Groucho Marx famously said: “I refuse to join any club that would have me as a member.”

When it comes to dividends, the 10% Club isn’t usually a badge of honor either. That’s because bigger isn’t usually better when you’re talking about dividend yields.

The FOMC has targeted short-term rates of between 1.75% to 2.00% in the U.S. and the yield on the benchmark 10-year note is hovering around 3%. Almost any other income investment can be priced based off these rates, depending on how much extra risk you’re willing to take on.

Historically-speaking, any time a stock is paying more than seven percentage points above the AAA-rated, government-secured debt, investors begin to question if the dividend is sustainable.

However, not all dividends in the 10% Club are too good to be true. The mission behind Contrarian Outlook is that financial markets aren’t always efficient in the near term and buying opportunities are regularly created, if you know how to look for them.

I’ve found three stocks with double-digit yields that generate the cash flow to cover those lofty dividend payments. In addition, there appears to be room for investors to further gain through either future payout increases or when the market realizes that such a large risk premium isn’t necessary.

Alliance Resource Partners (ARLP) is a coal limited partnership and the industry receives intense regulatory scrutiny, no matter who’s calling the shots in Washington. That said, the company is the largest operator in the Illinois Basin, where the product naturally burns cleaner for the amount of energy that’s created.

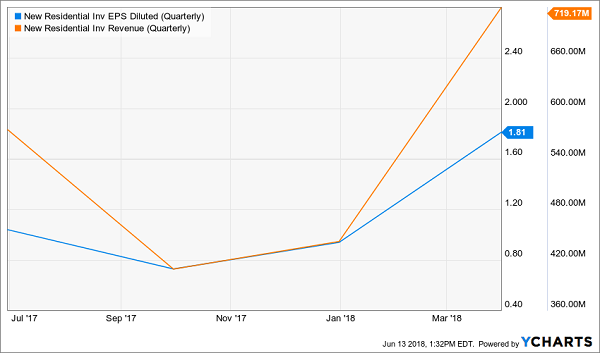

Stock Has Recovered and Still Yields Over 10%

In the meantime, the stock offers investors a rare opportunity. Alliance pays a 10.2% dividend yield and management has actually boosted the payout four straight quarters. In addition, the company has been reducing debt and recently pledged to buy back $100 million worth of shares.

Alliance earned $0.56 a share in the first quarter, which covered the quarterly distribution 109%. Consensus profit expectations have also moved up 3% in the past few months, as management is expanding the business by exporting more coal outside of the U.S.

The company is covering its dividend with room to spare, which gives management room to keep increasing the payout. This appears to be one name in the 10% Club worth owning.

Next up is Global Partners (GLP), which is a master limited partnership that transports and stores oil, natural gas and other refined energy products in the Northeastern U.S. The company also operates over 700 retail gas locations that stretch from Maryland up to Maine.

Global Partners did cut its dividend in early 2016 as energy prices wallowed, but time does heal some investor wounds. The company traces its roots back 75 years and has weathered several different energy price cycles.

Earnings Again Support Dividend

Excluding one-time items, management generated distributable cash flow of $0.86 a share in the first quarter, which was enough to cover the quarterly dividend (10.8% yield) nearly two times over. Global Partners saw record volume in the period, driven by wholesale demand. The company is also expanding its retail gasoline presence through acquisitions that are expected to boost near-term earnings.

Like several members of the 10% Club, Global Partners has some skeletons in its closet. Even so, the business appears to have stabilized along with energy prices and management can consistently cover the dividend.

New Residential Investment (NRZ) is a real estate investment trust my colleague Brett Owens touched on last year that focuses on mortgage servicing rights (MSR). Like Alliance Resource, the company’s yield is growing for the right reasons, as management has increased the quarterly dividend (11.1% yield) five times since 2015.

Traditional banks have been moving MSRs off the balance sheet to free up capital, which has created the opportunity for firms like New Residential to grow. By nature, MSRs should rise in value along with interest rates, as mortgage prepayments and refinancings decline.

Growth Leveraged to Rising Rates

New Residential had core earnings of $0.58 a share in the first quarter, which exceeded the consensus analyst estimate by $0.03 and covered the quarterly dividend 116%. The company also grew its book value by more than 10% in the period, given its leverage to higher interest rates.

The market is trying to catch up with New Residential’s earnings power, as consensus profit estimates have risen 3% in the past quarter. I believe this could signal another dividend increase soon.

Like Groucho Marx, there aren’t many dividends in the 10% Club that you want to associate with either.

A stable dividend yield of 10% is nice, but growth is the name of the game, especially if interest rates continue to rise.

If you can “forego” that allure of higher income today, you’re likely much better off if you consider investing that capital into dividend growers.

It’s a simple three-step process:

Step 1. You invest a set amount of money into one of these “hidden yield” stocks and immediately start getting regular returns on the order of 3%, 4%, or maybe more.

That alone is better than you can get from just about any other conservative investment right now.

Step 2. Over time, your dividend payments go up so you’re eventually earning 8%, 9%, or 10% a year on your original investment.

That should not only keep pace with inflation or rising interest rates, it should stay ahead of them.

Step 3. As your income is rising, other investors are also bidding up the price of your shares to keep pace with the increasing yields.

This combination of rising dividends and capital appreciation is what gives you the potential to earn 20% or more on average with almost no effort or price momentum investing at all.

Which “hidden yield” stocks should you buy today? Well you know us – we’ve got seven best buys that should safely double your money every three to five years.

It’s a simple formula – their dividends are doubling every three to five years, which means their prices will rise in tandem. At the same time, we’ll collect their dividend payments today and enjoy an even higher income stream tomorrow.

This dividend growth strategy has produced amazing 25.3% annualized returns for our Hidden Yields subscribers since inception. In two-plus years, we’ve crushed the broader market (the S&P 500 returned 15.9% over the same time period.)

If you achieve returns of 25.3%, you’ll double your money in less than three years. So if you haven’t been following this strategy, why not? The best time to get started is right now – before the seven dividend growers we mentioned begin to move. Click here and we’ll share their names, tickers and buy prices with you right now.