Whether you own a Treasury or the typical dividend stock these days, you’re still losing money after inflation.

I know what you’re thinking: tell me something I don’t know!

But there’s a solution hiding in plain sight: closed-end funds (CEFs), a widely overlooked (and publicly traded) asset class that often throws off rich payouts of 8% or more. We’ll do a deep dive into these scandalously overlooked income plays, and how they pay those big (and often monthly) dividends in a moment.

Here’s the top-line takeaway, though: by going with a CEF, you won’t have to sell the blue chips you own now. CEFs, like their ETF cousins, hold the Apples, Microsofts and Walmarts of the world. But unlike ETFs, CEFs pay you high—and often monthly—dividends. The three CEFs I’ll show you below pay even more, a healthy 10% on average.

How CEFs Help You Close the “Inflation Gap”

A 10% yield is well above inflation, and as rising prices start to ebb (as I expect through the end of this year and into 2023), you’ll be even further ahead of the game.

Before we get to the “instant” 3-CEF portfolio I want to show you today, let’s do a quick run-through on what CEFs actually are.

In your typical mutual fund or ETF, managers are happy to take in as much investor cash as possible, even if they aren’t prepared to invest it right away. That’s because these are “open-ended” funds that can swell to infinity in size—as long as investors keep pumping money in.

CEFs, meanwhile, go through their IPOs with a strict mandate that limits their ability to offer new shares, keeping the size of the fund roughly the same throughout its life. There are many advantages to this, including the fact that management can’t get greedy and accept more money, even if market opportunities are limited.

Here’s the best part: the closed-end structure allows CEFs to focus on returning as much capital as possible to shareholders in the form of income, often in monthly dividends. This is another way CEFs limit their size, and it also means a lot of funds pay huge payouts to investors.

The Anatomy of a CEF

Source: CEF Insider

CEFs work just like ETFs in that they pool together a bunch of cash from investors to invest in the market, whether it’s stocks, bonds or something else. The difference with CEFs is that their managers are always focused on returning as much cash to shareholders as possible, and as often as possible.

Ideally, a CEF will target a return like 7% or 8% per year, on average, and then target paying out that return in annual dividends. This helps keep management honest and helps CEF investors hold on to their assets during market downturns—always the worst time to sell—and live off their payouts until the storm passes.

A 3-CEF Portfolio Yielding 10% That You Can Buy Today

Now let’s take a look at the three CEFs I mentioned earlier, which give us that outsized 10% yield.

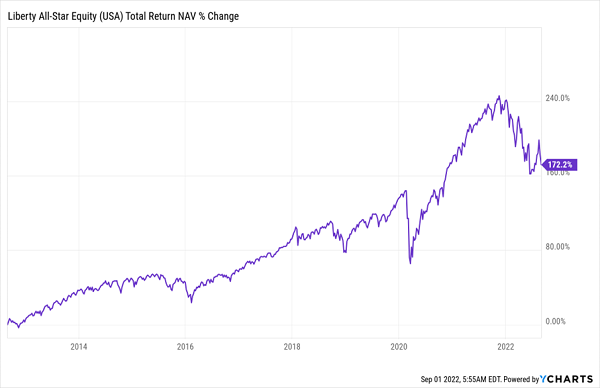

Our first pick is the 10.1%-yielding Liberty All-Star Equity Fund (USA), whose top holdings include Amazon.com (AMZN), Alphabet (GOOG), Microsoft (MSFT) and Visa (V), all companies with tremendous cash flows and strong long-term gains.

That’s translated directly into a strong long-term track record for USA.

USA’s Big Profits Fund Big Payouts

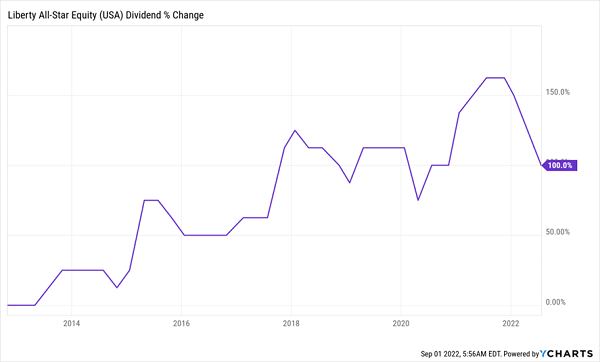

If you’re worried that USA’s 10.1% yield is unsustainable, this chart should put you at ease. With a 10.5% annualized return on its portfolio over the last decade, the fund has easily covered its payouts. In fact, it’s done such a good job that management has doubled the dividend over this period.

