Is it time to buy the higher yields that industrial stocks pay, or are their dividends and profits in cyclical trouble?

I’m talking about companies that make big physical products. Their yields of 3% and even 4% or more are 50% to 100% better than the broader market. Many of these stocks are paying at their most generous rates since the financial crisis.

I like buying stocks when their yields are near the high end of their historical averages. It’s an easy, effective contrarian income strategy. And most industrials fit the bill today.

But that flies in the face of another maxim – don’t buy industrials at the top of the business cycle. The global economy isn’t exactly booming, but we are seven years removed from our last recession here in the U.S. We’re due, and these yields reflect that.

As usual, it depends on the company. Let’s start with the two industrial dividends in the most danger first.

Two Payout Hazards

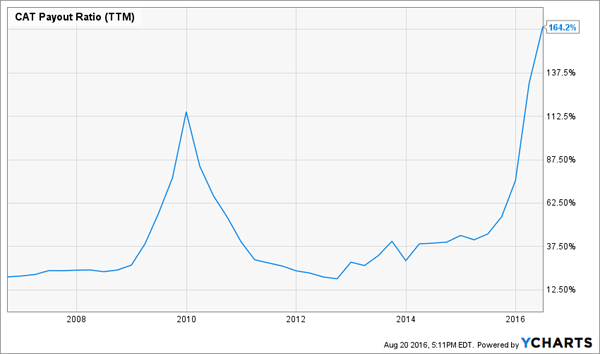

As usual, a “bull market” in the payout ratio is a big warning sign. Caterpillar (CAT) has paid out 164% of its earnings as dividends over the past four quarters.

CAT’s Exploding Payout Ratio

The firm has a strong balance sheet, so the payout is safe for now. The more disturbing trend is declining sales, down 16% last quarter year-over-year (yes, revenue headwinds extend beyond the consumer giants we like to pick on!)

Low energy and commodity prices have crushed sales for many of CAT’s products. It’s hard to picture a turnaround as long as oil is below $50 per barrel. And if you believe oil is ultimately heading higher, there are better ways to bet on it than CAT.

Pitney Bowes (PBI) is a 4.1% payer that is more of a turnaround speculation than an actual investment. Its traditional mailing business continues to evaporate as the company attempts to pivot into e-commerce software.

If that sounds crazy, well, it doesn’t appear to be working. Pitney isn’t getting enough traction to make up for its snail mail losses, and neither are its investors – the stock is down 11% year-to-date.

This payout is secure for now thanks to the cash cow legacy business. But for now this business is living on borrowed time, and its stock isn’t quite cheap enough (at 11-times free cash flow) to justify a position.

And Three Sturdier Dividends

At a glance agricultural powerhouse Deere (DE) could be lumped with our problem children. Its payout ratio has more-than-doubled over the past two years as the company has shunned dividend increases.

But here’s the deal with Deere – you want to buy it when corn prices are low, because that generally marks the bottom of its profit cycle:

When Corn is Cheap, Deere is Cheap

Sure enough, corn (and soybean) prices have begun to rally, and Deere just upped its earnings guidance for the year. With 10% of its public float currently sold short, these shares have some upside if the rally in agriculture continues.

Cummins’ (CMI) power-focused businesses are slumping this year with the firm projecting a 10% sales decline year-over-year. Demand for its products is cyclical, and this is its third revenue downturn in the last ten years.

Each previous downturn has been a good time to buy CMI:

Buy CMI on Revenue Declines

While its sales may ebb and flow, management is adept at generating gobs of free cash flow (FCF) regardless of top line action. CMI has generated significant FCF each four-quarter period over the last ten years, which has powered impressive 1,000% dividend growth over the decade!

CMI’s Cash Machine Keeps Humming and Growing

Today’s dividend is still less than half of FCF. The company should have no problem paying its investors during this cyclical downturn.

Eaton Corp (ETN) is another manufacturer-of-all-trades taking it on the sales chin, with management forecasting a 2% to 4% revenue decline this year due to lower demand for its hydraulic systems and industrial components.

Management is cautioning that it expects low organic growth in the years ahead as the global economy remains soft. That may translate to limited earnings upside, but the dividend is safe. Eaton has nearly tripled its payout over the past ten years, yet it still sits comfortably at less than half of FCF.

Eaton Earns Plenty of Cash

And Three I Like Even Better

All yields being equal, I prefer to invest in companies that are also growing their top line along with their FCF and payouts. That’s why I focus on recession-proof companies that grow their sales, cash flow and dividends year-after-year no matter what is happening in the broader economy.

The secret is finding companies profiting from niches that are growing by leaps and bounds thanks to the unstoppable trends they are riding. This is how venture capitalists invest.

But unlike VCs I don’t want to wait to cash out on my investment. I want to earn ever-increasing dividends year-after-year for years and decades on end from the same companies.

That’s why I’m passing on the industrials for now in favor of three ultimate dividend growth stocks for today’s economy. They operate in the booming healthcare sector – which explains why they’re able to grow their cash flows and already-large 6%+ dividends every year (and in one case, every single quarter.)

I just finished a research report on healthcare megatrend being driven by hordes of baby boomers rolling into retirement. Click here and I’ll send you my full analysis of this “demographic dividend growth” trend along with company names, tickers and buy prices.