When investors look for dividends, they usually think about blue-chip names that are just as common on Main Street as they are on Wall Street. However, there are a large number of single-digit stocks flying under the market’s radar that also offer attractive yields.

Individual investors tend to gravitate toward stocks trading under $10 for multiple reasons. For one, it can psychologically feel more powerful to buy 100 shares of a company trading for $8 than just eight shares of a $100 name.

While both investments are just as likely to generate attractive returns over time, low-dollar stocks have historically proven to be more volatile. In other words, they can offer active traders more bang for their buck in the short term. Volatility works both ways, which is why I’ve sifted through the names that appear to be trading under $10 for a reason and might not be able to sustain their current dividends.

Growth is always the name of the game with dividend investing. Not only do I believe these real estate investment trusts (REITs) can move above $10 over time, but there’s also room for management to potentially boost the payout.

REIT Under $10 No. 1: Generating Excess Cash

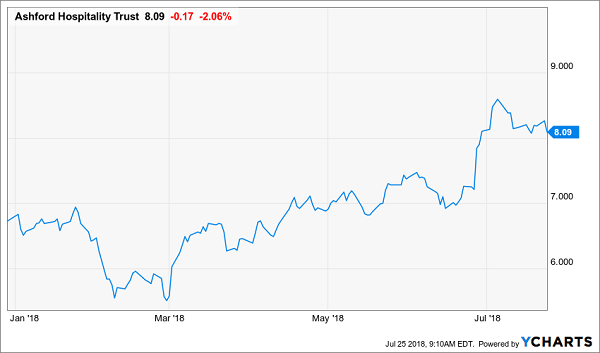

Ashford Hospitality Trust (AHT) is a REIT that focuses on upscale hotels, primarily under the Marriott and Hilton flags. The company has over 100 locations and saw core revenue per available room increase 2.5% in the first quarter of 2018, led by both price and occupancy growth. The hotel business is correlated to GDP growth, which has been above 2% four straight quarters for the first time in three years.

The stock has gained 24% year-to-date, but I believe that investors could be further rewarded by a dividend boost in the coming quarters. Ashford has not increased its payout since 2013, but there are a couple of reasons the 12-cent quarterly payment (5.9% yield) can move higher.

Back in June, management refinanced $1 billion of mortgage debt, reducing the borrowing rate by 72 basis points. Since the beginning of 2017, the company has lowered the cost on $3.4 billion of its debt, which means that more cash is flowing to bottom line and could be distributed in the form of dividends.

In addition, Ashford has $278 million of cash and equivalents on the balance sheet, or 35% of its market capitalization. This is above management’s target of a 25% to 30% cash reserve and the excess could also fund a dividend boost.

REIT Under $10 No. 2: Steady Growth Can Continue

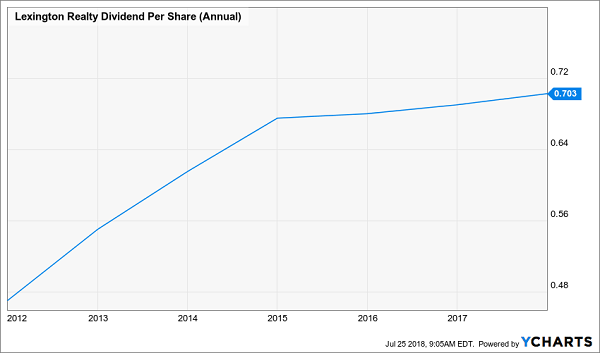

Lexington Realty Trust (LXP) is a net-lease REIT with a small stock price, but a multi-billion dollar business. The company has more than 160 single-tenant properties spread across the country and no single customer accounts for more than 4% of total base rent.

Lexington posted fractional same-store net operating income growth the first quarter of 2018, driven by rent increases. Management has guided for funds from operations (FFO) to be $0.95 to $0.98 share this year, which is more than sufficient to cover the quarterly dividend of $0.1775 a share. The company has consistently raised the payout since 2011 and I believe there is room for another boost later this year.

The dividend is backed by a solid balance sheet, and Lexington’s bonds carry an investment grade rating. In fact, management was buying back both debt and its own stock in the first quarter of 2018.

My previous experience is that under-the-radar REITs under $10 can be risky, but lucrative investments.

If, however, you’re nearing retirement, or have already retired and are living off income from your investments, I strongly encourage you to check out the top 7 REITs from Brett Owens, Contrarian Outlook’s Chief Investment Strategist. All seven are key recommendations in his 8% No Withdrawal Portfolio and check both boxes for “dividend growth” and “high current yield”.

As a group, they pay an impressive 8.5% average yield today, which is downright outstanding in a 3% world.

Combine 5% to 10%+ dividend growth with these high-single-digit current yields, and we have a formula for safe 15% to 20%+ annual gains from REITs, with a significant portion of that coming as cash dividends.

And thanks to the new tax plan, there’s never been a better time to buy REITs and live off their dividends.

(REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the new code. Investors will be allowed deduct 20% of their REIT dividend income, which means the 37% tax bill will drop to 29.6%.)

But it’s important to choose your REITs wisely.

Don’t buy a low-yielding static payer. Don’t buy a retail REIT, either (with that entire industry in a death spiral, future rent checks will be dicey for years to come).

Instead, focus on recession-proof firms, such as those that rent hospitals, business lodging and warehouses filled with Amazon packages. Landlords that own properties that will be in high demand no matter what happens to interest rates or the economy from here, in other words.