Exchange-traded funds (ETFs) offer “one-click” diversification. Investors buy ETFs to hedge against individual stock collapses.

ETFs can also offer big yields. We’ll look at 11 of them today, with dividends starting at 4% and climbing all the way up to an amazing 21%!

Is the 21%er a trap? Of course it is. But my favorite double-digit payer isn’t – in fact, its 10% payout is secure and spectacular. But this “last safe 10% yield” won’t last long – they never do!

So read on to learn about my best income buy as we round out today’s diversified dividend dozen.

Guggenheim Shipping ETF (SEA)

Dividend Yield: 4%

The Guggenheim Shipping ETF (SEA) invests in a bundle of companies with shipping operations across the world. This group of stocks has been pounded over the past few years as overall global growth continues to slow, reducing demand for the commodities and products SEA’s components ship.

I flagged this ETF the last time I warned investors about dangerous dividends, pointing out its “decimated stocks with many unsustainably large dividends.” Well, SEA’s last dividend payout was just 15 cents – down from 35 cents in the year-ago quarter – and its 4% trailing 12-month yield is now down from almost 15% a year ago. We simply cannot count on this volatile and downtrodden ETF for income over the long run – let’s move on.

Credit Suisse X-LinksTM Multi-Asset High Income ETN (MLTI)

Dividend Yield: 6.1%

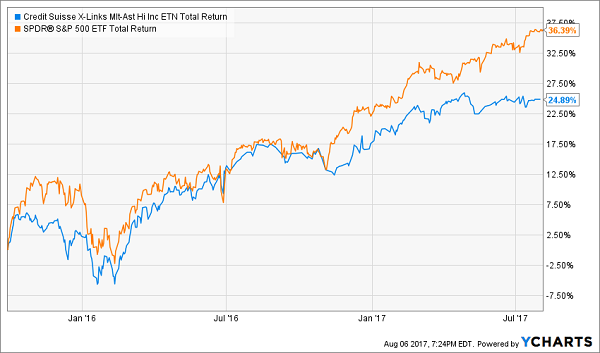

The Credit Suisse X-LinksTM Multi-Asset High Income ETN (MLTI) is one of several “multi-asset” funds that hold a combination of stocks, bonds and other assets rather than honing in on a specific part of the market. MLTI – an exchange-traded note that doesn’t actually hold assets, but instead is a debt instrument that merely provides the returns of its tracking index – is a multi-asset fund meant to generate high income.

It does this via an eight-asset pie, targeting no more than 15% allocation to areas such as emerging-market bonds, real estate investment trusts (REITs) and business development companies (BDCs). However, MLTI has proven a constant underperformer since inception in 2015, with even its 6% dividend unable to help the fund keep pace with the S&P 500 for any significant stretch of time.

MLTI Out-Yields the Market, But Can’t Outdo It

PowerShares CEF Income Composite Portfolio (PCEF)

Dividend Yield: 6.9%

The PowerShares CEF Income Composite Portfolio (PCEF) is a blaring example of over-diversification, investing in a basket of 141 closed-end funds – each of which contains dozens if not hundreds of their own holdings.

While the roughly evenly split mix of bond, high-yield bond and option income funds does provide an attractive yield of 7%, this fund screams of too many cooks in the kitchen, with several laggard CEFs holding back some component gems. To wit, since early 2013, top PCEF holdings such as DoubleLine Income Solutions Fund (DSL) and BlackRock Enhanced Equity Dividend Trust (BSJ) have more than doubled the total returns of PCEF.

Worse, you’re paying an additional 50 basis points of management fees to PowerShares in addition to expenses already taken out of the CEFs’ performance.

Global X SuperIncome Preferred ETF (SPFF)

Dividend Yield: 6.6%

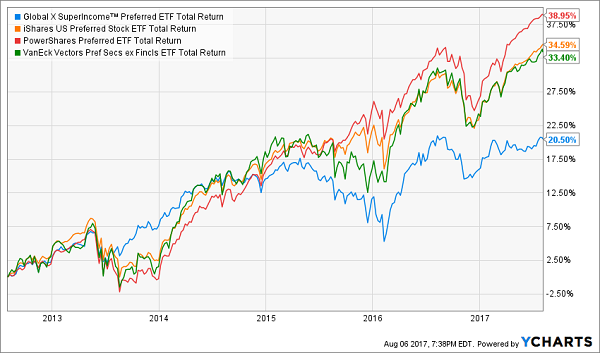

The Global X SuperIncome Preferred ETF (SPFF) isn’t nearly as complicated as the previous two funds – it’s just a preferred stock fund. The SPFF’s goal is to invest in 50 of North America’s highest-yield preferred stocks, and given an ETF yield of 6.6% compared to mid-5% for most of its competitors, SPFF clearly has succeeded.

