“First-level” investors – those who buy and sell on headlines – mistakenly believe that real estate investment trust (REIT) profits will suffer if rates rise.

Sure, in the short run, the “rates up, REITs down” theory puts on quite the show. When the 10-Year Treasury’s yield rises, REITs usually fall. And when its yield drops, REITs usually rally. This inverse relationship tends to hold up over multiple days, weeks and even months:

A Short-Run Seesaw Between REITs and T-Bill Yields

The theory backing up this price action says that, because REITs borrow money to grow their property empires, they need cheap cash. Yet this isn’t a “must have” criterion for all such landlords. If their costs increase, they can simply raise the rents when the lease is up for renewal, passing on their higher borrowing costs to tenants.

For example, let’s look at a three-year period starting in May 2003 when the 10-year rate climbed two full basis points – from 3.2% to 5.2%. Based on recent REIT price action, you’d expect most firms would be out of business!

But blue chips such as mall operator Simon Property Group (SPG) and self-storage stalwart Public Storage (PSA) not only survived the rate increases – they thrived:

The Best REITs Climbed With Rates

Why? Because rising rates signaled a booming economy – one in which these firms had no problem raising their rents. Both boosted dividends while investors in each stock enjoyed 129% total returns over the three-year period!

Which REITs Will Thrive This Rate Hike Cycle?

Firms having no problem issuing rent increases today are easy to spot. They report higher and higher funds from operations (FFO) year after year, which finds its way back to shareholders in the form of an ever-rising dividend.

Let’s look at five big paying REITs to see how rate-proof they appear. Three are promising, two… not so much.

Select Income REIT (SIR)

Dividend Yield: 8.7%

Select Income REIT (SIR) is a two-pronged REIT that mostly holds industrial and office properties, boasting 45.2 million rentable square feet across 35 states that it leases out to the likes of FedEx (FDX), Micron (MU) and ServiceNow (NOW). What really makes SIR something of a unique play, however, is just one of those states – Hawaii, which represents more than a third of its rentable space.

SIR has had a rough 2017, off about 7% year-to-date versus a mostly flat performance for the Vanguard REIT ETF (VNQ) and a positive 12% performance from the S&P 500.

Those difficulties largely have come thanks to a significant tenant’s bankruptcy. The REIT has been forced to write off rents and absorb asset impairments thanks to the exit of this tenant from two properties, putting a wrench in what has otherwise been a strong growth story. Select Income REIT has watched its top line jump nearly 150% since 2013, which has helped fuel a growing and sustainable payout that currently translates into a high-8% yield.

While the share declines in 2017 have no doubt disappointed existing shareholders, it has helped drive SIR shares into value territory, with the stock trading at less than 9 times trailing 12-month funds from operations (FFO).

Select Income REIT (SIR): It’s Not a Slump – It’s Just a Slip

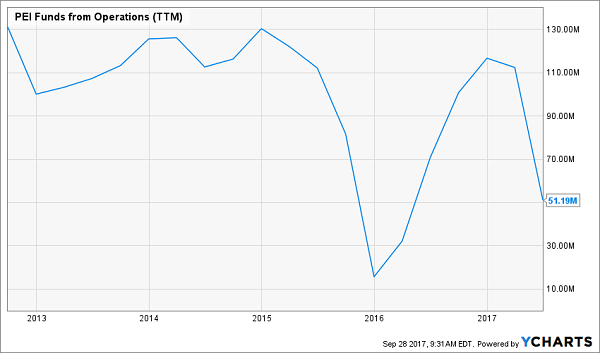

Pennsylvania R.E.I.T. (PEI)

Dividend Yield: 8%

While I think industrial and office properties like those held by Select Income REIT will be just fine, and while I believe SIR’s problems are mostly temporary in nature, I don’t feel the same way about Pennsylvania R.E.I.T., nor the retail world in which it plays.

Pennsylvania R.E.I.T. is a mall operator in (naturally) the state of Pennsylvania, as well as along the East Coast, including the attractive D.C. metro area market. And as one would expect, this retail-focused REIT has been hammered this year, with 45% year-to-date losses making it one of the sector’s worst performers of 2017.

I will say that PEI is at least giving itself a shot at survival by not standing still, and instead trying to focus more on the “experience” economy by bringing in tenants such as Dave & Buster’s (PLAY) designed to deliver more than just shopping/eating options.

But Pennsylvania R.E.I.T. has been beaten up for a reason. The company’s net loss through six months has widened year-over-year, and adjusted funds from operations have dropped from 85 cents through the first two quarters of 2016 to 74 cents through 2017’s midway mark. Meanwhile, the dividend, while generous, hasn’t budged since 2015 after years of growth – and given PEI’s problems, I don’t expect that problem to fix itself anytime soon.

Pennsylvania R.E.I.T. (PEI): The Trend Is … Nauseating.

Hospitality Properties Trust (HPT)

Dividend Yield: 7.3%

Speaking of the “experience” economy, I believe hotel REITs have a lot left to offer, and Hospitality Properties Trust (HPT) looks like one of the stocks that has something worth looking at.

That’s in part because HPT isn’t your garden-variety hotel REIT.

Hospitality Properties Trust does own 310 primarily select service and extended stay hotels throughout the U.S., Canada and Puerto Rico, under brands such as Courtyard, SpringHill Suites, Hyatt Place and Radisson.

However, while HPT has exposure to urban or high-density suburban areas via its hotels, it also sucks money from the highway system, where it owns or leases nearly 200 full-service travel centers that don’t just pump gas, but also include restaurants and truck repair.

While Hospitality Properties was hampered by a rough first quarter, it bounced back with a nearly 20% jump in second-quarter net income. And while FFO trickled down a bit, it still came to $1.06 per share – enough to cover its 52-cent quarterly dividend twice and then some.

