Ten percent dividends are no joke.

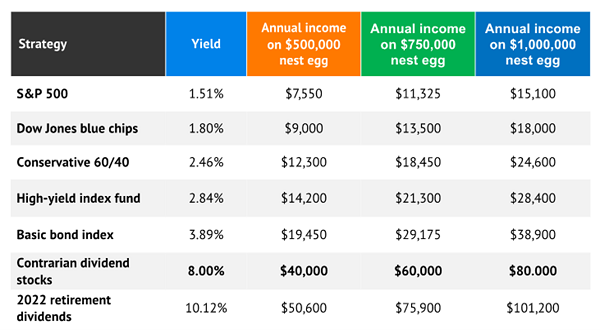

We’re talking $50,000 in annual payout income on $500K. Or $100,000 in yearly dividends on a million dollars.

This is serious cash flow. And best of all, we’re talking yields—which means, if we buy right, we can sit tight, collect these payouts and keep our nest egg intact.

Generous yields give us a big advantage over vanilla investors, who fawn over traditional blue chips (paying 2% to 3%). That’s not enough. It’s easy math.

Let’s reference the million-dollar portfolio again. If we invest in the “broader market,” the S&P 500 yields 1.5%. It’s proxy, the SPDR S&P 500 ETF Trust (SPY), pays a meager $15,000 in annual income.

Lame!

For a two-person household, we are $3,310 under the national poverty level!

At this point, we don’t have any choice but to claw away at your nest egg to make up the chasm between that dividend income and your monthly bills. Yields matter.

Yields Make the Retirement Difference

In honor of 2023, let’s pull up 23 fat yields. This list pays 7% all the way up to 18.2% per year (yup, that’s no typo).

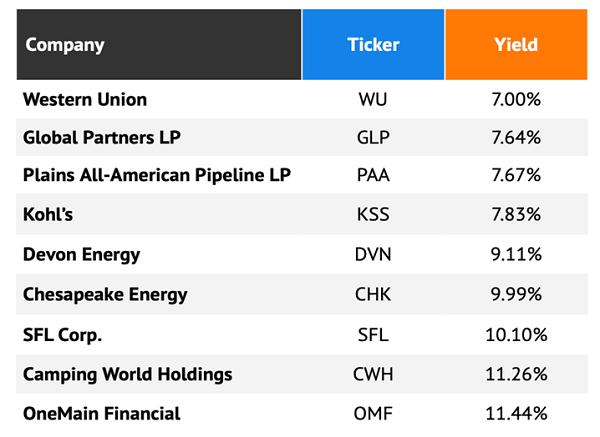

High-Yield Group #1: Traditional

Let’s start with some traditional stocks (and OK, one master limited partnership) that don’t have any special attributes—just high yields.

Chesapeake Energy (CHK) and Devon Energy (DVN) no longer have traditional dividends programs, where they pay the same amount (sans raises) every quarter. You can thank the former’s 2020 bankruptcy protection filing, and the latter’s 2016 dividend cut and years of share hemorrhaging, for that.

Now, both operate more responsible dividend programs that make sense for their commodity-centric business models. Specifically, both have a regular base dividend, then both will augment with additional variable dividends based on a percentage of cash flow. (Devon will pay up to 50% of cash flows, and Chesapeake will pay 50% of cash flows.)

Western Union (WU) and Kohl’s (KSS) reflect more traditional dividend programs—though the former’s payout has been stuck at 23.5 cents quarterly for a couple of years now while the latter literally doubled its payout in 2022.