However, a focus on lower-quality preferreds has dragged on performance since 2012 inception, and it consistently trails funds such as the iShares U.S. Preferred Stock ETF (PFF) and the PowerShares Preferred Portfolio (PGX).

SPFF Doesn’t Have It Where It Counts

Peritus High Yield ETF (HYLD)

Dividend Yield: 6.9%

Peritus High Yield ETF (HYLD) is another example of how a yield chase can lead an ETF into low quality and underperformance.

HYLD is a junk-bond ETF that holds 104 issues – fairly sparse for a bond fund. However, the trouble isn’t lack of diversification, but a dedication to extremely “junky” high-yield debt, with nearly half the fund invested in bonds rated B- or lower.

The headline yield of nearly 7% is much more attractive than the likes of the iShares iBoxx $ High Yield Corporate Bond ETF (HYG, 5%) and SPDR Bloomberg Barclays High Yield Bond ETF (JNK, 5.7%), but the low quality of HYLD’s holdings has overridden any yield benefit, keeping it consistently behind HYG and JNK, not to mention well short of the broader market.

HYLD’s Big Yield Can’t Hide Its Awful Performance

WisdomTree Global ex-U.S. Real Estate Fund (DRW)

Dividend Yield: 7%

WisdomTree Global ex-U.S. Real Estate Fund (DRW) is a basket of roughly 200 real estate-related companies (mostly REITs and development companies) spread across 32 countries, though particularly concentrated in Hong Kong (26%) and Australia (11%).

While international diversification is fine in spirit, there’s a certain detriment to bundling a large group of developed countries that sport little growth, and where a few nations’ growth is often canceled out by lagging performances by other countries. Moreover, leaving out the U.S. real estate market hasn’t exactly been a winning investment thesis for years.

Thus, while a 7% yield is better than many of DRW’s America-centric rivals, its performance largely isn’t.

Gartman Gold/Yen ETF (GYEN)

Dividend Yield: 7.9%

When we last looked at the Gartman Gold/Yen ETF (GYEN) – which creates the effect of buying gold in yen rather than U.S. dollars – it boasted a 7.9% annual yield, and that hasn’t changed, because the fund only pays out one distribution each year that includes dividends and capital gains.

What will this year’s dividend be? Nobody knows. It could yield 8% … but it also could yield 4%, as it has been in previous years. And in addition to a payout you can’t possibly count on for your retirement planning, GYEN has produced half the gains of the more straightforward SPDR Gold Shares (GLD) this year. Yuck.

VanEck Vectors BDC Income ETF (BIZD)

Dividend Yield: 8%

Business development companies (BDCs), which provide financing to small- and mid-sized businesses, are dividend dynamos that can anchor a retirement portfolio. So naturally, income investors might gravitate toward a fund like the VanEck Vectors BDC Income ETF (BIZD), which holds 26 such BDCs and yields a whopping 8%.

But the common theme of quality dilution comes alive again with BIZD, which holds a few stellar BDCs … along with several duds. Consider that since 2013, investments in larger holding Main Street Capital Corporation (MAIN) or smaller, up-and-coming Gladstone Investment Corporation (GAIN) would’ve netted 3x to 4x returns compared to VanEck’s fund.

BIZD: Sometimes It Pays to Stock-Pick

SPDR Dow Jones International Real Estate ETF (RWX)

Dividend Yield: 8.2%

The SPDR Dow Jones International Real Estate ETF (RWX) is similar to WisdomTree’s DRW in that it invests in publicly traded real estate companies in mostly developed (but some emerging) international countries. What’s important to note here is that even a different global composition doesn’t help the international case.

Here, Japan makes up more than a quarter of the fund, with Hong Kong relegated to an 8% holding. Australia is still outsize at nearly 15% of RWX’s assets, but the United Kingdom and France stick out further with double-digit allocations.

Not only is RWX no closer than its U.S.-based counterparts, but its portfolio has looked particularly weak compared to DRW’s in 2017, underperforming 9% to 22%. And you also get to worry about several bubbly-looking international real estate markets to boot.

RWX and DRW Make America Look Great Already

VanEck Vectors Mortgage REIT Income ETF (MORT)

Dividend Yield: 9.4%

Unlike traditional REITs that own and operate properties, mortgage REITs (or mREITs) simply hold on to paper – mortgage-backed securities, commercial mortgage loans and other real estate-related paper.

This has been a difficult industry for the past few years, with several mREITs lowering their distributions over the past 52 weeks. Which is why the VanEck Vectors Mortgage REIT Income ETF (MORT) has sported a lower nominal payout over its past four distributions than the previous four, which were less than the four before that!