USA’s Dividend Doubles

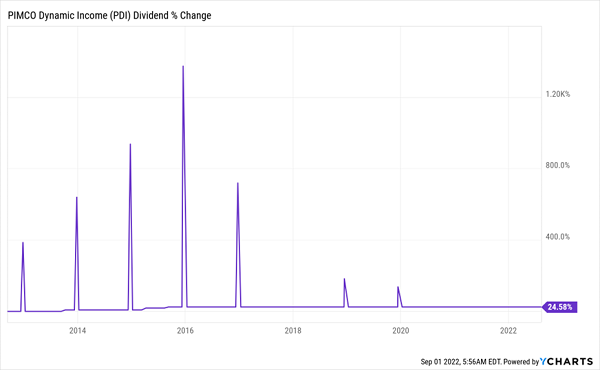

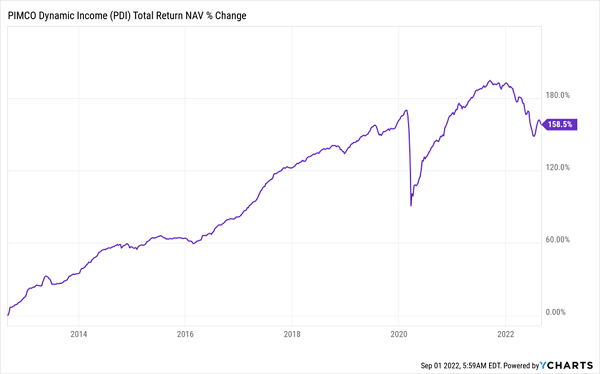

Now let’s move on to our second pick, the 12.2%-yielding PIMCO Dynamic Income Fund (PDI), whose payouts have also defied gravity over the last decade.

Big Regular Payouts—and Big “Bonus” Dividends, Too

Now, a 24.6% hike in payouts isn’t as impressive as USA’s doubling of its dividend, but check out those spikes: those are special dividends PDI pays out in years of particularly strong performance—and also note that this happened the last time the Fed was hiking interest rates (from 2015 to 2019).

That’s because PDI plays the various corners of the bond markets to find income and rising prices, according to whatever the Fed is doing at that particular time. It’s an active management strategy that’s paid off, with a 10% annualized return over the last decade, during times of rate hikes and cuts.

PIMCO Doesn’t Fight the Fed

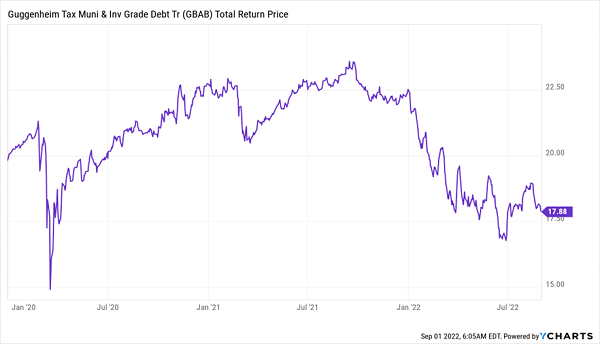

Now let’s get another group of even safer dividends with the Guggenheim Taxable Municipal Bond and Investment Grade Debt Trust (GBAB), a municipal-bond fund that looks for the highest-yielding taxable municipal bonds out there.

(Note that most municipal-bond funds’ dividends are tax-free for most Americans. That’s not the case with GBAB, because it also holds corporate bonds. However, its 8.4% yield, the highest in the muni-bond space, more than makes up for this.)

Another big plus is the fund’s stability, with default rates on muni bonds running at a microscopic rate below 0.1%. And buying through a diversified fund like this, which collects over a hundred muni bonds, adds yet another level of safety.

Add on top of that the simple fact that tax revenues are up across America and President Biden has earmarked a trillion dollars to go into infrastructure in municipalities across the country, and it’s easy to see why buying GBAB makes sense now. Yet investors have panicked to the point that they’ve reduced this safe and reliable income producer to bargain levels.

GBAB Is Dramatically Oversold

While we wait for the current selloff to abate, GBAB will give us an income stream that’s big enough for many folks to live on. That makes the fund a great hold in periods like this. We’ll then rotate out of it, and into a fund with more alpha, when markets turn from fear to greed.

5 Monthly Dividend CEFs With Big UpsiYielding 7.9%

There are just two snags with the CEFs above: 1) Only two pay dividends monthly (USA’s payout is “managed,” or tied to the value of its portfolio), and 2) They’re all just a bit pricey, trading at premiums to net asset value (NAV, or the value of the assets they own).

We demand discounts when we buy CEFs, and we want monthly dividends, too! That’s what the 5 other CEFs I’ve uncovered deliver now. They trade at huge discounts that simply can’t last, which gives us a shot at some nice upside in the coming years. Plus these 5 funds yield a reliable 7.9% on average and pay dividends monthly, too!

So their payouts line up perfectly with our bills.

Don’t miss this opportunity for gains and a monthly income stream that can see you through this market mess. Click here and I’ll share my complete CEF investing strategy and give you the names, tickers, current yields and my complete analysis of each of these 5 monthly paying funds.