We all know financial stocks have gone through the roof since President Trump’s win. So the question becomes: what do we do with these companies now?

There’s no one answer for every financial stock, of course. Some are still great, undervalued buys—but there are two that have gotten grossly overvalued and should be avoided, or sold if you hold them. (Below, I’ll reveal 2 better high-yield stocks to buy instead.)

These 2 Financials Are Headed for Trouble

Bank of America (BAC) is the first bank on my hit list.

A Breathtaking Rise

After spending most of 2016 in the red, BAC has soared more than 37% in three months. Nothing much has changed at the bank; it’s just riding a wave of euphoria as investors bet that Trump’s America will mean higher interest rates and fewer regulations, driving up BAC’s earnings.

However, the stock’s recent outperformance is far above that of peer Citigroup (C), which is up only 15% since Election Day:

“Only” 15% Gains in 3 Months

Still, that’s a lot of price growth—far more than is justified. Here’s why.

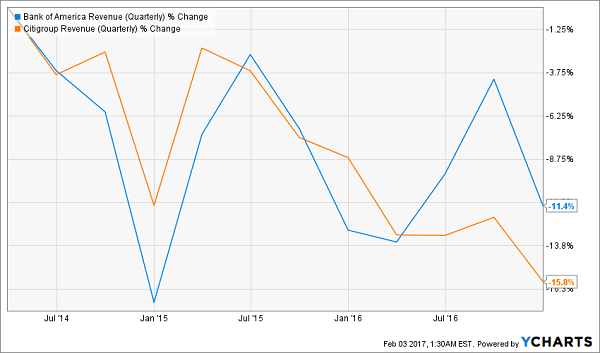

For starters, Citigroup is getting smaller. Its revenue has collapsed in the last three years (the same thing is happening to BAC, by the way, though not as severely):

Stock Prices Up, Revenues Down

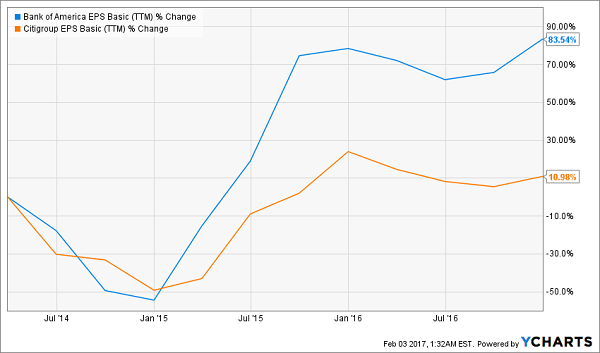

Thanks to cost cutting, Citigroup has been able to grow earnings per share by a pittance over the same time period—but Bank of America has actually been much better at this game:

No Growth Behind These Earnings

But that doesn’t mean BAC is a buy; both of these stocks are sells. Why? Because they’re too expensive relative to their performance:

Higher Price, Lower Growth

You’re paying a price-to-book value of almost 1 for BAC, while C is now priced at the same discount we would’ve gotten in 2014 and 2015. That’s no bargain, considering C’s revenue decline, and BAC’s earnings growth seems fully priced in. Besides, how long can BAC keep growing earnings while losing market share?

With all that in mind, I think we need to look for alternatives. Here are three.

2 Under-the-Radar Stocks With Gains Ahead

These aren’t financial names, because the sector as a whole is highly overvalued right now. Instead, we’re going to rotate into other areas and wait for some downtrodden but high-quality companies to come back into the limelight.

If we do that, we find a couple of stocks with attractive price-to-book ratios, considering their revenue growth, dividends and earnings potential.

They are: Aircastle (AYR) and Frontier Communications (FTR):

2 True Bargains

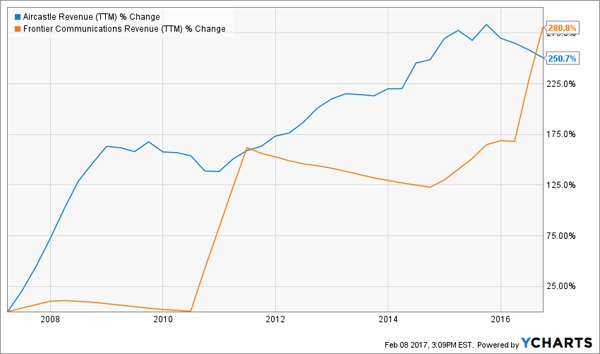

Unlike BAC and C, these companies’ revenues are rising. NE has the slowest sales growth, but it’s still up over the past decade—and the lower price-to-book ratio means we’re getting compensated for that slower growth:

Rising Sales From Expanding Firms

We’re also not buying these stocks at the top, since they have been out of favor for months:

Not the Market Darlings

Note, however, that AYR is up big over the last year (it’s shot up over 40%). It’s also got a price-to-earnings ratio of around 13, which is half that of the S&P 500. So this stock isn’t priced for growth, even though that’s clearly what it’s doing.

