The Wall Street Journal reports – yet again – that stock picking is dead. We’re being told that passive index funds outperform actively managed funds over the long term, and smart investors should choose passive because actively beating the market isn’t possible.

On one level, this is true. If your plan is just to buy and hold for 30 years or more, and if you don’t need any income right now, you are probably better off with a low-cost index fund than a higher-cost actively managed fund. But what if need income NOW? Then the “wisdom” of passive investing isn’t so great, and you need to consider alternatives.

Let’s look at two passive S&P 500 funds, the SPDR S&P 500 ETF (SPY) and Vanguard’s alternative, the Vanguard 500 ETF (VOO). First you’ll notice the dividends on these funds are awful:

Low Yields, High Risk

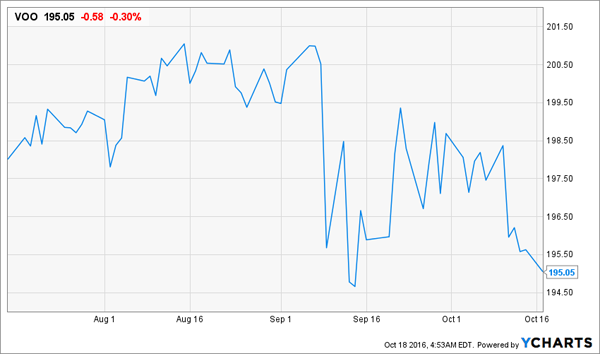

A measly 2% income isn’t going to cut it for most retirees, especially when these funds can (and have) fallen by 10% or more in the span of a few months. Just ask anyone who owns low-cost (and low-return) VOO:

Start of a Downtrend?

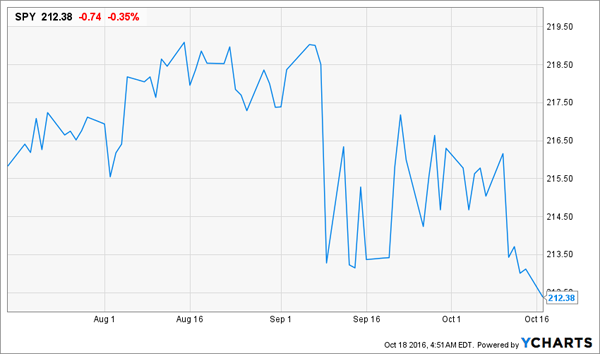

You already lost 2.8% if you bought at the top over the past 3 months. The same goes for SPY:

Look Familiar? Index Funds Drop

Stock prices are precarious right now, to say the least. The market predicts a 70% chance of the Federal Reserve raising interest rates in December. When interest rates go up, risk-averse investors (who are increasingly becoming part of the stock market itself thanks to passive index funds) will shift towards U.S. Treasuries and away from widely owned stocks. This is especially true if they’re looking for dividends. The iShares 20+ Year Treasury Bond ETF (TLT) is already yielding more than the stock index funds—and with less risk:

Bond Yields Beat Stocks, At Last

Does this mean we should buy U.S. Treasuries? Alas, no, because they’re also at risk with a rate hike. So where can we go?

There is a great alternative to SPY and VOO that has many of the characteristics risk-averse investors should love. The fund pays a dividend of 7% and provides less exposure to stock downturns than the index funds. Also, the fund is selling at a discount of 9%, meaning you’re buying $1 of stocks for about 91 cents.

The fund is the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) and it’s unique in that it provides exposure to the S&P 500 but always sells call options on those stocks to provide a higher rate of income. This is extremely good if you need income right now and you’re (rightly) worried about a stock market correction coming in the wake of the Fed’s rate hike.

