stocks identified as “DIVCON 1” are more likely to cut their payouts than increase them.

Today their screen is flashing red for one BDC: Prospect Capital (PSEC), which yields nearly 17%.

Its down 22% in the last 3 months. And there’s an obvious problem: PSEC’s payout ratio has swelled to 135%, more than double where it was at the start of 2012.

PSEC’s Payout Ratio Swells Beyond 100%

3 REITS That Are Screaming Buys Today

Don’t despair, it’s not all gloom on the income investing beat. As I mentioned, healthcare REITs look good here, and there are three in particular that I really like.

They pay yields of 6.7%, 7.4%, and 7.8% today. And all three companies are increasing earnings and their dividends annually. Anyone who buys today will see a 10%+ yield on their initial capital in just a few years.

This is the best time to buy them, at the height of interest rate panic. Click here and I’ll share the name and ticker from each, along with the unique system that I used to uncover them.