This is an exceedingly safe dividend that has ticked higher for years, and it’s in an idea area of the economy for the coming years.

Hospitality Property Trust (HPT) Is a Thing of Beauty

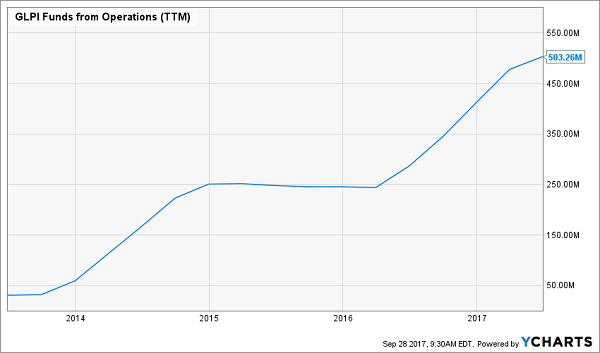

Gaming and Leisure Properties (GLPI)

Dividend Yield: 6.9%

Gaming and Leisure Properties (GLPI) is another great variation on the traditional hotel REIT. That’s because it’s a casino real estate play – so while rooms are certainly part of the action, you’re also getting in on America’s increasingly gambling-happy ways, and again, the “experience” economy.

GLPI isn’t a “Big Vegas” play like Las Vegas Sands (LVS) or Wynn Resorts (WYNN). In fact, this REIT has very little Nevada in it at all, and tends to focus its operations in southern states like Louisiana and Mississippi, and midwestern states such as Ohio and Illinois.

This is a monster growth play that has seen revenues nearly quadruple since 2012, and its recently reported Q2 showed continued strong operational performance. Of note was AFFO of $167.8 million – not just up 24% year-over-year, but ahead of the company’s own guidance.

The results were so good, in fact, that GLPI hiked its dividend to 63 cents per share – its fourth increase in just two years!

Gaming and Leisure Properties (GLPI) Is on a Heater

CBL & Associates (CBL)

Dividend Yield: 12%

What’s not to like about a 12% yield?

Plenty.

CBL & Associates (CBL) is a REIT that specializes in shopping centers – malls, yes, but also “community centers” that mix retail, dining and entertainment. Still, this is a primarily retail outfit, and one that has been forced into a painful pivot as CBL tries to redefine what it is.

CBL’s net income has declined 34% year-over-year through just the first two quarters of 2017. And while the dividend is hardly in trouble — $1.02 in AFFO through six months easily covers two 26.5-cent payments – it’s not growing, either, with the payment stagnant since 2015. Moreover, that $1.02 in adjusted funds from operations represents a nasty 11% slide year-over-year.

CBL & Associates (CBL) Is Stalling Out

CEO Stephen Lebovitz’s second-quarter comments illustrate both the company’s troubles and its state of flux. “Taking into account the difficult retail environment, second quarter operating results were in-line with expectations, but still disappointing,” he said. And “Our priority through the remainder of the year is maintaining and improving occupancy and income as we focus on reinventing our market dominant properties.”

This follows a quarter that saw portfolio occupancy decline a full percentage point, and that saw CBL decide to write off several new development projects in lieu of focusing on redevelopments.

An eventual turnaround story? That remains to be seen. But this double-digit yield is the result of dwindling confidence and share prices – not a robustly expanding payout. Steer clear.

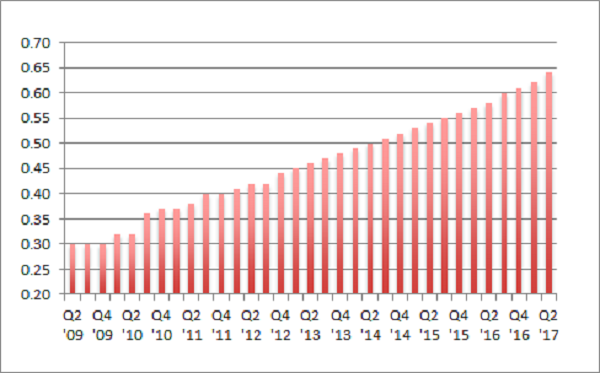

Buy These Rate-Proof REITs: 2 Plays With 7.6%+ Yields and 25% Upside

One of my top REIT buys right now recently raised its dividend again by 4% over last quarter’s payout. This marks the 20th consecutive quarterly dividend hike for the firm:

Dividend Hikes Every Quarter

It pays an 8.1% yield today – but that’s actually an 8.5% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times funds from operations (FFO). Pretty cheap.

However I expect its valuation and stock price will rise by 20% over the next 12 months as more money comes stampeding into its REIT sector – which makes right now the best time to buy and secure an 8.5% forward yield.

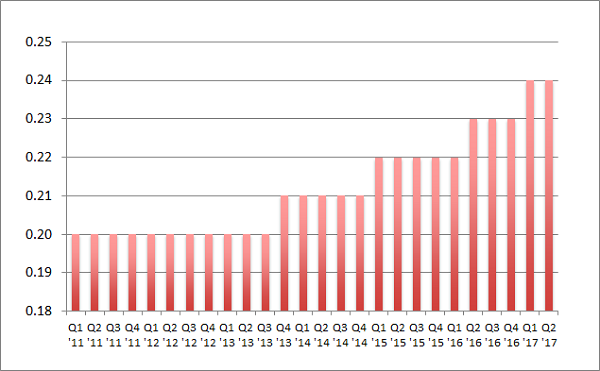

Same for another REIT favorite of mine, a 7.6% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years.

The firm’s investors have enjoyed 86% total returns over the last five years (with much of that coming back as cash dividends.) And right now is actually a better time than ever to buy because its growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

An Accelerating Dividend

This stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof,

- It yields a fat (and secure) 7.6%, and

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.6%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.