This aging bull market in U.S. stocks turned seven last month. It’s a bit expensive and past its prime for my liking. But another “niche bull run” is kicking off right now. And no matter what happens with the broader market, these issues – and their dividends – will roll higher for decades.

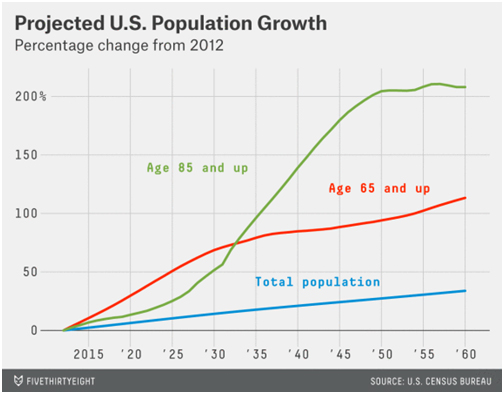

There are 77 million Baby Boomers that make up 28% of the U.S. population. Any companies that make products they buy are usually doing great. This massive generation made baby products makers rich in the 1950s, and homebuilders rich in the 1990s and 2000s.

Now, they’re transitioning their spending again. There are 10,000 boomers hitting retirement age every day. Over the past two years, more than 3 million each year have turned 65. This wave of new retirees will continue to grow every day, every year, for the next couple of decades (at least).

What do 65+ folks spend money on? Medical care and living arrangements, for starters. Let’s talk about five (actually six) companies poised to rake in big business in these markets from boomer spending.

3 Cash Cows Curing Diseases & Boosting Lifespans

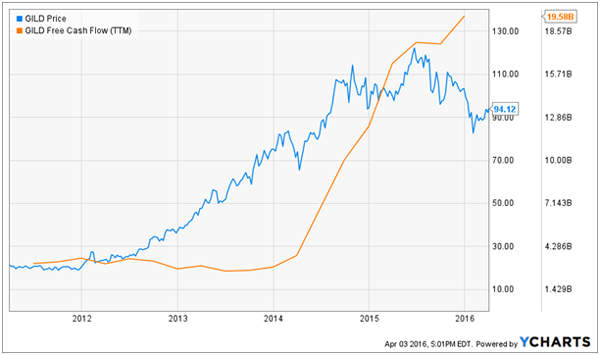

Gilead Sciences (GILD) has produced some of the biggest biopharmaceutical blockbusters over the past decade. Its hepatitis C treatment had a 90% success rate, with few side effects. It sold tens of billions of dollars worth of these drugs (Sovaldi and Harvoni) since they hit the market in 2014, with most of their profits dropping straight to the bottom line.

Gilead’s Free Cash Flow (FCF) Skyrockets Thanks to Hep C Treatments

As you can see the company’s share price has lagged its free cash flow (FCF) growth over the past year. Wall Street is worried about the Gilead’s next act, as well as jawboning from political candidates about forced price reductions in pharmaceuticals.

These worries, and more, appear to be discounted in the share price. Its stock is as cheap as ever, trading for just 7.3-times FCF. Management agrees it’s a bargain, repurchasing 7% of shares outstanding over the past year. Plus, the company initiated a dividend last year, which is well supported by a modest 14% payout ratio.

Last month, the board approved an additional $12 billion repurchase program to complement its current $15 billion effort (which is about half complete). All said these programs will remove about 15% of the current shares outstanding. Combined with the firm’s 1.8% dividend, there’s a nice floor on the stock price for an investor to wait for the next brilliant breakthrough from Gilead’s R&D department.

Thermo Fisher Scientific (TMO) is a science powerhouse. Its cutting edge equipment improves patient diagnostics and increases laboratory productivity.

Thermo Fisher sells to both the private and public sectors, and tight Congressional funding for departments like the National Institutes of Health (NIH) have weighed on the stock over the last two years. But the NIH budget just got a 6% bump, and sales to Asia are increasingly robust with China trying to clean up its dirty air and food chain.

You wouldn’t even notice these “first-level worries” taking the long view however – the firm has increased its FCF 10-fold over the past 10 years!

Everybody Loves Science – Thermo Fisher’s Booming FCF

Thermo Fisher pays a token dividend of 0.4%, but has plenty of room for increases and share repurchases. Its payout ratio is just 12%, and the company generated an impressive FCF of $2.4 billion over the past 12 months from $17 billion in revenues.

CVS Health (CVS) runs America’s largest drugstore chain, a pharmacy-benefit-management business and 1,100 in-store medical clinics. E-commerce websites such as Amazon.com (AMZN) may be eating into traditional retail sales, but they’re not a threat when it comes to prescription drug fulfillment.