Finally, let’s look at dividends. Bank of America and Citigroup pay a measly 1% yield, on average, but look at the payouts with these two alternatives:

Massive Payouts

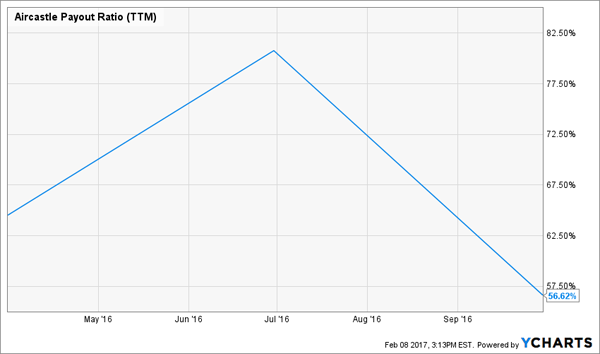

The over 4% yield at AYR is great—and the outlook for dividend growth is strong, too, thanks to their low payout ratios (or the percentage of earnings sent out to investors as dividends):

Safe Payouts Set to Rise

However, we need to be cautious about FTR. A yield above 12%? What’s the deal with that?

Simple—the market is expecting FTR to cut its dividend. And it probably will. But that doesn’t matter to me, because this has been priced in for years:

Investors Give Up on FTR

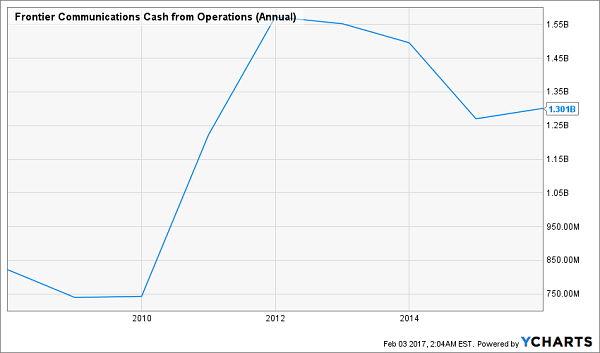

However, the company’s cash from operations has skyrocketed, thanks to the firm’s growth:

A Cash Machine

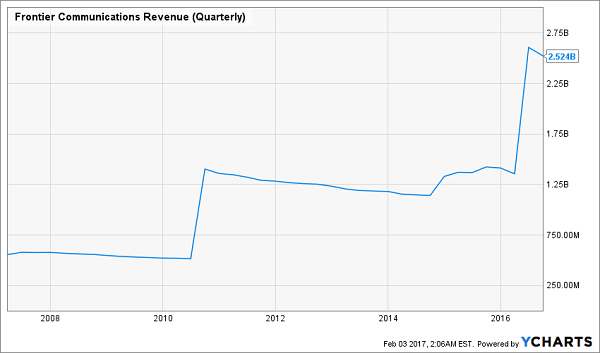

Again, that growth is coming from a strength Citigroup and Bank of America lack—more sales:

Revenue Skyrockets

So I don’t expect that 12% dividend to last forever, but I also don’t expect the stock price to collapse if/when a dividend cut comes. We all know it’s going to happen, which has made the stock oversold—and created a buying opportunity.

FTR is 12% yield is great, but with a dividend cut a distinct possibility, the stock comes with a caveat: you need to keep a close eye on it and handle it with care.

If you prefer a lower-risk “set-it-and-forget-it” high-yield investment, you’re in luck … because I’ve got those for you, too—6 of them, actually.

I’m talking about the 6 reliable income generators in our new “No-Withdrawal” retirement portfolio. They throw off rock-solid yields of 6%, 8%, 9% and up.

And with an average yield of 8.0%, this portfolio will easily hand you a $40,000 income stream on a $500,000 nest egg.

Each of those payouts is backed by rock-solid balance sheets and surging cash flows. These income powerhouses are all cheap now, but I don’t expect that to last.

These no-drama plays are perfect for 2017, with the market starting to look twitchy after the go-go “Trump bump.” Don’t miss out. Click here and I’ll share our 6 top picks for high income and double-digit upside.