I was in heaven. One baseball toss away was a man of surreal size, Aaron Judge.

The New York Yankee slugger. All six-foot-seven standing in a minor league ballpark right here in Sacramento’s Sutter Health Park.

My family and I sat second row, right behind the dugout. I’d waited until just four hours before first pitch to buy the tickets. (A contrarian purchasing strategy that usually works because most buyers don’t have the stomach for it. Here once again it paid off with reasonably priced dugout seats to watch the Yanks at a fraction of the price we’d have paid in the Bronx.)

Our Last-Minute Seats (Not Bad!)

Then my kids turned to me. “Daddy, this is boring.”

Well, of course it’s boring, kids. It’s baseball!

My kids are football and basketball watchers. The swing-and-a-miss rhythm of modern baseball was not fun for them. Fair enough, it’s what baseball has become over the last twenty or thirty years. The hitting instructors have optimized the sport into a simple framework: swing for the fences, hit it over everyone.

And if you strike out? Eh. Cost of doing business. The analytics say it works. But it’s admittedly a grind to watch.

Wall Street “research” works the same way. Our analyst friends tend to swing and miss too! The difference? Their batting averages aren’t tracked.

They whiff on one stock call, shrug, and move on to the next recommendation. They don’t get demoted or sent down to the minors. Their batting averages are bad and these clowns never get called out. Which is good news for contrarians like us.

Here’s how we capitalize on their incompetence.

A widely cited academic study on analyst target price accuracy found that only about 54% of 12-month price targets correctly predicted even the direction of the subsequent price move.

Fifty-four percent. On direction alone. That’s barely better than a coin flip!

Analysts give specific price targets to stocks like they are scripture. In reality, they don’t even know if the thing is going to move up or down!

And it gets uglier. A 2024 Yale School of Management study found that analysts systematically delay downgrading stocks after bad news — to curry favor with the companies they cover. The suits aren’t just bad at predicting stock moves. They’re deliberately stalling their warnings to protect their banking relationships.

Put those two facts together and the picture is clear. Wall Street “research” is a farce. Which is exactly why it works so well as a contrarian indicator!

When Wall Street’s collective price target sits below the stock’s current price, that’s not a signal to sell. That’s a signal that full pessimism is baked in! All it takes is one decent earnings report and the stock gaps higher while the research machine scrambles to reload.

Which is exactly how my Dividend Swing Trader subscribers banked 24% returns in two weeks on Texas Instruments (TXN).

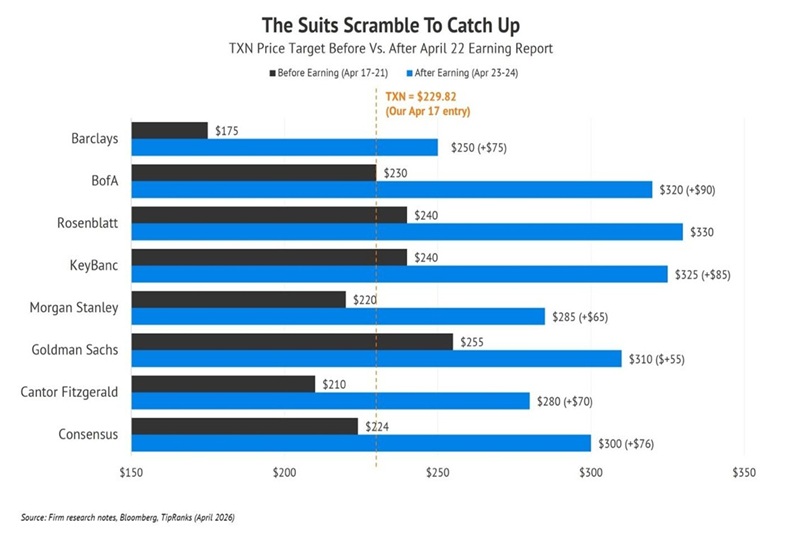

Heading into last Wednesday’s earnings report, the Wall Street research on Texas Instruments was about as bearish as it gets. The analyst consensus price target was below the stock’s current trading price—meaning the suits, as a group, thought TXN was already overvalued. Barclays had the stock at Underweight. The bears were all aligned.

The tariff story drove the bear case. TXN manufactures globally—with fabs in China and Japan—and the herd priced in worst-case trade scenarios.

What they missed: TXN is reshoring aggressively. The company committed to invest $60 billion in new US fab capacity. It secured $1.6 billion in direct CHIPS Act funding plus $6 to $8 billion in investment tax credits. The Sherman, Texas fab already produces chips. The Lehi, Utah facility comes online this year.

The CHIPS Act literally pays TXN to bring manufacturing home. Every tariff headline that scared the suits actually accelerated TXN’s competitive position.

On cue, last Wednesday, TXN reported. Revenue rose 19% year-over-year. Earnings beat consensus by 24%. Management guided next-quarter revenue 8% higher than the quarter they just blew out. CEO Haviv Ilan even flagged the possibility of price increases in the back half of 2026.

And then the “research machine” swung into action. Ha! What a joke. Overnight, the same Barclays analyst who had TXN at Underweight two days earlier hiked his price target by $75. BofA slapped a Buy rating on it with a $320 target. Rosenblatt went to $330, KeyBanc to $325.

The vanilla boys were chasing the move, late to the party, as always.

Longtime readers know this playbook, because we ran it on TXN before. Back in June 2017, I recommended TXN to my Hidden Yields subscribers at $79.70. We held the position for four and a half years. We collected nearly $15 per share in dividends along the way. And in January 2022, we sold at $175.72 for a 148% total return—22% annualized. From a “boring” chipmaker!

Most investors would have moved on after a trade like that. Not us. We watched. We waited. And when the herd panicked on tariffs and pulled TXN back into our buy zone, we stepped up to the plate again.

Same framework. Find the dividend-growth compounder the suits are sleeping on, buy before the earnings catalyst and let the chasers drive the price higher after the fact.

Straight talk on TXN: the stock is now trading above my original $230 buy-up-to price. I’m not recommending that new money chase it here. The trade has moved.

But that’s the point. My subscribers got TXN before the 24% rip. Before the Barclays upgrade. Before the $75 overnight target hike. Before CNBC found the story.

If you want to hear about the next setup before the research machine catches up, you need to be inside my Hidden Yields service. I find the next “boring” dividend grower the suits can’t bring themselves to recommend. My subscribers buy it. We wait for the earnings catalyst. And we let the analysts catch up to us.

The question isn’t whether we’ll call the next one right. It’s whether you’ll be on the right side of the trade when we do. Click here to start your risk-free trial of Hidden Yields.