It’s actually easy to find dividend stocks that yield more than 5%. No, really. You can go to a screener like the one at FinViz.com and actually search for dividend stocks that yield more than 5%. As of right now, about 450 stocks hit that bar.

But that’s merely a list – a list that more closely resembles a minefield.

Buried in that list of high-yield dividend stocks is a horde of time bombs. These are stocks that threaten your hard-earned nest egg in any number of ways.

Some of these big yields are simply a result of big stock losses, which in turn are a reflection of deteriorating financials that could lead to payout cuts or suspensions in the future. In fact, in some cases, these stocks are paying out far more in distributions each quarter than they earn! That’s what happened over the past year as dwindling oil and gas prices forced the hand of numerous energy stocks, whose profits simply couldn’t support their lofty payouts.

Still more of those yields come from international stocks, which have their own sets of asterisks to deal with. Many internationals pay out sporadically, and even those that pay, say, a regular annual payout don’t offer consistent baselines that rise over time, so one year’s cash explosion could turn into a subsequent year’s dud. And the dividends you do get typically are subject to double taxation – both U.S. taxes, as well as foreign-tax withholdings.

In truth, there’s a very limited group of stocks that not only offer high yield, but enough assurances that the dividend will actually be around in future years.

Today, I want to show you a group of three such stocks. Each of these companies yields 5%, and importantly, they’re not stretching fiscally to make those regular distributions.

Tupperware (TUP)

Yield: 5.1%

Payout Ratio (Earnings): 63%

Tupperware (TUP) doesn’t boast quite the same level of blue-chip cache as consumer dividend stalwarts such as Johnson & Johnson (JNJ) or even Sherwin-Williams (SHW), but it’s still a very well-known brand name that’s still managing to find its way in the world.

And at a yield of more than 5%, it’s got at least one leg up on JNJ (2.8%) and SHW (1.2%).

Moreover, Tupperware isn’t straining too hard to make its 68-cent quarterly payout. Currently, TUP shares’ dividend represents less than two-thirds of its earnings estimates for the current fiscal year, which is well within the realm of safety. The figure actually drops to 60% when you look at projected earnings for 2017.

Tupperware isn’t without its issues, however.

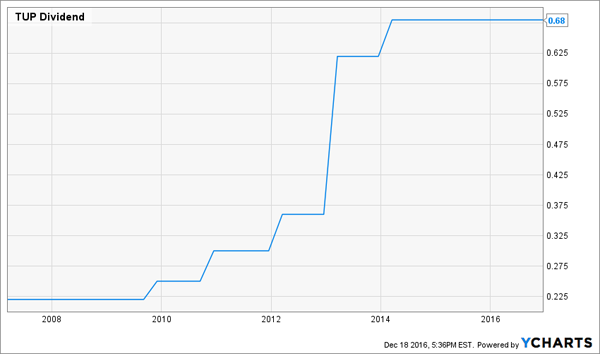

A Payout Plateau

That straight line you see above is a flattening of Tupperware’s quarterly dividend. The payout has been frozen at 68 cents per share since 2014, which means investors haven’t seen an increase in about two years.

Perhaps not coincidentally, that has come in tandem with shrinking revenues and net income; sales are on pace for $2.23 billion, off 17% from three years ago; adjusted earnings should fall about 20% to $4.32 per share. That has come in part thanks to Newell Brands’ (NWL) Rubbermaid, which has aggressively ramped up its own storage solutions over the past few years.

The flip side? TUP has fought back by expanding its offerings to include things such as its Quick Chef Pro system – a manual food processor that can chop vegetables, make salad dressings and accomplish other kitchen tasks. And Tupperware is stemming the bleeding, with analysts predicting slightly higher sales next year and a return to substantial profit growth.

Iron Mountain (IRM)

Yield: 6.9%

Payout Ratio (AFFO): 75.6%

Iron Mountain (IRM) sits on one of technology’s hottest trends of the past few years: digital storage. But while that might conjure up thoughts of “the cloud,” that’s not quite accurate. Iron Mountain offers a number of information services, which includes a heaping helping of actual physical storage of documents.

Among IRM’s other businesses? Secure shredding, providing anytime access for business data, health information management, federal records storage and document imaging.

But a tech company yielding nearly 7%?

