The way to protect your portfolio isn’t large caps–it’s large yields. And the very best ones often come in small packages, such as the three “underappreciated dividends” yielding up to 15% that I’m about to show you.

I’m talking about funds that pay big, secure dividends. When pullbacks happen, these funds’ prices don’t move thanks to their yields. After all, a 15% annual payout (like the one we’re going to discuss shortly) buffers your portfolio against plenty of market volatility.

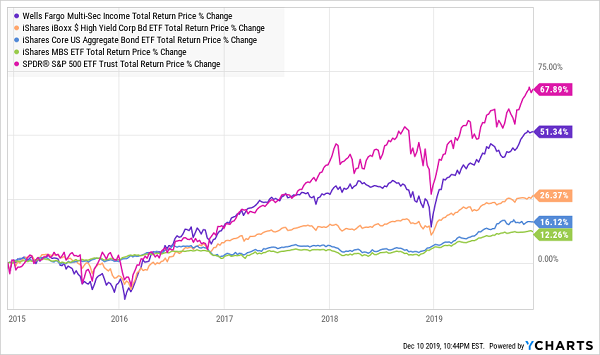

Here’s an example. Let’s consider Wall Street’s temper tantrum from late 2015 to early 2016, which greeted our launch of the Contrarian Income Report service focused on dividends that are big enough to retire on.

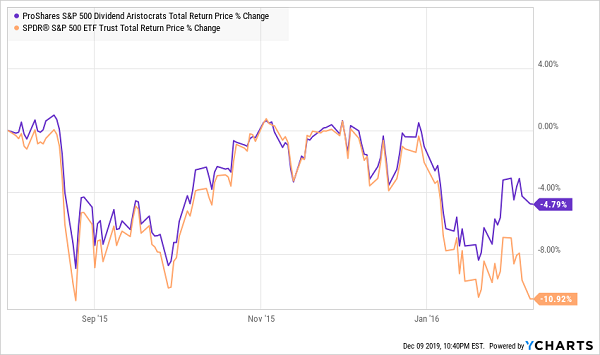

During this stock-market correction the S&P 500 lost more than 10% in six months. And the Dividend Aristocrats (blue chip stock that have raised their payouts every year for the last 25) provided far less protection than you might have expected:

Not Much Pullback Help Here…

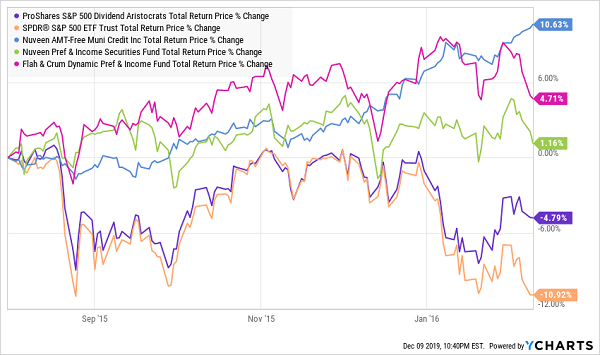

But while tried-and-true Aristocrats such as W.W. Grainger (GWW) and Stanley Black & Decker (SWK) were submerged, our more generous dividends had their heads above water. Indeed, if our subscribers had simply paid attention to their portfolio returns and somehow skipped the daily news, they might have missed the market’s fit altogether!

… But Our Big Dividend Payers Barely Blinked!

Check out the green, pink and blue lines above: These rarely covered bond holdings not only kept churning out their 7% annual dividends but generated 5%-plus returns in six months while stocks were busy correcting.

I’ve never seen a single one of these funds touted on CNBC or Fox Business, but these sneaky super-yielders have delivered 10.6% annual gains to subscribers since inception, most of which has been in the form of cold, hard cash.

Let’s dive into a trio of massive yields that come in small, hidden packages. These relatively secretive income picks dish out between 9.3% to 15.0% annually like clockwork, making them powerful, potentially pullback-proof plays.

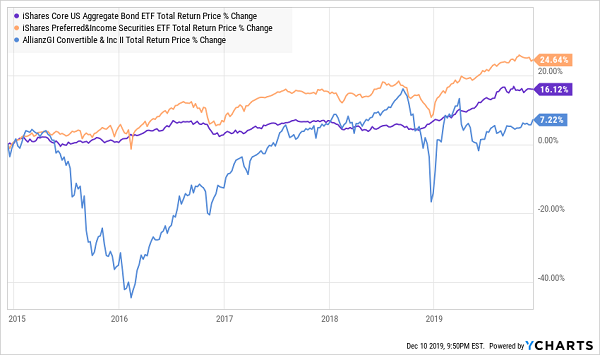

AllianzGI Convertible & Income Fund II (NCZ)

Dividend Yield: 10.8%

AllianzGI Convertible & Income Fund II (NCZ) is a fixed-income fund that aims to invest at least half its portfolio in domestic convertible securities, with the rest in good, old-fashioned high-yield bonds.

How much ultimately goes into convertibles—typically corporate bonds or preferred stocks that can be converted into common stock—depends on various market factors. That decision falls upon an experienced management team, with every member on board for at least a decade.

The portfolio currently is split 60-40 between convertibles and high-yield bonds. At the moment, top holdings include the likes of a 7.5% preferred series from Wells Fargo (WFC), a 6% preferred from Sempra Energy (SRE) and an 8% preferred from chipmaker Broadcom (AVGO).

