You’ve probably been told you can’t have high yields and high growth in the same investment.

If you want growth, the traditional thinking goes, you need to accept little or no dividend income. And if you want high dividends, you can forget about growth.

Today I’m going to show you two investments that turn this outdated thinking on its head. They’re closed-end funds (CEFs) that hold convertible bonds, a powerful asset class most investors ignore.

More on these two funds in a moment.

First, let’s take a quick look at how convertible bonds work, and why so many investors are making a big mistake by not including them in their portfolios.

In a nutshell, they offer the best of stocks and bonds: high income and tremendous growth potential.

Convertible Bonds 101

Like most bonds, convertibles pay out interest at regular intervals. The difference is that holders of convertible bonds can also “convert” their bond into stock in the company that’s issued the bond.

Why would you want to do that?

Let’s say you’re looking at investing in a company with strong cash flow, but you’re uncertain about its growth potential. You don’t want to own the stock, because its value might go down, but you do want to grab a piece of that cash flow.

So you give the company credit by buying a convertible bond. That way, if the company’s growth potential suddenly improves, you can take advantage by swapping your bond for shares.

This switch from being to a creditor to a shareholder is a big plus … but it’s also why most investors avoid convertible bonds: they just don’t have the time to do the research and figure out the optimal moment to make the switch.

That’s where another of my favorite investments, closed-end funds (CEFs), come in.

Run by managers who spend their careers focusing on precisely this question, CEFs that hold convertible bonds can deliver big growth, an outsized income stream and less risk than you’d take on by investing in convertibles yourself.

To show you how, let’s take a look at one of my favorite CEF buys now.

AVK: Growth and Income at a Discount

There are several CEFs that offer diversified portfolios with major convertible bond holdings. Two are selling at big discounts now, despite boasting stellar track records.

The first is the Advent Claymore Convertible & Income Fund (AVK), whose net asset value (NAV) has risen over 5% since inception and whose shares are proven performers in a downturn: after losing 50% in 2008, the fund gained 62% in 2009.

That alone is reason to consider AVK, but there’s much more.

Like the fact that the fund boasts an 8.3% dividend yield on its current market price, which translates into $690 in monthly income for every $100,000 invested.

That high yield is also sustainable, partly because AVK trades at a hefty 15.8% discount to NAV, so it only needs to earn 7.2% in income from its holdings to keep the payout at its current level. That’s only 71 basis points above the average yield on high-yield corporate bonds—a small margin to get from capital gains or leverage.

And since the fund’s assets are 41.2% levered, AVK only needs to get a gross yield of 5% to cover its distributions. A child could do that with dividend-growth stocks, so the fund’s dividend seems extremely safe.

Fortunately, AVK hasn’t had to seek yield by going into junk bonds from companies facing insolvency. Quite the opposite, in fact.

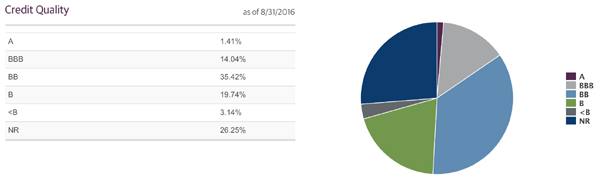

Top-Quality Corporate Bond Holdings

A quarter of its holdings aren’t rated, partly because some of these firms are too small to get the attention of Moody’s and the rest. But as you can see, the vast majority are rated B or above.

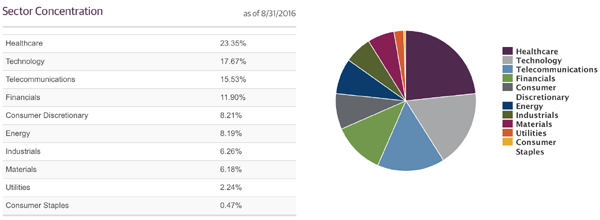

AVK is also well diversified across sectors:

The Entire Economy in One Fund

With healthcare, tech, telecoms and financials at the top, AVK has tapped into sectors where debt can pay high yields, even if the issuing firm has good credit.

Now is also a great time to buy AVK. Despite the market’s swift recovery from its post-Trump panic, the fund is essentially flat year-to-date after a strong performance since February.

A Fire Sale That Won’t Last

However, the fund’s NAV has risen nearly 5% in the same time period. This means you’re getting its assets at a better price now than if you’d bought at the beginning of 2016. That gives us a tremendous buying opportunity that won’t be around for long.

ACV: Buy Before the Secret Gets Out

Which brings me to the second deeply discounted convertible-bond CEF I like now: the AllianzGI Diversified Income & Convertible Fund (ACV).

This fund has gone from trading at a premium last year to trading at a 14.8% discount to NAV right now. That’s one of the biggest discounts in the whole CEF universe! There are three reasons why: ACV is new (its IPO was in 2015); it’s small (with net assets of just $322.8 million); and it’s a CEF, which the market tends to ignore generally.

