I’ve always avoided “paper payout tigers” – stocks that look great on paper and have great, but unsustainable, payout yields. If you own any of these, sell now. Many of these “zeros” looked like heroes thanks to semi-permanently low rates.

But with Wall Street’s new focus on interest rates, the landscape has shifted for many industries that have relied upon cheap capital. With so many out there, it can be hard for an investor to find an issue without risk.

Last month I cautioned that mortgage REITs (mREITs) like Annaly Capital (NLY) should be sold immediately. As interest rates climb, the borrowing costs for these firms increase. Worse, their portfolio holdings are being devalued with every Fed interest rate hike.

As these firms are forced to cut their payouts, their stock prices will plunge – just as they did in the second half of 2004 when then-Fed Chair Alan Greenspan hiked rates.

Two Harbors Investment Corp (TWO) and New Residential Investment Corp (NRZ) are two more paper payout tigers. The “smart money” institutional investors are fleeing in anticipation of rates hikes.

That leaves naïve first-level individual investors piling into these stocks that look great at first glance. TWO pays 12.5% annually while NRZ yields 15.1%.

As they say in late-night infomercials, after you buy the only knife you’re even going to need, they’re going to throw in another knife… for free. Or in this case, a stock price plunge to match a slashed dividend.

Like Annaly, these two knives will cut you. Unfortunately, the mREIT segment is crowded with them. But don’t despair – there are safer REITs that are more insulated from rising interest rates.

Trade in Your mREIT for a Rental

When looking for values in an unloved sector I consider the strongest and biggest players first. They have the best chances of weathering any hiccups.

It’s why I’m looking squarely at Equity Residential (EQR) and Avalonbay Communities (AVB). With market caps over $25 billion they are larger than the next biggest firm by $10 billion.

I like that these firms both invest in multi-family properties as opposed to single family mortgage debt. Apartment communities are stable and have been in demand as investments.

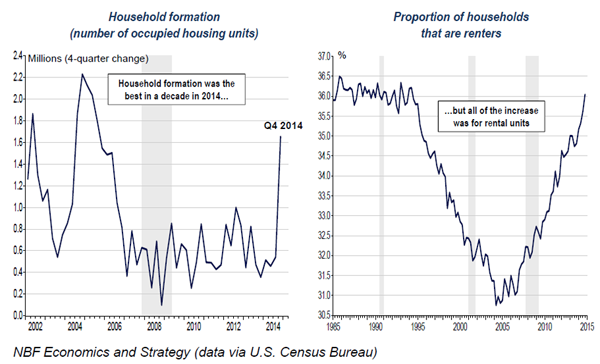

Two lingering effects of the financial collapse have been the reduced levels of home buying and the limited creation of new households. Kids these days are scared to buy their first home and instead choose to rent far longer than prior generations did.

New Households Are Choosing To Rent Rather Than Buy

You can see from the chart that when we did see an increase in household creation, it was driven by renters and not homeowners. That’s good news if you’re a landlord.

Equity Residential is currently paying a dividend of $2.21 that yields 2.7% while Avalonbay is delivering a $5.00 dividend that also yields 2.7%.

Institutional investors on Wall Street may be concerned about some of the aggressive payouts from some mREITs – but not these two. Equity Residential spots a 98.8% institutional ownership while Avalonbay has 99.3%.

These two heavyweights might have the strength to weather the onslaught of rate increases even as a number of their competitors go under. It’s what the big guys are betting on.

If you’re looking to decrease your risk even more, consider spreading your investment across a number of other big players like Essex Property Trust (ESS), Mid-America Apartment Communities Inc. (MAA) UDR Inc (UDR) or Apartment Investment and Management Company (AIV).

The Best REITs To Buy Today

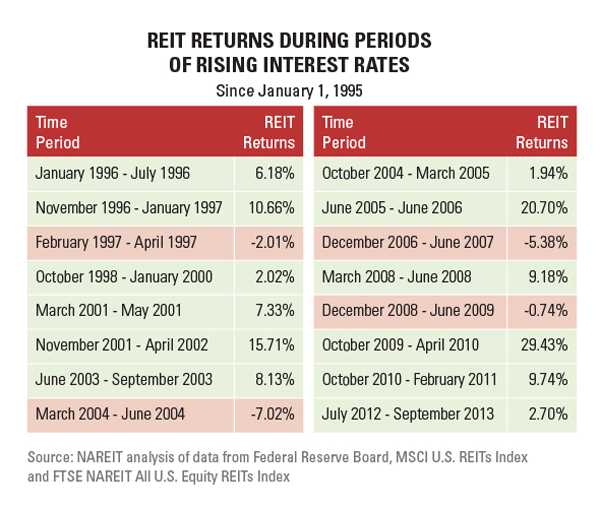

REITs in general have usually performed well during periods of rising interest rates.

The sector as a whole got pummeled in 2015 on interest rate fears – making now the ideal time to buy the best REITs. Instead of mortgage REITs, I prefer a sector that’s capitalizing of the biggest demographic shift in U.S. history. Let me explain…

No matter what the Fed does with rates from here, or how GDP grows in the coming years, there’s one sure economic bet in America:

The country will be older in the future than it is now.

There’s a bull market unfolding as Americans get older, and it will run for at least two or three decades. Here’s what’s driving profits in the America-is-getting-older trend:

- 77 million Baby Boomers – 28% of the entire US population – are starting to turn 65 at a rate of nearly 10,000 per day.

- We’re living longer than ever before thanks to healthier choices and advances in medical technology. That means the 65+ population will double and the 85+ population will triple in the coming years.

- Americans over 65 are three times more likely to be admitted to a hospital, and for longer periods of time and for more expensive types of care.

By 2024, national healthcare expenditures are expected to climb to $5.43 trillion, or about 20% of GDP. This colossal spending will be driven in large part by the increasing demands of the massive Boomer demographic, and are certain to continue for the next 30 years.

Healthcare REITs in particular are perfectly setup to capitalize on this massive demographic shift. My top three are all bargains today thanks to last year’s rate hike panic.

They pay yields of 6.3%, 7.2%, and 7.6%. And all three companies are increasing earnings and their dividends annually. Click here for the names of all three and to learn how we’re playing the biggest demographic shift in U.S. history.