Few people realize it, but there’s a way to take a “low” dividend yield and “convert” it to a payout four times higher. Maybe even more.

The stocks we need to get this “hidden” payout are hiding in plain sight. To find them, we need to be on the lookout for three key strengths:

- A growing, and ideally accelerating, dividend.

- A history of share buybacks, and …

- A high “shareholder yield,” which combines the first two points (I’ll come back to that in a second).

Even better if we can find a stock whose share price has fallen behind dividend growth. That way, we can grab some price upside to go along with our high “hidden” yield.

The best way for me to explain this strategy is to let you see it in action. Once we’ve done that, I’m sure you’ll find it easy to put into practice and find more of these overlooked income plays on your own.

Let’s start with a “low-yielding” railway whose stock has been on the siding for years:

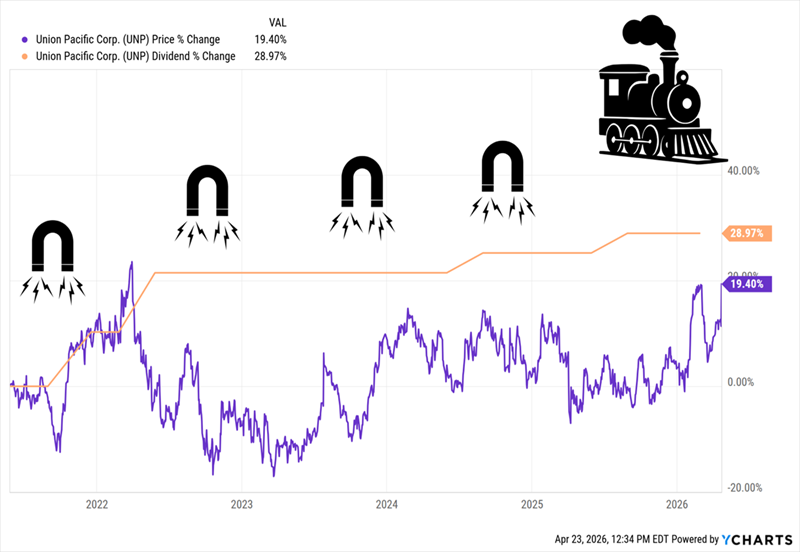

Union Pacific’s 2% Yield Jumps to 3.7% Now, 6.3% Later

Union Pacific (UNP) has hit wave after wave of challenges in the last few years: COVID-19 shipping disruptions, post-pandemic inflation and, more recently, trade worries. (UNP’s track network dominates in the West and Midwest, including key ports at San Francisco and Long Beach, and stretches down into Mexico.)

As a result, the stock has more or less moved sideways since 2022, though it has thrown some coal in the boiler lately, on a potential merger with Norfolk Southern (NSC)—more on that in a moment.

For now, let’s set aside the bluster around trade because the numbers say something else: In 2025, US imports from Mexico came in at $534.9 billion, according to the United States Trade Representative (USTR), up a healthy 5.8% from 2024. US exports to the country also gained, to the tune of 1.2%.

Moreover, the USMCA is up for review this year. While there’s been a lot of hand-wringing here, unless the US walks away—unlikely, without the support of Congress and in light of higher inflation—the deal does not disappear. It’ll simply be up for annual review until 2036, unless extended.

Trade misunderstandings alone make UNP a bargain. The “hidden” yield we’re going to get into now makes it even more intriguing.

As I write this, UNP sports a current yield of just 2%, not enough to get our hearts racing. But that number masks dividend growth: In the last decade, UNP’s payout has shot up 151%. So anyone who bought in the spring of 2016 is yielding a lot more than 2%—closer to 6.3% on their original buy.

Moreover, in the last five years, UNP’s share price has fallen behind its dividend. That sets it up for “snap-back” gains—especially as management has restarted dividend hikes:

UNP’s Dividend Magnet Powers Up

I expect those hikes to continue as UNP gets more efficient: Its adjusted operating ratio—the lower the better—fell to 59.9% in the latest quarter, down from 60.7% a year ago. Freight revenue jumped 4% and adjusted EPS popped 8.5%.

Meantime, we don’t even have to wait a decade for dividend growth to “convert” UNP’s 2% yield into something much higher.

This is where “shareholder yield” comes in.

It’s a complete measure of how a stock rewards us. You calculate it by taking the amount spent on buybacks and dividends in the last 12 months, deducting share issuances, then dividing into the company’s market cap.

This makes a big difference for a company like UNP, which emphasizes buybacks: In the last 12 months, management repurchased $2.7 billion of its own stock and spent $3.2 billion on dividends (with no issuances). The total—$5.9 billion—is 3.7% of the company’s $158.7 billion market cap. That’s 85% higher than UNP’s current yield, and a much better measure of what we’re really getting here.

