Dividend stocks are a great way to build long-term wealth. But how do you pick the right ones—and steer clear of companies whose payouts are headed off a cliff?

You can start by avoiding the five classic blunders below. If you’ve made any of them, don’t worry. We all have. But keeping them in mind will help you stay off the rocks and boost your future returns.

- Focusing on High Yields—and Nothing Else

For many investors, buying dividend stocks is a simple matter of seeking out a high yield—above 6%, say—and hitting the buy button.

That’s the worst thing you can do, because many stocks paying out at those levels are nothing more than “yield traps”: their profits and cash flow simply can’t back up their hefty payouts.

This story typically ends with a slashed dividend, a steep drop in the share price and plenty of sleepless nights for investors who didn’t get out in time.

So how do you avoid that nightmare scenario? First, you need to go beyond yields and look at things like a company’s dividend history, its payout ratio (more on that below), cash reserves, debt levels and cash flow—all the things that go into a healthy, growing dividend.

Which brings me to Frontier Communications (FTR), a telco with a 7.9% current yield.

What’s powering that high payout? Not much, it appears. For one, Frontier ended the fourth quarter with $15.5 billion of long-term debt. That’s nearly triple its $5.7-billion market cap! A big part of that debt springs from its $10.5-billion purchase of Internet, phone and TV assets in Florida, California and Texas from Verizon Inc. (VZ), which is slated to close March 31.

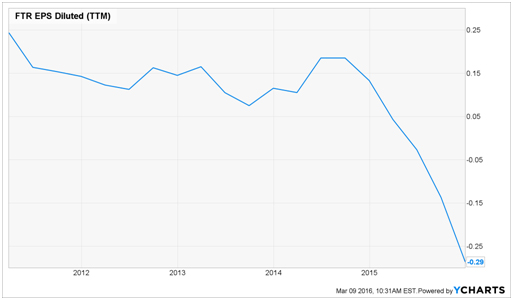

Worse, Frontier is losing money, to the tune of $0.29 a share in 2015, so it’s paying investors with cash it doesn’t have.

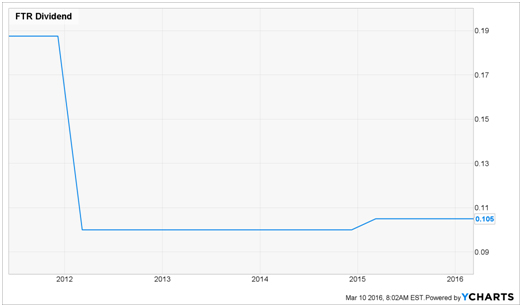

Finally, Frontier does have a history of dividend cuts, the latest one coming in 2011, when it slashed the payout by 47%—and the dividend rate has barely budged since then.

- Dismissing Stocks With Low Yields

I know it sounds counterintuitive, but it’s true: stocks with low dividend yields can be some of the best income investments you’ll find. That’s because, over the long haul, it’s dividend growth—not current yield—that matters.

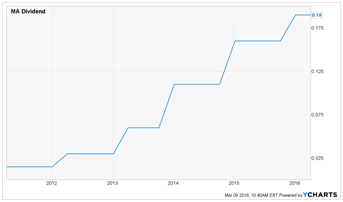

The poster child for this is MasterCard (MA), a stock that makes nobody’s “dividend hot list.” Why? Because most investors see its $0.19 quarterly dividend, which yields 0.88% on an annualized basis, and say, “What’s the point?”

In fact, a 0.88% yield would have looked huge in October 2011, when MasterCard’s yield clocked in at an almost nonexistent 0.18%.

But here’s the kicker: if you’d gone ahead and bought the stock then—a little more than four years ago—you’d already be yielding 2.31% on your original investment.

That’s because the company has boosted its payout by 1,166% in that time (adjusted for a 10-for-1 stock split in January 2014). That’s to say nothing of the 164% share-price gain MasterCard investors have enjoyed.

- Ignoring Payout Ratios

If you’re looking for one indicator of whether a dividend could grow like MasterCard’s—or drop like Frontier’s is in danger of doing—the payout ratio is it. Too bad many investors ignore this simple signal.

You calculate payout ratio by taking the amount a company spent on dividends in the past year and dividing it by net income. For maximum safety, I like to see a payout ratio of 50% or less for most stocks.

So how do our two examples stack up? Right now, Frontier is losing money, so its payout ratio is negative—a big red flag. But MasterCard boasts a payout ratio of just 19%, leaving it loads of room to keep those big hikes coming.

- Overpaying for the Stock Itself

Sometimes investors get so enamored with a company’s “story” they ignore value measures like price-to-earnings and price-to-book ratios.

They’re taking a big risk, because stocks with suspiciously high P/E ratios could nosedive if they fail to meet investors’ lofty expectations. On the flipside, while a low P/E can signal a bargain, it can also mean a business is headed for trouble, which is why investors have bid down the “P” part of the equation.

The bottom line? Like dividend yields, P/E ratios and other valuation measures should be just one part of your research—not the extent of it.

- Failing to Reinvest Dividends

Once you’ve hit the buy button, don’t hesitate to put your money to work: take those payouts and get them compounding.

A great way to do that is through a company’s dividend reinvestment plan (DRIP), which lets you use your cash dividends to buy more shares (or even fractional shares). That means your dividend will be larger in the next quarter—and you’ll get to buy more new shares than last quarter—and your wealth builds on itself.

DRIPs give you two big advantages: first, you don’t pay any commissions on the additional purchases. And second, thanks to the periodic nature of the investment, you get more shares when the stock price is lower and fewer when it’s higher.

This compounding really adds up over time. Here’s how the performance of Pfizer Inc. (PFE), a high-yielding drug stock I analyzed a couple weeks ago, looks when you stack up its 10-year return with dividends reinvested vs. share-price growth alone.

Pfizer 10-year returns with dividends invested vs. without

You won’t have to worry about dividend cuts if you pick up shares of the three high-yielders I just told my subscribers about. They tick off all my “dividend safety” checkboxes: they have sterling dividend histories, low payout ratios, and they’re trading at bargain valuations, to boot.

And unlike MasterCard investors, you won’t have to wait another five years to get a decent yield out of these stocks. They let you pocket yields of 6.9%, 7.3% and 8.9% straight out of the gate—and I fully expect their payouts to double in the years ahead.

That’s because all three provide healthcare services to a rapidly growing segment of the population, and they’re all profiting from one undeniable truth: Americans are getting older. And quickly.

There’s a silent “bull market” developing in the U.S., and it will run for at least two or three decades. Here’s what’s driving profits in the America-is-getting-older trend:

- 77 million baby boomers—28% of the US population—are turning 65 at a rate of nearly 10,000 per day.

- We’re living longer than ever before thanks to healthier choices and advances in medical technology. That means the 65+ population will double and the 85+ population will triple in the coming years.

- Americans over 65 are still three times more likely to be admitted to a hospital, and for longer periods of time and for more expensive types of care.

Like I said, I’ve just released the names of these three companies to a small group of investors, but you can still be among the first to hear about them. Simply click here and I’ll give you full details on all three of these income wonders now.