Today, I want to talk to you about my favorite strategy for beating the market and building long-term wealth.

If you’ve been reading my regular columns on Forbes and ContrarianOutlook.com, you probably already know what it is: buy dividend growth. (I’ll name 4 individual stocks that should be on your list now in just a moment.)

Because as I’ve written before, stocks that regularly hike their payouts outperform any other kind of company over time. You can give yourself a bigger edge if you invest in companies that surprise the market with bigger-than-expected dividend hikes.

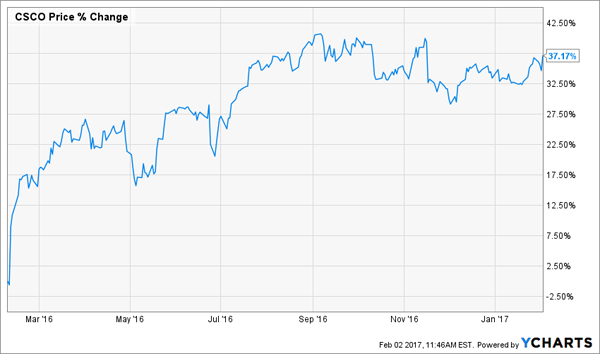

Take Cisco Systems (CSCO), which “accelerated” its quarterly payout last February: after three years of $0.02- and $0.03-a-year increases, Cisco “went big,” boosting its dividend by $0.05, or 23.8%.

Management declared the new dividend on February 10, 2016; if you’d bought the day before, you’d be up 37% right now:

Big Payout Hike Ignites CSCO

Problem is, Cisco’s sales and earnings are flattening out, and its payout ratio (or the percentage of earnings paid out as dividends) is edging up near 50%. So even if it does drop another outsized hike on investors this month, I don’t expect that run to continue.

But that’s not the case with the four other stocks I’ve got for you today.

SHW: The Color of Money

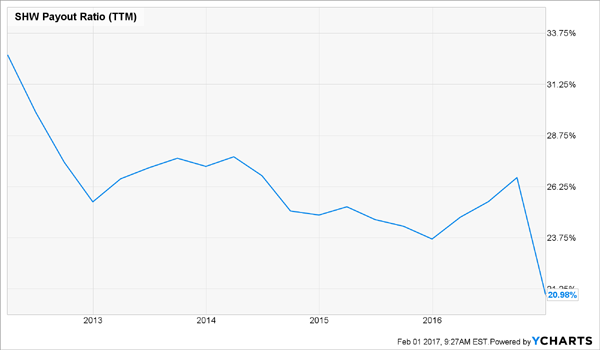

Sherwin-Williams (SHW) investors can count on a dividend hike in mid-February, when the paint maker typically announces its quarterly payout for the coming year.

Sherwin has raised its dividend for 37 straight years, and it’s unlikely to break that streak now. Quite the contrary: in the last three years, the payout has jumped 18.8%, on average, and I expect at least that again this month.

Why? For one, the company just reported fourth-quarter revenue and earnings that blew past expectations. Management will be keen to draw attention to that, and a fat dividend hike is a great way to do it.

They have plenty of room: SHW’s payout ratio is minuscule, even with the outsized dividend raises it’s been dishing out:

A Safe, Growing Payout

You might think Sherwin’s upside is capped by its seemingly high forward price-to-earnings (P/E) ratio of 22.2, but that’s still below its five-year average of 22.5.

And investors are right to expect growth: according to the Leading Indicator of Remodeling Activity, US home-reno spending will jump 6.7% this year. With 37% of the paint market—and likely closer to 50% once it closes its merger with rival Valspar (VAL)—Sherwin’s perfectly placed to capitalize.

Meantime, the all-but-guaranteed dividend hikes will keep driving the stock price higher. Check out how SHW has risen in lockstep with the payout:

Dividend Doubles, SHW Triples

This 151-year-old company currently offers a 1.1% forward dividend yield. The time to buy is now.

LEA: A Dividend in Overdrive

Lear Corp. (LEA) may not get your blood pumping on the current yield front—it pays just 0.85%—but it certainly should when it comes to dividend growth. In the past five years, the automotive seat maker’s payout has more than doubled. As with Sherwin, that’s helped ignite the stock:

Another Triple-Double

Last February, Lear handed out a 20% dividend increase, and I see another double-digit hike coming this year, likely mid-month.

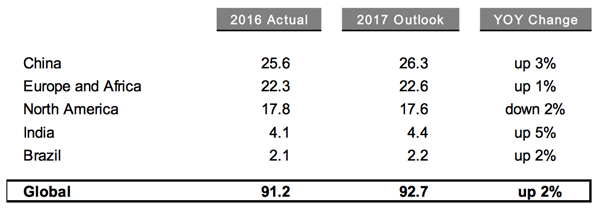

Sure, North American car sales have plateaued, but Lear gets 60% of its revenue from outside the continent, and it’s forecasting gains in all of its other regions.

Car Sales Roll On

Source: Lear Corp.

That will help drive Lear’s revenue up to $19.5 billion, topping the record $18.6 billion it posted in 2016. And it’s sitting on a record order backlog, to boot.