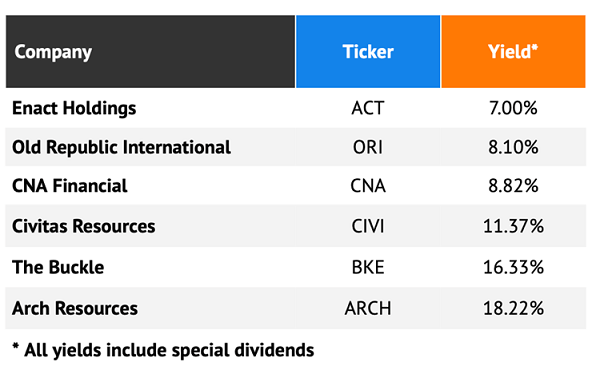

Special Payers

The term “special dividends” gets a bad rap from some income hunters. That’s because most of the time, these are one-time payments flowing from a special event—say, a company sells off a part of its business and uses some of the windfall to reward its shareholders. Naturally, you wouldn’t expect to see similar dividends going forward.

But with a handful of special dividend payers, you actually can expect somewhat regular special treatment.

Old Republic International (ORI), a general- and title-insurance provider, regularly pops up on my high-yield radar despite a headline yield of roughly 4%. That’s because most years, it pays out a generous special dividend as profits allow, often more than doubling its annual total of quarterly payouts. Still, 3.9% is an acceptable floor if you know that in most years, you can get paid out 8% or 9%.

Of course, some special payers take the idea too far and can’t really be depended upon for retirement income. Of Arch Resources’ (ARCH) 18.2% in yield, a whopping 17.5 percentage points are from numerous special dividends. And unlike the other names on this list, it doesn’t have a long history of delivering consistent special dividends—making it highly suspect for investors who value reliability.

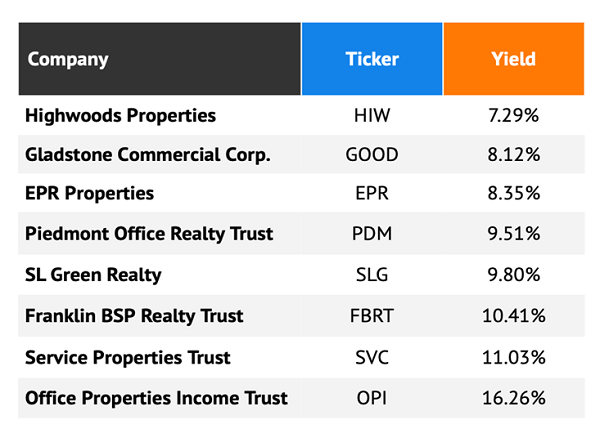

Real Estate Investment Trusts

Real estate investment trusts, or REITs, are synonymous with generous dividends. Which makes sense—they’re literally mandated to redistribute nine-tenths of their income back to their shareholders.

But these eight REITs distribute more than most—at least 2x the yield on the Vanguard Real Estate ETF (VNQ).

For instance, there’s EPR Properties (EPR), a specialty “experiences” REIT that yields more than 8% at present. Its nearly 360 locations, leased out to more than 200 tenants across 44 states and Canada, include AMC (AMC) theaters, Topgolf driving ranges, ski resorts, waterparks, even museums. EPR is still in recovery mode from deep COVID struggles that caused it to temporarily suspend the dividend. It has since reinstated that payout, and while EPR shares are off by double digits in 2022, the REIT is roughly in line with the market and outperforming the real estate sector.

Just be careful. Most of these REITs yield so much because of bad to downright atrocious performance over the past year—while REITs have lagged the market, some of these names have outright languished, and could be set for more difficulty in the year ahead. Office Properties Income Trust (OPI) and Piedmont Office Realty Trust (PDM) have lost 45% and 52%, respectively, for the year-to-date through late 2022. Yes, some employers are finally shoving their workers back into cubicles, but that momentum could falter if the economy does fall into recession in 2023.

Give Me 4 Minutes and You Could 4X Your Retirement Income

In short, while the 23 yields above are nice, their positioning as we go into 2023 is fairly spotty.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to be able to plan around our income with laser precision—a tall, tall task when the Fed is constantly tinkering with its monetary policy.

But fortunately, we’re navigating the Fed—and a seesaw U.S. economy!—just fine in our “Perfect Income” portfolio.

And now, you can too.

The perfect dividend retirement stocks have several things in common:

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Even better, many investors could double, triple, even quadruple the dividends they’re receiving from the average S&P 500 stocks.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!