The retirement-income battle never ends! In 2020 and 2021, we were terrified of dividend cuts. Now we’re sweating soaring inflation!

The good news? No matter what the worry, we can apply my “2-step retirement income plan.” It’s designed to keep anything Jay Powell, Vladimir Putin or even Chinese President Xi does from impacting our dividend streams.

(Below I’ll give you two tickers that work perfectly with this strategy, including one that profits from the demise of Russian oil. This unsung company just hiked its payout 50%.)

Inflation Sideswipes Retirees

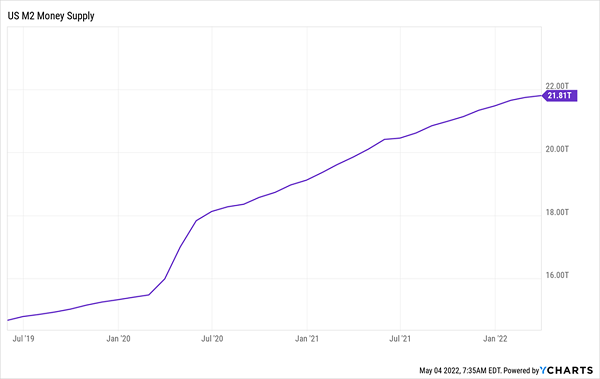

Of course, this market crash is mainly the work of Powell, who overshot the mark on stimulus, boosting the money supply by a ridiculous 40% since February 2020. And look at the right side of the chart below: even though inflation has been a problem for more than a year, he’s only just now tapping the brakes!

Powell Grows (and Grows and Grows) the Money Supply

We all know that retirees—folks with the least amount of wiggle room in their budgets—are taking the brunt. If you’re retired, or near retirement, you’ve probably noticed that the prices of the things you need the most have spiked.

Hoping to visit the grandkids this summer? The price of airline tickets jumped 11% in March from February, according to the latest read of the consumer price index. Forget driving—gas prices are up 48% from a year ago! Other everyday essentials are also soaring: electricity is up 11% from a year ago. Clothing? Up 7%.

You’re no doubt nodding your head along with this list. And if you’re like me, you think these numbers are too conservative compared to what we’re seeing in stores.

This is where my two favorite dividend strategies for dealing with our soaring cost of living come in. One is more suitable for an investor who’s years out from retirement, while the other is a perfect way to bulk up your income if you’ve clocked out of the workforce, or are about to do so.

Years From Retirement: Switch on the “Dividend Magnet”

If you’re still a few years from hanging them up, dividend-growth stocks should be your go-to as inflation heads north. But not just any old dividend growers—we want stocks with payouts that are accelerating.

Companies with soaring payouts pay us in three ways:

- By paying a dividend now, and …

- Growing their payouts, and …

- Share-price growth, as dividend growers’ share prices, puppy dog–like, track their dividends higher.

Cameco: A Smart Buy as Nuclear Power Roars Back

The first stock I want to tell you about is perfect for this approach. It’s a uranium producer—and I love the outlook for uranium.

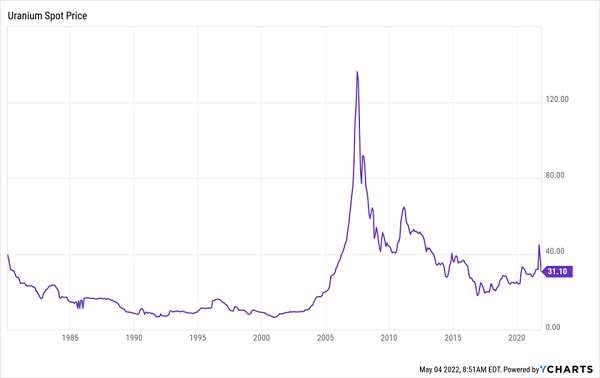

The other yellow metal peaked before the financial crisis. Yet its price has floundered for the last 15 years. That’s right. Uranium crashed in 2007 and it’s only now starting to rally. With a 15-year windup, it’s poised for quite the pitch:

Uranium’s Unfolding Rebound

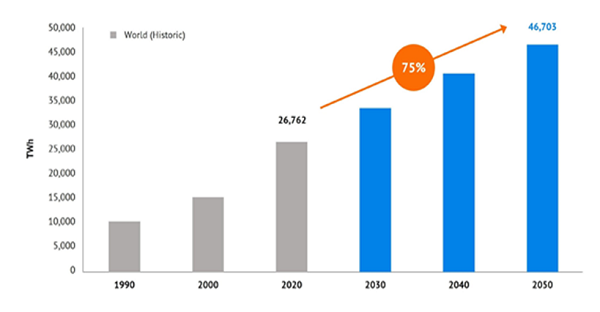

Demand appears locked in a long-term uptrend for many reasons, starting with population growth: by 2050, we’ll have nearly 9.8 billion people on the planet. The resulting jump in electricity use is forecast to inflate uranium demand by 75% in the three decades following 2020:

Source: Cameco, IEA World Energy Outlook

Nuclear-power generation will be needed to get us from here to there. Plus, nuclear is considered a clean energy source, and lower CO2 emissions are required to ensure a livable tomorrow.