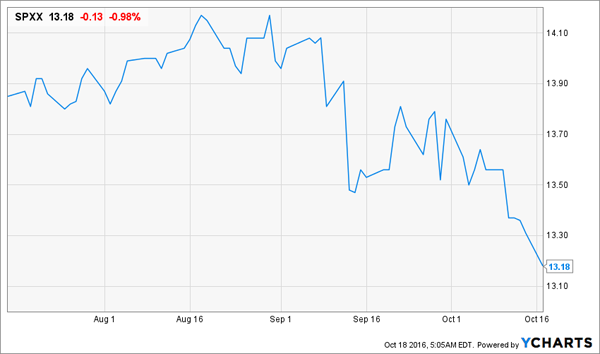

You could stagger purchases in this fund over the next few weeks and take advantage of its dividend payouts while also getting some limited exposure to the market as a whole. We are already seeing the fund being sold in a panic (further widening its discount):

Fear Driving Investors Away

We want to run against the herd and buy this fund because of the discount. But if SPXX is so great, why aren’t more people buying it? There’s one simple answer: the fear of fees. The fund’s total annual expenses are 0.92%, whereas VOO’s annual expenses are 0.05%. This is something passive investors love to focus on—look, you’re paying 18.4-times as much in fees as I am!

But what does that mean in actual hard dollar terms? A $500,000 investment in VOO will have annual fees of $250, versus $4,600 in annual fees for SPXX. That sounds like a very big difference, but remember that those fees are taken out of the fund before distributions—you don’t get a big bill that needs to be paid out of pocket. Most people don’t even notice the fees at all (which is partly why ill-managed funds get away with charging fees of 2% or more).

But will these fees drag on performance? The answer is yes and no. Over the long term, yes, it will, as we can see from this chart:

Total Returns for VOO and SPXX

But notice how there are moments of great divergence between VOO’s and SPXX’s total returns – and how that divergence is greater now than it has been in a long time.Shortly after those divergences, SPXX tends to revert to VOO’s trendline—and sometimes even outperforms VOO.

That’s why now is a terrible time to buy VOO but a great time to buy SPXX. It will revert to VOO’s trendline, meaning it will recover more sharply than VOO whenever the market begins to recover. And if you buy SPXX now and wait for that recovery, you’ll also be getting a dividend of over 7%.

The divergence between SPXX, and its inevitable recovery, hasn’t been happening just relative to VOO. Let’s look at another low-cost Vanguard favorite—the Vanguard Total Stock Market ETF (VTI):

Notice a Pattern?

Again we see the same thing—a sudden massive divergence in SPXX performance relative to VTI, which has been followed by an inevitable recovery in SPXX bringing it in-line with the broader stock market. Those who buy those dips tend to outperform.

And that brings me back to the fee issue. Sure, you could buy VOO and save yourself $4,350 in extra fees for a $500,000 investment. However, people who buy SPXX on dips get more than just that 0.87% in capital gains in a very short time period, as we can see by looking at what happened in February and March this year:

Buying on Dips Means Huge Upside

We got a return of over 3% if we bought during the February jitters. That’s $17,150 on our $500,000 investment, or about 4 times more than what the passive indexers were saving. Plus, our high income stream means we don’t need to sell stocks from our portfolio during the market downturn, meaning we don’t have to worry about locking in our losses.

Most investors avoid locking in their losses by saving more—so instead of needing $500,000 to retire, they need $1.75 million to retire. Which means working more, and saving more, and waiting more.

If you don’t want to work, save, and wait, you don’t have to—but you do need to be a bit more aggressive and, well, less passive in your investing. This bold step of “second-level thinking” can produce a No Withdrawal Portfolio that provides enough income so that you never need to worry about selling during a market downturn. It takes a bit more research and time, but it’s well worth the effort if it means knocking off over $1 million on the capital you need to retire!

SPXX is just one step in building this portfolio. There are additional funds and stocks you can use to diversify across sectors and asset classes and further insulate yourself from market volatility. Click here to read more about creating your own No Withdrawal Portfolio, and how to find funds paying 8% dividends with capital gains upside that will increase your nest egg even more.