Big Merger Could Unlock More Upside

As I touched on a second ago, UNP is working to convince regulators to approve its proposed merger with Norfolk Southern (NSC) for $85 billion cash and stock. It’s far from clear they’ll agree, but UNP’s prospects look strong either way.

If the deal fails, UNP is left with its already-strong business. If it passes, the company’s strong balance sheet will help it integrate Norfolk Southern. Plus, both railroads generated about $4.5 billion in combined free cash flow last year. Going forward, that would also help defray the deal’s cost.

And of course, the combined company would boost its pricing power, too.

But that’s further down the tracks. Right now, the thing to remember is that the company’s 2% yield is just a starting point. Shareholder yield gives it a kick higher right away, then dividend and buyback growth work their magic as time goes on.

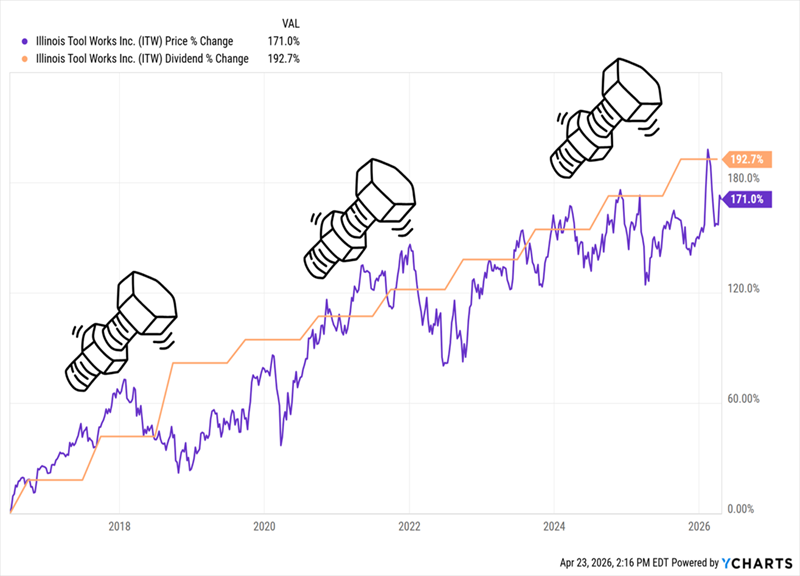

Illinois Tool Works’ 2.4% Yield Flips to 4.2%, Then “Stair Steps” to 6.2%+

Illinois Tool Works (ITW) is another “boring” dividend stock that fits nicely with our shareholder yield/dividend-growth formula.

The company has a place in countless industrial businesses, churning out everything from fasteners and plastic car parts to commercial kitchen equipment, welding materials and gear for testing electronics.

ITW’s current yield looks a lot like that of UNP, around 2.4% today. But also as with UNP, this number masks two other—and more important—drivers of shareholder returns: dividend growth and buybacks.

Let’s start with payout growth, as ITW has one of the strongest Dividend Magnets out there:

ITW’s Share Price Is Bolted to Its Payout

That’s about as clear as the dividend/share-price relationship gets! Every time the share price falls behind (as it has now), it snaps back above the dividend in short order.

And of course, there’s the effect that payout has on yield on cost, and it’s substantial: Anyone who bought 10 years ago is getting nearly triple the stock’s current yield out of their upfront investment: a stout 6.7%.

Not bad! And with revenue up 4% in the latest quarter, the business generating solid operating margins of 26.5% and EPS popping 7%, we can expect more payout growth.

But let’s bring it back to today and talk shareholder yield. It’s particularly important here because ITW spends nearly as much on buybacks ($1.5 billion in the last year) as it does on dividends ($1.8 billion). Add those two together ($3.3 billion) and divide into ITW’s $78.7 billion market cap and you get a shareholder yield of 4.2%.

That’s a much more realistic (and frankly better!) place to start than the stock’s 2.4% current yield. Anyone buying now can then sit back and let management’s ongoing dividend (and buyback) hikes drive their shareholder yield higher.

5 More Stocks With Surging Payouts (and Big Shareholder Yields, Too)

UNP and ITW are solid. But I’ve uncovered 5 other stocks that are further along the curve, with high shareholder yields and faster payout growth.

I expect them to announce their next big dividend hikes in the coming weeks and months. And if history is any guide (it is!), their share prices will rise immediately after.

We want to get in before that happens. Click here and I’ll give you my full “Dividend Magnet” strategy and send you a free Special Report revealing these 5 stocks’ names and tickers.