Again, I believe you’re better off picking stocks in this space – especially considering an investment in MORT automatically exposes you to significant overweights in a couple large mortgage REITs such as Annaly Capital Management (NLY) and AGNC Investment Corporation (AGNC) anyway.

Credit Suisse X-Links Gold Shares Covered Call ETN (GLDI)

Dividend Yield: 17%

Have you ever heard of covered calls? This popular options strategy involves selling call options on securities you own to generate income during flat and down markets. It’s a phenomenal hedging strategy that makes the most of a bad situation … when done right.

The Credit Suisse X-Links Gold Shares Covered Call ETN (GLDI) does exactly this, going long the GLD and then selling covered calls against it for income. But despite a monster yield that sits in the top 1% of all ETFs, GLDI’s long-term performance essentially is on par with the GLD … and the fund charges you 25 basis points more in expenses for the trouble. Forget this fund.

Infracap MLP ETF (AMZA)

Dividend Yield: 21.4%

The chart below tells you everything you need to know about the Infracap MLP ETF (AMZA) – an exercise in frustration in what already is a frustrating MLP space.

AMZA: How to Make a 21% Dividend Yield Look Ugly

AMZA – which invests in MLP mainstays such as Energy Transfer Partners LP (ETP) and Williams Partners LP (WPZ) – has a boatload of tricks at its disposal. These include the ability to invest in general partners, use leverage and execute a covered call strategy similar to GLDI.

Yet despite all these levers to pull, AMZA not only has been unable to avoid the past few years of pain for MLPs … it has felt the brunt the worst. AMZA has fallen well behind competitors such as the Alerian MLP ETF (AMLP) and the JPMorgan Alerian MLP ETN (AMJ). The final kick to the stomach is a high 0.95% management fee for all that underperformance.

The Last Safe 10% Yield

“Back in the day” it used to be easy for my subscribers and I to make a killing in closed-end funds (CEFs). We had a simple, profitable two-step formula:

- We’d buy a double-digit yield at a big discount, and then

- We’d bank the payout AND upside for safe 40%+ returns!

Yes, we’ve had fun contrarian times since the spring of 2016. That April, we actually purchased “Bond God” Jeffrey Gundlach’s DoubleLine Income Solutions Fund (DSL) for a fat 11% yield at a 7% discount to its net asset value (NAV). Our savvy purchase went on to crush the broader market, delivering 40.5% returns in just 16 months:

Gundlach’s DSL Became Quite Popular

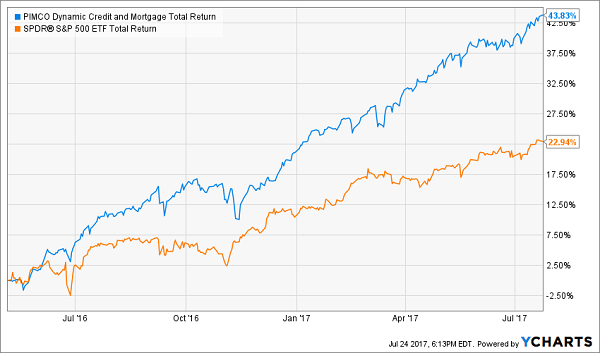

The following month we did it again. We found a 10% payer – issued by the ever-popular PIMCO no less – selling for a 10% discount. And we enjoyed 43.8% total gains from PIMCO’s Dymanic Credit and Mortgage Fund (PCI) in the 15 months to follow:

PIMCO’s Stepchild Fund Gains Favor

Of course these were easy pickings in hindsight. It’s hard to believe now, but the funds were quite out-of-favor at the time. DSL was dogged by its recent underperformance, while PCI carried the baggage of an investment strategy highlighted (and maligned) in The Big Short.

In the last eighteen months, as I mentioned, CEFs have trended back in vogue. Their discounts have narrowed and yields have compressed. But there’s one double-digit yield left, and it’s fittingly the offspring of a recent Bond God favorite.

I recently shared my full research on this “last safe 10% yield” to followers of my No Withdrawal Portfolio. If you want to retire on dividends alone, my research will show you ten safe buys paying an average of 7.5%.

Which means a million dollars invested in these stocks and funds will be safe, diversified – and pay you $75,000 annually without you having to sell a share.

And here’s the kicker: your capital also enjoys 10% upside or better, thanks to the strategy I mentioned earlier.

Are you a current subscriber? If not, why not? We have a 60-day risk-free trial that will let you cancel and get your modest $39 investment back (no questions asked). AND I’ll let you keep all of my research for free.

Which means your downside is zero, and your upside is a secure, prosperous retirement funded by safe 7% to 8%+ dividends. Click here to get started and I’ll explain more about my no withdrawal approach – plus you’ll get the names, tickers and buy prices of my three favorite closed-end funds for yields up to 10%.