The company also has a relatively small number of locations (just 9% of its total) in Mexico, the country that’s taken the brunt of President Trump’s ire lately. Meantime, Trump’s tax and infrastructure proposals could goose job and wage growth in the US—and send more Americans to their local dealership.

Above all, Lear is a free-cash-flow machine, cranking out $1.1 billion worth in the last 12 months. Its dividend accounts for a mere 7.1% of that—one of the lowest ratios I’ve ever seen in a dividend stock.

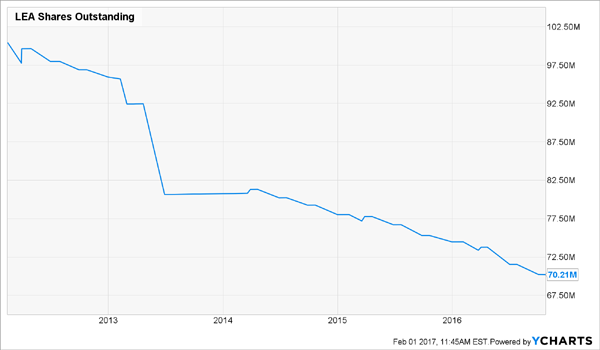

Finally, Lear is cheap, trading at just 9.0 times forward earnings. That, plus management’s aggressive buybacks, give you some added downside protection:

A Buyback Champ

NHI: A Long-Term Outperformer

National Health Investors (NHI) is a real estate investment trust (REIT) that finances seniors’ housing facilities through mortgage, sale-leaseback, joint-venture and other forms of financing.

You won’t find Sherwin- or Lear-style double-digit payout growth here. What you will find is consistency: NHI’s payout has risen for 14 straight years, and those hikes are still healthy, with the dividend growing at 7.7% annualized over the past five years. Plus, the REIT sets you up with an outsized 4.9% forward dividend yield right off the bat.

And if you bought NHI a decade ago, you’re no doubt happy today. On a total-return basis, the REIT has crushed the benchmark SPDR S&P 500 ETF (SPY):

Built for the Long Haul

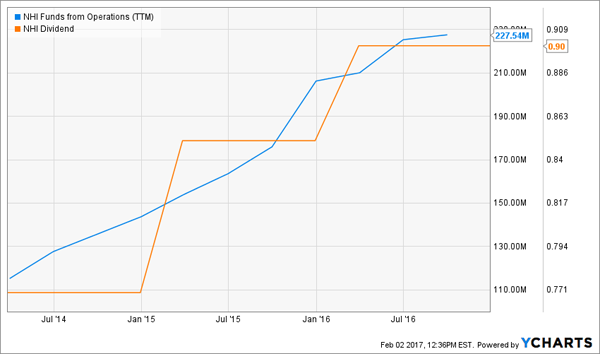

When it comes to REITs, the key figure is funds from operations (FFO), not earnings. And a surge in FFO—as demand for the facilities NHI finances marches higher—has been the driving force behind both the soaring share price and the payout growth.

Surging FFO Launches NHI’s Dividend

I fully expect that to continue, thanks to demographics: roughly 10,000 Americans turn 65 every day, and that will fuel soaring demand for senior care in the years ahead. NHI, with a presence in 32 states, stands directly in the way of that trend.

Investors, for their part, can look forward to February pay raises for years to come. The dividend currently represents 73.2% of normalized FFO, a very manageable level for a REIT. NHI is also attractively priced at just 13.3 times trailing-twelve-month normalized FFO. Buy this one and tuck it away for the next 20 years.

WYN: Another Yield-and-Growth Play

Wyndham Worldwide (WYN) also offers an above-average yield—2.5% vs. 2.1%, on average, for the S&P 500—and strong dividend growth: in each of the past three Februarys, WYN has delivered a fat 20% dividend hike. Can it keep up the pace?

I wouldn’t bet against the hotel chain, because the earnings behind that payout growth keep arcing higher:

The company’s payout ratio has also held steady at just 28%, despite the fact that it’s more than doubled its dividend since 2011.

(Wyndham is the world’s fifth-largest hotel chain by revenue, with more than 7,900 hotels and 112,000 vacation-rental properties worldwide.)

The hotel business is competitive, but WYN’s more than holding its own, thanks in part to its popular loyalty program, which lets customers rack up points fast, thanks to the company’s huge number of properties.

The Street sees more strong earnings growth ahead, with analysts forecasting EPS of $6.25 in 2017. That bodes well for more big payout hikes. Plus WYN is cheap, trading at just 12.7 times this year’s EPS forecast. Check into this one now.

A Screaming Bargain

All 4 of these stocks are great buys now. Problem is, even with their incredible dividend growth, their lower current yields mean they won’t be much help if you want to build a retirement portfolio that lets you live on dividends alone.

That’s where my new “No-Withdrawal” retirement portfolio comes in. The 6 bargain-priced investments it’s built on deliver safe yields that double up, triple up—and even quadruple up—those of your average S&P 500 stock.

These income powerhouses yield a safe 8.0% on average, so a relatively modest $500,000 nest egg would hand you a nice $40,000 yearly income stream!

Click here to discover my full strategy and get my 6 best buys for a safe 8.0% average yield now.