Clearly, AllianzGI Convertible & Income Fund II’s portfolio has a high yield base as it is. But as a closed-end fund (CEF), NCZ’s management can crank up its distribution into the 11% realm by applying a hefty 30% in leverage to boot.

That hasn’t helped in recent years, unfortunately. While the fund’s longer-term performance is admirable, the past five years or so have been less than stellar, with NCZ struggling to keep up with basic ETF bond and preferred-stock benchmarks.

AllianzGI Convertible & Income II Looks Clunky Lately

The CEF does trade at a thin, but rare, discount to its net asset value (NAV) at the moment. But I want to see if NCZ’s management can right the ship again first.

Let’s move on.

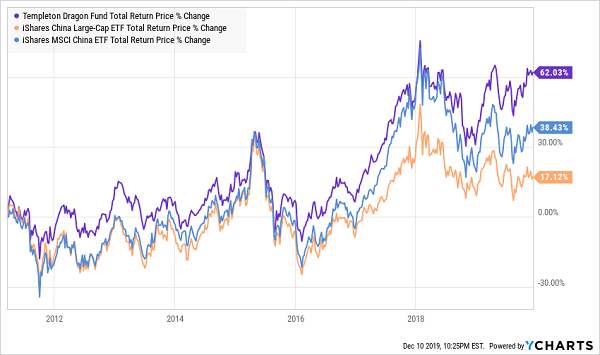

Templeton Dragon Fund (TDF)

Dividend Yield: 15.0%

The Templeton Dragon Fund (TDF), as the name alludes to, is a rare China-focused fund in the CEF space. Most of the portfolio (83%) is invested in mainland Chinese stocks, with another 8% in Hong Kong equities and the rest in companies HQ’d in Taiwan.

A quick look at the innards reveals a pretty standard Chinese portfolio, albeit a concentrated one. E-commerce giant Alibaba Group (BABA), tech conglomerate Tencent Holdings (TCEHY) and chipmaker Taiwan Semiconductor (TSM) alone make up a quarter of TDF’s weight. That said, financials, such as AIA Group (AAGIY), make up the largest part of the fund at 25% of assets.

There’s nothing novel here. Just strong management. Yes, the trade war has been a doozy for anyone trying to invest in China, but TDF has done it better than most. Not only does it beat most China-focused ETFs handily, but at 1.33% in annual expenses, it’s decidedly on the inexpensive side for a CEF. It trades at a steep 12% discount to NAV, though that’s a pretty typical discount for Templeton Dragon.

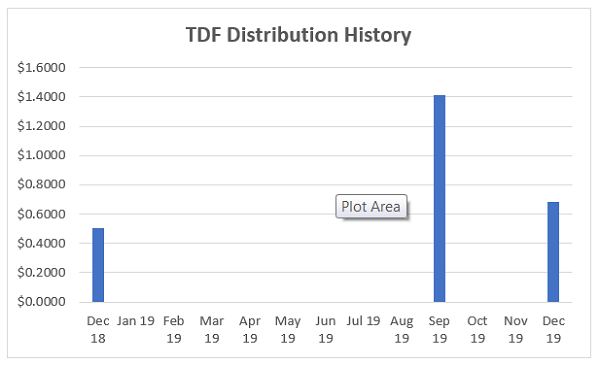

The only fault to find with TDF—and it’s not a small one—is that the sky-high distribution is extremely uneven, with no real pattern to when it pays. In other words, while it’s a fantastic fund, this isn’t the kind of holding that will keep you in dependable income on a regular schedule.

Data Source: CEF Connect

This is too erratic for a retirement portfolio.

Wells Fargo Multi-Sector Income Fund (ERC)

Dividend Yield: 9.3%

The Wells Fargo Multi-Sector Income Fund (ERC) is a bit misleading. That is, you’re not going to be invested in, say, utilities, tech stocks and health-care companies. The multi-sector moniker refers to the three fixed-income “sleeves” it invests in: 30%-70% high-yield corporate debt, 10%-40% foreign debt and 10%-30% adjustable-rate and fixed-rate mortgage-backed securities (MBSes) and investment-grade corporates.

Right now, more than half the fund is in corporates, with most of that allocated to junk. The rest is dispersed across foreign government bonds (17%), loans (14%), “Yankee” corporates and notes (6%) and a peppering of other debt.

This fund is a strong fixed-income candidate. It’s never going to beat the market when it’s in full bull mode, but it’s able to crush most standard fixed-income benchmarks.

And, unlike TDF, it’s much more a model of what you want from a retirement fund: monthly distributions—the best for planning around your monthly obligations—and uber-high yield to boot.

Just exercise patience. ERC has averaged a nearly 10% discount to NAV over the past five years, and has traded as cheaply as 83 cents on the dollar within the past year. But it’s relatively expensive now, at just a 4% discount.

I would wait for a wider discount window before considering this fund.

Never Fear a Pullback Again: “2008-Proof” Stocks With 7.5%+ Yields, 10%+ Upside

This is no time for “but” funds.

You know. “It’s a great fund, but …”

We’re in the back half of a bull market that’s too long in the tooth for comfort, and global risks are piling onto still-climbing but still-fragile stocks.

So even mammoth yields like the ones above aren’t really worth all that much if they don’t provide every last thing you need to protect, and grow, your hard-earned nest egg, rain or shine.

That’s precisely the inspiration behind my 5-stock “2008-proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver two things most “blue-chip pretenders” don’t:

- Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure a safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “2008-proof” plays might have wondered what all the fuss was about!

These five “2008-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out, with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.