Well, it’s not exactly a tech company anymore. Back in mid-June 2014, Iron Mountain’s board unanimously approved a conversion into a real estate investment trust (REIT), with CEO William Meaney saying at the time that “this structure enhances our ability to sustain our durable, high-return storage rental business.”

It also enhanced Iron Mountain’s payouts. Starting in 2013, before the conversion, IRM offered a 27-cent quarterly dividend. With the conversion, that escalated to 47.5 cents per share, ticked higher to 48.5 cents in 2016, then ballooned to 55 cents quarterly just this month. Even then, the payout ratio is only three-quarters of Iron Mountain’s adjusted funds from operation (AFFO) – a conservative figure considering that 90% is the typical investor “worry line.”

But buyer beware: Iron Mountain isn’t exactly a cushiony ride, and while shares have been in a general uptrend since the 2008-09 market crash, it has been in nauseating fashion (despite the payout’s steady climb higher):

A Price Rollercoaster Over a Steady Payout

It’s also worth pointing out that revenues have more or less been stagnant over the past few years, showing a decided lack of growth. IRM looks like a stable, dependable payer, but incomes might be the lion’s share of your returns down the road.

Ventas (VTR)

Yield: 5.1%

Payout Ratio (FAD): 71%

Healthcare-focused REIT Ventas (VTR) plays in the baby boomer megatrend powering healthcare higher, including health-related real estate, such as assisted living facilities and medical offices. Ventas’ portfolio is heaviest in senior housing, which makes up nearly 60% of the company’s revenues. Specialty hospitals and U.S. acute care hospitals are another quarter. Skilled nursing, international hospitals and consolidated joint ventures make up the remainder.

Like Iron Mountain, Ventas also upped its dividend in December, from 73 cents quarterly to 77.5 cents, helping to push its yield above the 5% threshold. Also like Iron Mountain, its payout is within perfectly acceptable levels – instead of AFFO, though, the metric to watch is funds available for distribution (FAD).

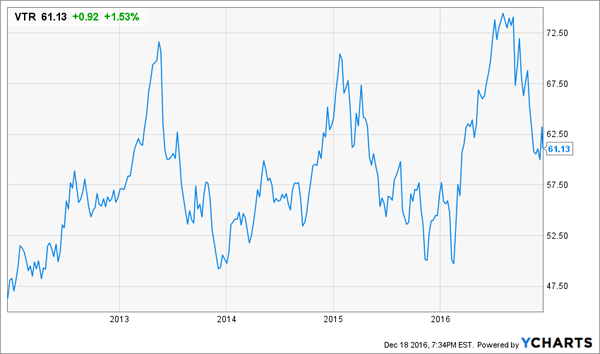

And like Iron Mountain, Ventas has been a high-yield roller coaster over the past few years:

Ventas has been a REIT in some amount of flux in recent years, thanks in part to the spinning off of 355 skilled nursing properties in the form of Capital Care Properties (CCP). Now, the plan is to rely on its core senior housing portfolio while trying to find advancement opportunities in hospitals.

VTR shares have cooled off after a roughly 50% jump out of its February lows, and that has helped bring price/FAD down – but at around 16, while it’s not grossly expensive, it’s hardly a screaming value.

But why accept 5% yields from “good enough” stocks? Heck, why even accept 7% yields if you have no faith that the business as a whole isn’t growing?

Why spend your investment funds on anything less than excellent?

There’s not much margin for error for individual investors who are trying to raise enough money to enjoy life in retirement.

I’ve done the math on it, and realistically, if you have a half-million dollars, you need to be making something around $40,000 annually – or 8% – to fund the kind of lifestyle you’d actually want to have in your post-career years. If you think Treasuries will do that for you, think again. You’re looking at more like $15,000, $16,000 every year. That’s just not good enough.

You need excellence, and I know just where you can get it.

My favorite dividend stock yields 8.5% right this minute, it raises its dividend every single quarter, and it will keep churning out income even if the market throws us a curveball or two. Tack on the projected capital gains on this sure-fire pick, and you’re looking at a total return 17% between dividends and capital gains every single year!

The stocks above definitely merit a spot on your watch list, but if you’re looking for winners to invest in right now, let’s talk.

I specialize in uncovering contrarian 8%+ income opportunities like my ever-rising dividend pick. Click here and I’ll explain more about my strategy and my favorite stocks and funds to buy for a secure retirement on $500,000.