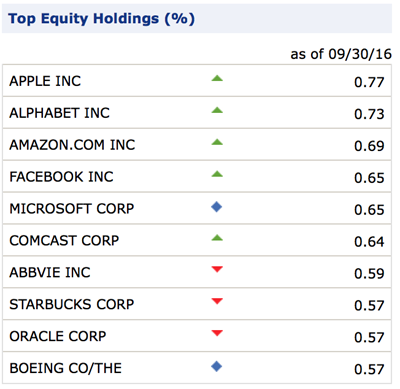

That all adds up to a huge opportunity for us. Not only does ACV pay an 11.5% yield, but it’s well diversified among three asset classes: corporate bonds, convertible bonds and equities. The managers have also stocked it with top-notch companies, as you can see from its top 10 stock holdings:

Familiar, Strong Performers

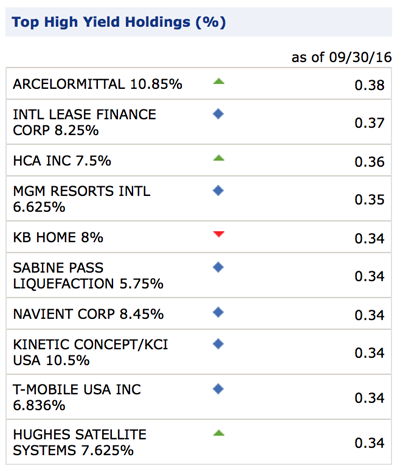

Its corporate bond holdings provide additional diversification and, crucially, do not overlap significantly with its stock portfolio:

A Collection of High-Quality Corporate Bonds

Again, we see several proven, familiar firms, like MGM Resorts (MGM) and KB Home (KBH), and we see the fund’s managers buying bonds with yields between 5.8% and 10.9%.

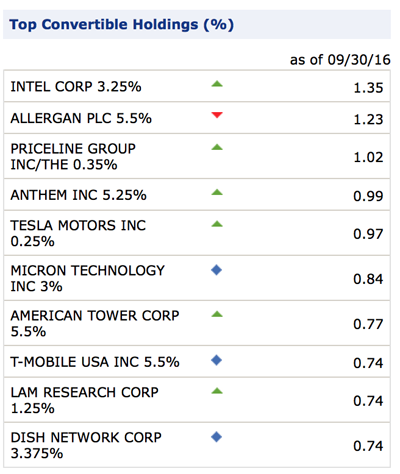

Which brings me to convertible bonds, which make up the largest slice of ACV’s portfolio and are generating even more income for the fund, along with the opportunity for upside if and when it converts these holdings into stocks.

Collecting Income While Waiting for Takeoff

Here we see the fund hedging its risk by extending credit to companies with big potential but stock prices that can swing wildly, such as Tesla (TSLA), Micron Technology (MU) and T-Mobile (TMUS).

For example, Tesla is down 18.8% year-to-date and has swung from being up 10% to being down 40%. Seeing this, ACV’s managers have wisely decided to buy TSLA’s convertible bonds instead of the stock.

Add it all up and you get a fund that defies traditional investor thinking, delivering an 11.5% dividend yield and tremendous growth potential.

You’d think the market would reward that, right? Well, you’d be wrong, because ACV is down nearly 5% year-to-date—a ridiculous situation that’s provided a perfect entry point for us:

ACV: Ready to Buy

A final note about ACV’s huge 11.5% dividend: it seems unsustainable, right?

Not really.

With the fund’s discount and current leverage, it needs to earn a 7.8% gross yield to sustain its payout. This is doable, but there is one snag: the fund’s borrowing costs are high. Its average short-term loan rate is 1.75%, much higher than AVK’s and what most other CEFs pay.

For this reason, I would put a bigger bet on AVK than ACV right now, and look closely at ACV’s leverage ratio and NAV performance in the coming months. I suspect both metrics will improve because of the stellar quality of the portfolio, in which case I’d buy even more of the fund.

The bottom line? With ACV and AVK, I can produce a portfolio with an average dividend yield of around 10%, plus the potential to benefit from strong growth in tech and biotech firms—without facing the volatility of owning shares in those companies outright.

Better yet, I’m also getting those assets at a major discount, thanks to the market’s ignorance of this small but powerful asset class. If that’s not having your cake and eating it too, I don’t know what is.

The Secret to Retiring on $500,000 or Less

These two CEFs are great buys now, but they’re just the start. We also have 3 more safe closed-ends for you throwing off steady 8% to 11% yields.

They’re perfect if you feel trapped “grinding out” dividend income with 3% to 4% payers, because you can double up—and even triple up—your payout (or better) immediately by switching over to them.

These 3 overlooked CEFs are the perfect complement to the two above, because they give you even stronger diversification, together with a safe 9.6% yield and 16% upside, thanks to their deep discounts to NAV.

That would hand you $9,600 in income for every $100,000 invested—or nearly $40,000 on a $500,000 nest egg—just for making the switch to CEFs.

This is as close to a “no-brainer” investment decision as you can get, and we’re ready to share the names of these 3 incredible investments with you now. Simply click here to get all the details—including the names, tickers and buy prices—of our 3 favorite CEFs.