Forget fixed income – it’s dead, at least as we knew it. It is still possible to earn secure, meaningful yields – with price appreciation to boot – but it requires a new-look portfolio.

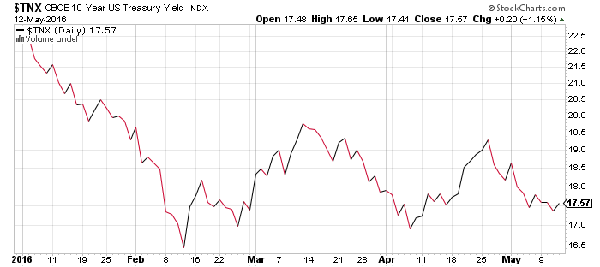

Interest rates have languished below 2% virtually all year long. We started off at 2.27% and it’s fallen steadily as the year presses on. Now hovering in the 1.75% range, there’s not a lot of profit to be had in conservative investments.

Luckily there are some select stocks that offer both growth potential as well as healthy dividend yields. If you’re looking for income, sell your Treasuries and buy these issues instead. Here are five stocks paying 3.3% or better, with upside to boot.

American Railcar Industries (ARII) is a $762 million designer and manufacturer of hopper and tank railcars that’s been trading between $38 and $45 per share all year long. A rising auto manufacturing sector is good news for the railroad industry which has been fighting headwinds from lower coal production – a major source of freight for the rail roads. Right now it trades very cheaply at just 10.5 times earnings while long-term EPS growth estimates are over 10%.

Based on full year estimates, this stock could easily rise to $45 per share or more representing a gain of about 15%. On top of that, the beefy dividend yield of 4.2% along with its incredibly low payout ratio of 27% means American Railcar can easily keep up its dividend commitment with plenty of room to boost it down the line.

Sometimes it pays to pick up a stock that’s already demonstrated a winning track record. Take Consolidated Edison (ED), a diversified utility company that can trace its roots all the back to Thomas Edison. It’s up more than 17% year-to-date.

Despite the slight miss for 1st quarter earnings, management reiterated its full year guidance of $3.85 to $4.05 per share. That gives the stock a fair value of about $82 per share – an 11% gain. The company’s announcement of a common share offering, normally an action that hurts a stocks price through diluting outstanding shares, is actually having the opposite effect.

Con Ed plan to use the proceeds to reduce short-term debt and purchase an interest in a gas pipeline puts the company a step ahead of its peers – which lack these types of growth catalysts. Con Ed’s healthy dividend yield of 3.6% is an additional bonus to investors who are looking to capitalize on this utility growth play.

If you’re looking for an undervalued stock that has nowhere to go but up, look no further than MetLife (MET). This $48 billion life insurer trades at just 9.5 times earnings while long term EPS growth is estimated at around 11% making it a value superstar. Throw in a book value that’s nearly 150% the stocks current price and a chunky 3.7% dividend yield and you get the ingredients for the perfect turnaround story. Estimating a fair P/E and full year earnings guidance, this stock is easily worth $52 per share representing a 21% gain.

Low interest rates haven’t helped the company’s life insurance investment portfolio’s profits. But a recent Federal ruling excluding the company from the list of “too big too fail” institutions and a spin-off of MetLife’s retail segment could help propel this stock higher over the next several months.

The auto industry is one of the few industries in the US that’s showing very strong bullish signals and Ford Motors (F) is set to take advantage. Consumers purchased a record 1.5 million automobiles in April, breaking the old record held since 2005 with trucks and SUV’s leading the way. Low gas prices have helped sales and reinvigorated the auto industry as evidenced by last year’s record of 17.5 million vehicle sales – a trend that looks to continue this year as well.

The stock trades very cheaply at less than 7-times earnings and the company reported stunning first quarter results beating the analysts estimates by 43%. The hefty dividend yield of 4.5% makes this stock a great pick up for value investors as well. As sales keep climbing, this stock could easily hit $18 per share by the end of this year – a 38% gain.

One company that could surprise investors this year is The Cato Corporation (CATO). The $1 billion apparel retailer reported disappointing same-store sales figures for April, but that could present an opportunity for investors. With no debt and a relatively small market cap, this company could easily be a takeover target for a larger competitor.

The stock trades at 15-times earnings – less than its industry average. It carries no debt, short term or long term, to speak of making it very agile during difficult economic environments. The dividend yield of 3.3% gives investors an additional bonus as well. Based on full year earnings, this stock could easily be valued at $40 per share – a 14% pop.

And Three Funds Paying 8% or Better With 7-15% Upside

Right now there’s an anomaly with a certain type of publicly traded fund. They own high quality assets like Australian government bonds and blue chip infrastructure stocks – but they’re trading at double-digit discounts to their net asset value, or the price their actual holdings would fetch if sold today.

The result? Three secure issues that pay 8%, 8.4% and 11% annual dividends, with 7-15% additional upside thanks to their big discount windows. They’re a backdoor way to buy the best dividend-paying issues on the planet at a “free money” discount.

I don’t expect this anomaly to last for long, so I’m encouraging my subscribers to load up their portfolios with these high-paying issues while they’re still so cheap. You should do the same. Click here and I’ll give you the names, tickers and descriptions of these high yield investments.