A few weeks ago we discussed how you can make 12% annually, forever, from stocks. Now let’s apply those lessons to 2017, and highlight five that should do even better (17%+ returns) this year (and likely beyond).

Remember, projecting our returns from any given stock is simple. We simply add together the three ways it can pay us:

- Its current dividend.

- A future dividend hike.

- Share repurchases.

It also helps if the stock is inexpensive, as buybacks deliver more bang for management’s buck. So let’s stick with stocks that are dirt-cheap, trading for 10-times free cash flow (FCF) or less for this exercise.

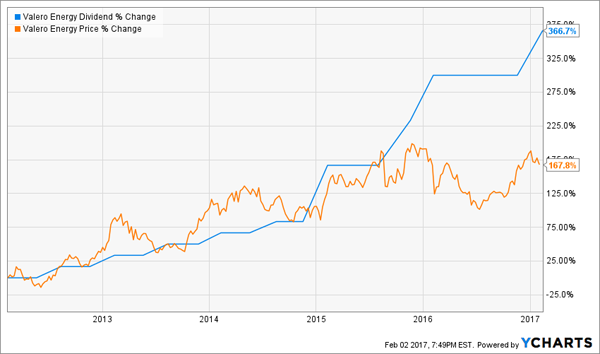

Here’s an example of a stock ready to return 17% or more over the next year. Blue chip refiner Valero (VLO) has a great management team that knows how to make money no matter what happens with energy prices.

Over the last five years the company has increased its free cash flow (FCF) by 115% per share while rewarding investors with a cumulative 300% dividend raise, even as oil prices were chopped in half:

A Free Cash Flow Machine

Shares yield 3.6% today – that’s money in our pocket. Plus management recently raised its dividend by another 16.7%. And dividend hikes have everything to do with future returns.

Here’s why: Early next year, Valero will tee up another payout increase. It will probably be a $0.10 per share raise (in line with the last three hikes).

The company has plenty of cash to do this already. It generated $10.40 in FCF over the past twelve months, and will only pay out $2.80 in dividends over the next twelve!

A “one dime” hike would be 14%. And if Valero’s shares stand still, they’ll yield more than 4% this time next year.

But here’s the thing – they probably won’t pay 4% then because investors will bid Valero’s price up (and its yield down) in anticipation of the hike. After all, even 3% is generous today.

Which means that Valero’s share price should climb in line with its next hike. And that’s exactly what was unfolding until late-2015, when the stock “decoupled” from its dividend’s trajectory:

Valero’s Stock Due To “Catch Up”

This means Valero’s share price actually has two past dividend hikes to “catch up” with as well. The stock easily has 30% to 40% upside thanks to past, present and future payout hikes alone.

And let’s not forget share repurchases! The firm bought back 15.5% of its outstanding float over the last three years, and should continue to be a buyer of its own bargain stock.

Buybacks, by the way, are underrated as a driver of returns. When the number of shares is reduced, every “per share” metric – dividends per share, earnings, and FCF – all improve. And their increases are leveraged to the amount of stock that is bought back.

After all, if profits are flat while float is reduced by 50%, the result is a 100% increase in earnings per share! And repurchases also support dividend growth. In Valero’s case, it has fewer and fewer shares to “settle up with” every year, so it can hike its payout more than it would otherwise with a static share count.

Four More Stocks With Booming Shareholder Returns

It sounds easy to bank double-digit returns like these, but here’s the catch – in today’s expensive stock market, Valero doesn’t have much company in the bargain bin.

In fact, I count just 19 firms today that:

- Pay a meaningful current yield (2%+).

- Are growing their dividend 10%+ annually.

- Have reduced their outstanding share count over the past 12 months.

- And are dirt-cheap (at less than 10-times FCF).

Some of these dividend growers are dogs though, as their business models are being eaten alive. But a few gems are set to endure. Here’s a four-pack worthy of additional consideration.

CVS Health (CVS) runs the country’s largest drugstore chain, a pharmacy-benefit-management business and 1,100 in-store medical clinics. E-commerce websites such as Amazon.com (AMZN) may be eating into traditional retail sales, but they’re not a threat when it comes to prescription drug fulfillment.

The stock’s yield has “rallied” to its highest levels since in the past decade:

CVS Health’s Highest Yield in 10 Years

A 2.3% payout sounds modest until we add in likely 15%+ dividend growth later this year (CVS has hiked its dividend by 208% over the last five years). Plus a few percentage points worth of buybacks, and we’ve got a prescription for 20% returns.

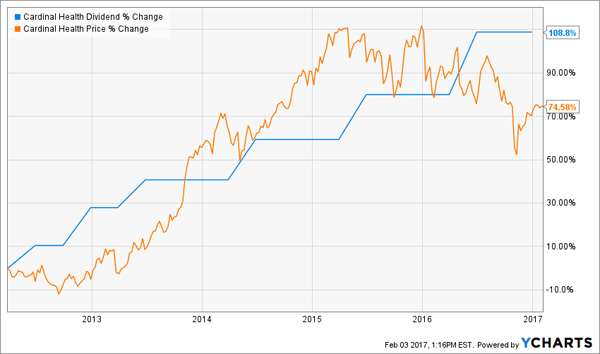

Cardinal Health (CAH) investors are also due for a big 2017. They enter the year holding shares trading for just 9.2-times free cash flow (FCF). They’ll probably receive a double-digit dividend increase in the first half of the year. And their stock price hasn’t even caught up to last year’s hike yet!

CAH Stock Price (Blue) Lags Its Payout (Orange)

Life insurer Prudential Financial (PRU) trades for just 2.5-times FCF and an equally laughable 81% of book value (or what it would be worth if it were broken up and sold off today). That’s despite the fact that, as a life insurer, it’s well positioned to profit from the three rate hikes the Fed’s planning this year; PRU invests its “float”—or the premiums it takes in—in low-risk, interest-bearing securities.

The stock pays 2.6% today, and PRU has plenty of room to keep raising its dividend with a modest 26% payout ratio. Since we first discussed this bargain last May, shares have rallied 35%. They’re still comically cheap.

Finally Bill Gross’ new home hasn’t been hospitable to shareholders after the stock’s initial “Bond King pop.” Janus Capital (JNS) sits 14% lower today than it did when the legendary bond strategist joined the firm.

But Janus has increased its dividend by 38% during Gross’ reign, and it’s due for another hike. Shares pay 3.6% today, their highest mark ever.

As I’ve said before, while buying stocks at all-time highs can be scary, buying yields at all-time highs is often a simple yet effective market timing strategy. Gross & Co. agree – they’ve repurchased 1.8% of the firm’s outstanding shares over the last 12 months.

The Sweet Spot: 7% Yields With Dividend Growth

Blue chip stocks like Cardinal Health and CVS rarely pay current yields more than 3% or 4%. They are simply too popular and likewise usually too expensive.

You’ll do even better focusing on stealth income plays such as closed-end funds, preferred shares and real estate investment trusts (REITs). In many cases, these issues pay secure yields of 7% or better – with dividend growth to boot!

This means you are assuring yourself of 10%+ annual returns, with most of that coming as cash dividends. These vehicles are safe, but they aren’t as well known as your average blue chip. And that’s a good thing for us, because we can lock up secure income streams of 7% or more while enjoying payout growth and price upside to boot.

These stealth plays are the perfect investments for 2017. Regardless of Trump’s next tweet, these 7% payers are going to become increasingly popular with retirees as they’re discovered. Make sure you buy them now, before their prices get bid up (and their yields are compressed). Click here for the details about my favorite 7% plays in funds, preferreds and REITs – and I’ll share the names, tickers and buy prices with you, too.