But the future isn’t our only problem. The world needs non-Russian energy sources yesterday. Buying gobs of natural gas to fund a war machine is no good.

That’s why the UK has announced plans to triple its nuclear-power generation. French President Emmanuel Macron promised more nuclear power in his re-election platform. More countries on the continent will likely follow.

Canada-based Cameco (CCJ) is a prime beneficiary of this nuclear renaissance. It’s one of the world’s largest uranium producers, churning out 53 million pounds annually, good for 17% of global output.

The majority of Cameco’s uranium comes from its operations in Saskatchewan, with a smaller mine in Kazakhstan it owns through a joint venture. Cameco also has suspended mines in the US that it could restart, but management is taking a careful approach, with plans to run its mines below capacity for the next few years.

Like all miners, Cameco’s fortunes rise and fall with the price of the commodity it produces. As such, the stock has gained, with lots of potential to move higher.

That’s in part due to the influence of its payout, which does only yield 0.4% today but looks set for a long-term run, as the company rolled out a whopping 50% hike last year. Investors took notice, bidding up the stock up in tandem (all figures in Canadian dollars):

Cameco’s “Dividend Magnet” Pulls Its Share Price Higher

As Cameco’s dividend fluctuates with uranium prices, this isn’t a stock we’ll buy and tuck away. But it is a smart buy now, as countries wean themselves off fossil fuels in general and Russian fossil fuels in particular.

The company gets an extra cushion from its balance sheet: as of the end of the first quarter, it had $996 million in long-term debt, less than its $1.5 billion in cash and short-term investments. Finally, the fact that Cameco is based in friendly Canada is an added plus in this new era of “onshoring” and “deglobalization.”

In (or Near) Retirement: Grab These Monthly 7%+ Cash Streams

Cameco is a great stock to consider if you’re far from retirement, as rising uranium will likely translate into higher dividends and share prices in the long run. But what if you’re in or near retirement and want more of your return in dividend payouts?

This is where one of the best—and by far the most unloved—dividend plays of them all comes in: closed-end funds (CEFs).

There are around 500 CEFs out there, and they offer retirees the one thing they need most: big dividends, often paid monthly. The typical CEF yields around 7% right now, and many pay more.

Consider a fund like the Eaton Vance Tax-Managed Buy-Write Strategy Fund (EXD), which can be a great high-dividend way to own some of America’s best-known blue chips. It has a particular weighting to tech, at 36% of the portfolio. Apple (AAPL) and Microsoft (MSFT) are its top two holdings.

That makes EXD interesting, as tech’s influence in our lives will long outrun this string of Fed rate hikes, making today’s prices on beaten down large-cap techs tempting. As tech recovers, you could ride along while collecting most of your gains through EXD’s 8.2% dividend, paid monthly. And that big payout is resilient: it held firm through the COVID-19 economic collapse.

In addition, EXD generates extra cash by selling covered-call options—rights investors purchase to buy EXD’s shares if they trade above a certain level at a fixed time in the future. This strategy works well in a volatile market because if a stock closes below the strike price, EXD keeps its shares and the premium our option buyers pay. We get that premium as part of our dividend.

Plus we can pick up EXD at 1.8% below its net asset value (NAV, or the value of the shares in its portfolio) as I write this. That may not sound like much of a deal, but the fund has traded at premiums for most of the past year, suggesting further gains could be ahead.

Crush Inflation With My 7 Top Dividend-Growth Buys (Yours Now)

I’ve handpicked 7 dividend-growth stocks whose payouts are all rising at a fast clip. As a result, I expect these 7 companies’ payouts to drive 15%+ annualized gains for years to come.

And thanks to their rising payouts, more and more of that return would come your way in dividend cash as time rolls on!

A 15% return is more than enough to outrun inflation—even stratospheric inflation like the 8.5% rise in the CPI we’re facing today. That makes now the perfect time to buy these 7 stout dividend growers.