Today I’m going to share my favorite retirement investment with you. Even with the stock market at elevated levels, I expect it to earn me 8-10% annually over the long haul.

Last month my software company setup a 401K retirement plan through Vanguard. I had to select my funds – and that gave me instant pause. Sure, stocks for the long run… but the S&P at 23-times earnings? Europe or Asia? Roll the dice on emerging markets?

My answer was “none of the above.” Instead I piled my current and future contributions into the Vanguard Dividend Growth Fund (VDIGX) with a 100% allocation.

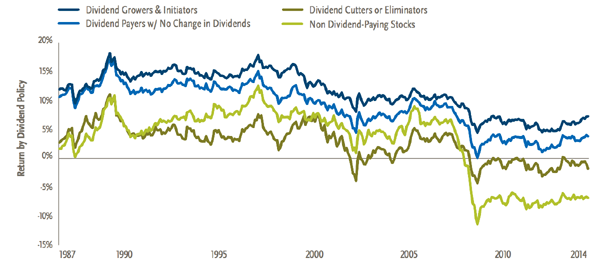

Remember, according to Ned Davis Research, 80% of the total return of the S&P 500 since 1960 can be credited to the compounding and reinvestment of dividends. And since 1987, perennial dividend growers have returned 10.1%. They’ve outperformed static dividend payers, non-dividend paying firms and dividend cutters or eliminators.

Dividend Growers Outperform, Returning 10.1% Annually

We discussed VDIGX’s cousin, the Vanguard Dividend Appreciation ETF (VIG), last year in our dividend ETF review. It was the best of the lot, thanks to the earnings power of the companies it owns. That’s why dividend growth investing tends to win over time – it buys the strongest businesses, with ever-rising profits driving ever-rising dividends.

Funds like VDIGX and VIG are good options for investors who don’t have the patience or ability to buy individual stocks. But since you’re reading this, I know you have the know-how to build your own portfolio – and secure even better returns.

It’s easy – just buy the best dividend growers when they’re trading at reasonable prices. And avoid companies that have peaked in terms of earnings power.

Here are five good ones to consider buying with 10%+ dividend growth and yields above 2.5% today. All are reasonably priced, with bullish profit outlooks for future payout increases.

5 Cheap Dividend Growth Stocks

Prudential Financial (PRU) generates gobs of free cash flow (FCF). Over the last 12 months, the firm made $14.6 billion in FCF, which is quite impressive given a market cap of only $34 billion!

The company is still atoning for its 2013 dividend cut in investors’ eyes. Management has repented by boosting its payout by 75% over this time period while reducing shares outstanding by 5.4%.

The company’s focus on retirement solutions should serve it well as baby boomers increasingly hang it up, with 10,000 turning 65 every day. A 23.6% payout ratio leaves Prudential’s dividend plenty room to run. And the stock is cheap, trading for just 69.3% of book value. “Pru” shareholders don’t need much, if any, growth to get rewarded handsomely.

WEC Energy Group (WEC) is the leading electric and natural gas utility in the Midwest. The company has grown its dividend an amazing 330% over the last 10 years, and its total stock return hasn’t been far behind:

330% Dividend Growth Drives 300% Returns

WEC generates more than 99% of its profits from regulated operations, which means they’re protected even if energy prices fall again. Multi-year infrastructure projects will help the utility grow earnings at 5-7% annually beyond 2016 – twice as fast as many of its peers, illustrating why WEC is one of the only utilities in the U.S. worth owning right now. Its 3.3% yield will double again in the next decade or so.

Trinity Industries (TRN) rode the American oil boom up and back down. The company outfits railcars for shipping crude by rail. And while the firm’s stock price has completed a “round trip” up and down over the past five years, it’s steadily grown its dividend the entire time:

Dividend Growth Through Boom and Bust

Trinity’s yield started small but is now a respectable 2.6%. Even with low energy prices, the company is still profitable – and its stock is cheap at less than 10-times earnings.

Company insiders agree that shares are a bargain. They’ve purchased nearly 170,000 shares for their personal accounts over the past three months.

BB&T (BBT) is a community bank with wide reach – 2,137 financial centers in 15 states plus Washington, D.C. Shares pay 3.4% today and management loves giving cash back to shareholders, raising its dividend by 75% over the last five years.

The stock is cheap, trading for just 1.04-times book value. Which means when you buy shares in BB&T, you’re buying its portfolio at just 4% above market value – and getting the rest of the bank and its growing dividend stream for free.

BB&T’s earnings have been flat for the last three years, but rising interest rates could be the catalyst that sends share prices – and the dividend – even higher.

Finally “cloud computing” real estate play CoreSite Realty (COR) recently reported 34% growth in funds from operations (FFO) per share for the first quarter of 2016 versus the same time period a year earlier.

CoreSite has the “Internet of things” (IoT) trend working in its favor. The more devices that connect online, the more data centers get built – which the firm builds and leases.

This breakneck FFO growth flows right into our pockets as shareholders in the form of dividend growth. Shares pay 2.7% today, but more importantly, the dividend is growing by 20% annually. And shares trade for a reasonable 20-times cash flow.

My Sixth Pick Will Raise Its Dividend 20 Times in the Next 5 Years

My favorite dividend grower yields a sky-high 7% and this dynamic outfit raises its dividend every quarter, so you only have to wait three months for the next hike.

And just like these five, the shares are cheap right now, trading at just 10 times cash flow.

What’s driving that growth? A trend that oil prices, a Chinese economic meltdown or even a President Trump couldn’t change: the graying of America.

This company provides direct nursing care to older Americans—and their numbers are exploding, with the 65+ population set to double and the 85+ population poised to triple in the years ahead.

That’s fueling skyrocketing demand for healthcare services. By 2024, national healthcare expenditures will hit $5.43 trillion.

This well-run company is in the “sweet spot” and it’s growing its already-big 7% dividend literally every 3 months. Plus, thanks to its bargain valuation, the stock has easy 20% upside from here, or better.