Let’s relegate 2020 to the trash heap (where it belongs!) and look to the new year that dawns tomorrow. I’ve got three predictions I’m going to lay out for you now, and three high-yield closed-end funds (CEFs) with dividends up to 8% that are nicely positioned to ride them to strong gains in the next 12 months and beyond.

Prediction No. 1: Home Sales Will Surge—and So Will This 8% Payer

One of the biggest financial stories of 2020 was the strong real estate market. In November, US home prices jumped 12.7%, and Zillow believes 2021 will be “the hottest [year] in recent memory.”

What’s happening here is that lockdowns have caused many people to rediscover the joys of spacious single-family houses. That, in turn, has lifted real estate values more broadly, as a small bit of equity in, say, San Francisco can suddenly pay for most or all of a mansion in Idaho.

This trend has one clear winner: real-estate companies, not just in residential spaces but across the board because as residential real estate benefits outside the big cities, so too do other types of real estate not concentrated in large metropolises.

A good play in the real-estate space is the Cohen & Steers Quality Income Realty Fund (RQI), which pays an 8% dividend (compared to a meager 1.5% for the typical S&P 500 stock!). If you want one-stop access to the publicly traded real-estate market, this fund is a good option: it holds a variety of strong real estate investment trusts (REITs), like cell-tower operator American Tower (AMT), warehouse landlord Prologis (PLD) and data-center REIT Equinix (EQIX).

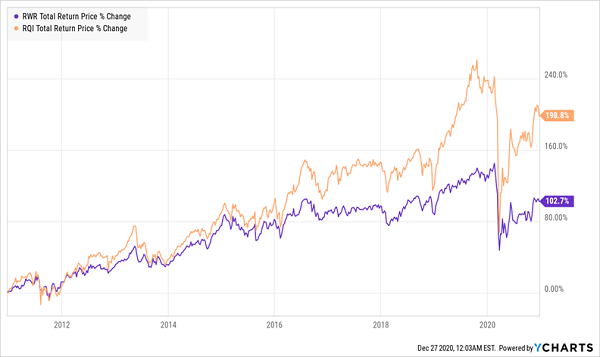

RQI has the kind of track record we love to see in a CEF: in the last decade, it’s nearly doubled the return of the REIT market, shown by the SPDR Dow Jones REIT ETF (RWR) in purple below.

RQI’s Managers Double Up REITs

RQI continued to outperform in 2020, a tough year for real estate, and has maintained its $0.08-a-share dividend, which it pays monthly. The COVID-19 crisis isn’t RQI’s first rodeo, either: it also navigated, and thrived after, the 2008/’09 collapse. Much the same is likely for 2021 and beyond.

Prediction No. 2: E-Commerce, and This 4% Payer, Have Just Started Their Run

The next big story of 2021 will be a continuation of 2020: COVID-19 has been called a “time machine,” driving us all to get rid of outdated practices and conduct more of our affairs remotely. We see this in everything from birthday parties held via Zoom to the sharp jump in online grocery shopping.

Some of this behavior will decline in 2021—after all, no one wants to attend a Zoom party when they can have the real thing. But a lot of it will keep growing as people have embraced real conveniences, such as remote learning and working outside the office. I expect this accelerated rise in online activity to keep driving tech stocks higher, even after their big jump in 2020.

A fund that’s well-tuned to the ongoing rise of tech is the BlackRock Science and Technology Trust (BST).

Like RQI, BST has a strong track record, beating the NASDAQ since its inception while easily earning enough from its portfolio of tech stocks—Apple (AAPL), Amazon.com (AMZN) and Microsoft (MSFT) among them—to cover its 4.2% dividend yield.

BST Outruns Tech High-Flyers

The reason for this is BST’s management. The team at BlackRock, the world’s biggest asset manager, has connections and research assets other firms can’t match. That helps it pick the tech stocks best positioned for tomorrow’s trends and sidestep overpriced firms with little to back up their lofty valuations.

Prediction No. 3: Main Street Recovers, This 5.4% Dividend Grows

Yes, the shops, restaurants and all the other things that make downtowns vibrant and fun will come back throughout 2021 as more people are vaccinated. Some sociologists believe the coming decade could mirror the roaring ’20s of a century ago, which were also spurred by a pandemic.

A good, high-dividend way for us to play a general economic renaissance is through the AllianzGI Equity & Convertible Income Fund (NIE).

NIE’s portfolio consists of stocks—mainly of big, reliable companies—and convertible bonds, a type of higher-yielding debt that can “convert” into stocks if the issuer’s stock price rises; convertibles are mostly issued by smaller, fast-growing companies.

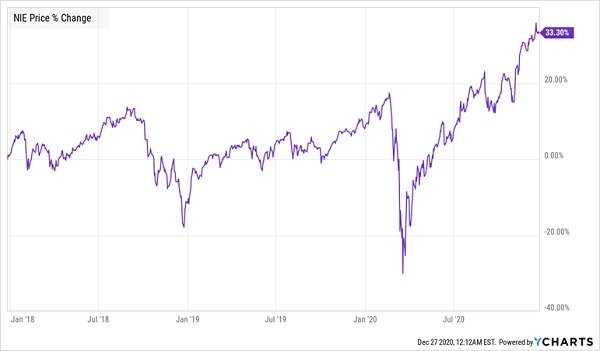

NIE’s stock/convertible-bond mix has resulted in a steady dividend for the fund’s investors that currently yields 5.4%. This payout has yielded around 7% in the past, but NIE’s recent price surge has brought the yield down (because you calculate yield by dividing the annual dividend payout into the current share price).

The good news is that I see NIE handing us some of its recent price gains in the form of a higher dividend in 2021, which would increase its 5.4% yield:

NIE’s Big Gain Foreshadows a Payout Hike

With NIE’s exposure and market dynamics, it should be positioned to grow its payouts as capital flows more freely throughout the real economy. This will improve cash flow for the companies NIE holds, in turn increasing stock prices and helping convertible bonds increase in value and convert to stocks, thus giving management more confidence to increase its payout to shareholders. When that happens, expect NIE’s 9% discount to net asset value (NAV, or the value of the fund’s underlying portfolio) to shrink, driving the fund’s price higher as it does.

Your Best Buys for 2021: The 7% Payers That Have Made Money 99% of the Time

Closed-end funds have another advantage beyond their massive dividends—they have an incredible safety record, too.

Here’s what my latest research says: of the 330 CEFs that are a decade old or older, only 14 have lost money in the last 10 years.

That’s a 96% win rate!

That’s incredible enough on its own, but there’s more: of the 14 CEFs that did lose money, 11 were in the energy sector. Dump those 11 laggards and these CEFs’ win rate jumps to an amazing 99%!

When you add in the fact that CEFs pay huge dividends—7%, on average, as I write this—you can see why these funds are a good choice for 2021, a year that looks strong overall but will likely hand us more turbulence in the short run.

That’s why, as we move into 2021, I’m pounding the table on 5 CEFs I see as your best plays for the year ahead. I’ve got all 5 pegged for 20%+ price upside in the coming 12 months, AND they pay even higher dividends than the CEF average: a gaudy 7.5% between them!

Don’t miss out on these high-yield “safety first” bargains with big upside ahead in 2021! Full details on all 5 of them—names, tickers, complete dividend histories and everything else you need to know—are waiting for you right here.