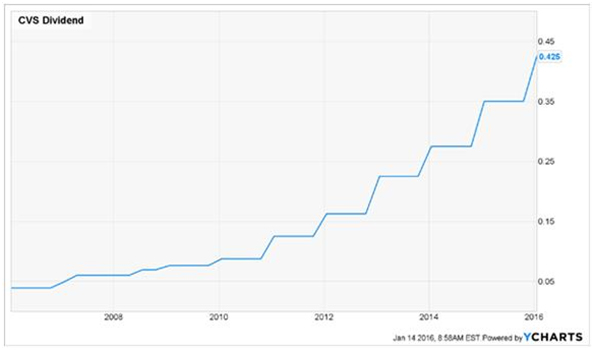

Business is booming at CVS, and the company generously shares its profits with shareholders. It’s raised its dividend by 9.9% annually, on average, over the past decade.

Accelerating Dividend Growth at CVS

Since 2007, CVS has also reduced its outstanding share count by 30%. These stock buybacks have created a virtuous cycle for shareholders, as fewer and fewer shares translate into accelerating earnings-per-share (EPS) and dividend growth.

By the end of this year, all of Target’s (TGT) 1,660 pharmacies will become CVS-branded facilities. Consumer advocates already worry that this acquisition, which consolidates competition, will lead to higher prices. It probably will – which is good news for CVS shareholders.

The stock yields 1.7% today. A modest 30% payout ratio provides some upside for continued dividend increases. Analysts are projecting double-digit earnings growth through 2019, making the stock’s price-to-earnings (P/E) ratio of 22 look quite reasonable.

And 3 Retirement-Lifestyle Firms With Growing Client Bases

Sun Communities (SUI) operates a couple hundred home and RV communities across the U.S. The stock pays 3.6% today, and the company just expanded its property list by 45% with its acquisition of Carefree Communities.

The deal also increases Sun’s presence in California from 1% to 6% – a plus for retirees who desire the Golden Coast. Carefree’s premium properties will boost Sun’s overall rents by 3.5%.

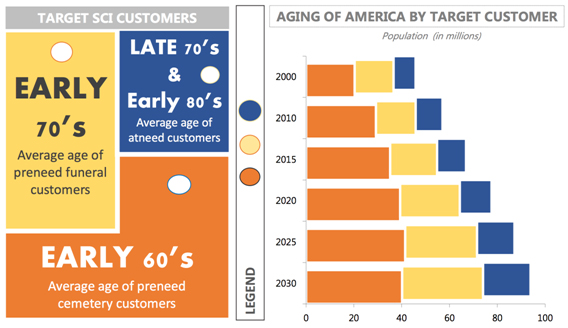

Service Corporation International (SCI) is North America’s largest provider of funeral and cemetery services. The company’s always had a large addressable market, but its potential for near-term business keeps getting better.

It’s a Bull Market in “Pre-Need” and “At-Need” Clients for SCI

At the end of 2015, the company had booked a record $9.5 billion in future revenues (more than 3-times current annual revenues) along with $1.6 billion in pre-need sales.

SCI’s always treated shareholders well, too – it increased its dividend by 380% over the past decade. Over that period, its stock returned 14% annually to shareholders versus 7% for the S&P 500.

And it should have won by even more. As you can see, SCI’s stock price hasn’t kept pace with its dividend growth recently – presenting us with a nice buying opportunity.

SCI’s Stock Price Lags Its Dividend Lately

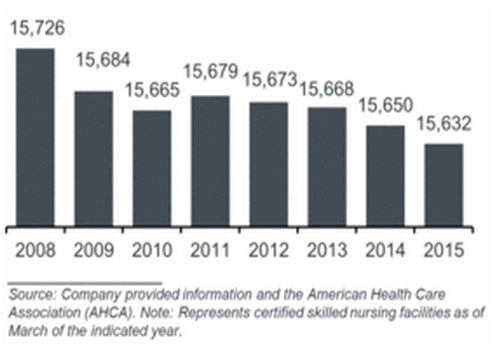

My final company, and top favorite, operates skilled nursing facilities. While healthcare is big, skilled nursing is a particularly hot area. These facilities provide the highest level of care an older adult can receive while still living independently. Residents generally get their own room, their own bed, and a private bathroom. Many folks are able to enjoy their remaining years here in relative comfort.

While demand is going to keep climbing (with the 65+ population set to double in the years ahead) supply is actually decreasing. We have less skilled nursing facilities today than we did in 2009!

Skilled Nursing Supply is Actually Decreasing

Rising demand and falling supply have this specialty provider well positioned to grow its dividend in the years ahead. I anticipate its payout will double again over the next decade. And remember, it already pays 8.9%.