Not many people know this, but if you really want to diversify—deftly balancing and rebalancing to maximize (and protect) your gains, you need to invest in closed-end funds (CEFs).

Doing this with CEFs, which yield around 8% on average, gives you two key advantages:

First, you get a much bigger income stream. That’s great on its own. But if you’re reinvesting your income, you get an even bigger edge because you can easily redirect your dividends from one CEF to another in a different sector. You just can’t do this with an index fund.

Let’s dig into how that works in practice.

While 2024 has been a great year for stocks, some sectors are lagging, as is always the case. And right now, as we look ahead to 2025, is a good time to reallocate a bit from your winners into the stragglers. That’s because, over time, these laggards will likely revert to their long-term average performance.

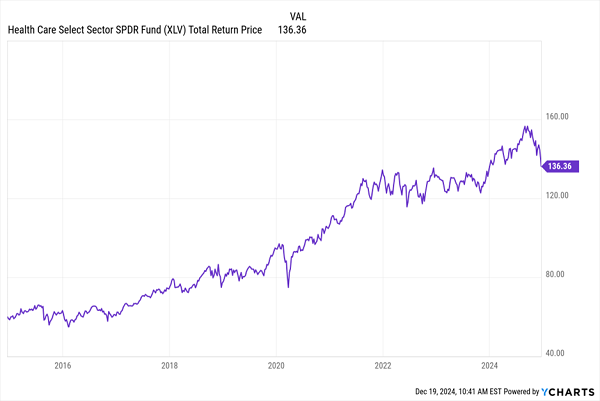

A look at the sectors making up the S&P 500 tells us that the biggest winners this year have been the communication services, finance, consumer discretionary and tech sectors. These firms are picking up the slack we’ve seen in materials, energy and healthcare. I want to focus on healthcare, because the gap between this year’s performance (up just around 1.1% following last week’s selloff) and what the sector has done in the long run is striking.

Healthcare: Short-Term Weakness Masks Long-Term Strength

With about a 9% annualized return over the last decade, healthcare has performed relatively well, making it a good target for rebalancing by moving profits (or CEF dividends) into it from the stronger-performing sectors of 2024.

The highest-yielding healthcare CEF is the abrdn Healthcare Investors Fund (HQH), a 14.2% payer whose portfolio includes key pharma names like Gilead Sciences (GILD), Amgen (AMGN) and Eli Lilly & Co. (LLY). It would take just $705,000 invested in this fund to get $100,000 per year in income.

Plus, HQH’s focus on healthcare means we could pair it with other sector-specific CEFs and rebalance to ensure we aren’t overexposed to any particular industry—and also profit from the performance differences between those sectors.

But to make certain HQH is the best CEF for this strategy, we need to dig deeper.

As of this writing, HQH has beaten the healthcare sector as a whole, with a 7.9% total NAV return year to date (this is a CEF-specific measure that examines the performance of a fund’s underlying portfolio, rather than its price on the open market), about seven times the return of the benchmark Health Care Select Sector SPDR Fund (XLV).

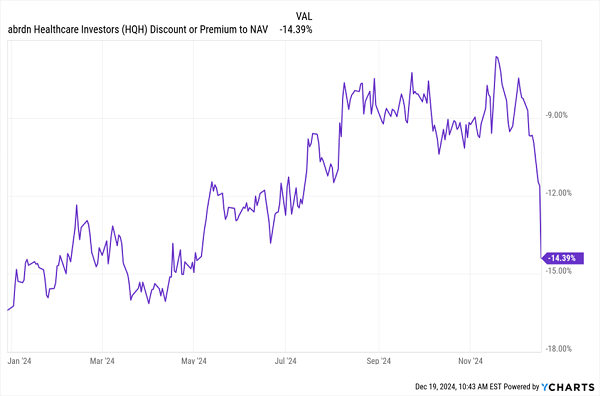

However, on the open market, the fund has returned 10.6%, including dividends paid out. This gap largely stems from the fund’s big discount to NAV (or the difference between the NAV- and market price–based return), which was over 15% at the start of the year and has now returned to that overly generous discount following the big selloff last week.

HQH’s Discount Fades and Returns

This is a new buying opportunity, and momentum could drive that discount smaller still over the coming months if the market’s recent panic subsides, pulling up the fund’s market price with it. And if HQH doesn’t cut its payout, we may indeed see that discount get smaller still.

There are two problems, however: Obviously, the market pullback might not yet be done and, more importantly, HQH raised its dividend in May, which means it’s now paying a 12.6% yield on NAV, much higher than that 7.9% total NAV return we just talked about. This means the dividend might need to be cut. Or HQH will need to pay out shareholder capital, shrinking the fund’s size—and its gain potential.

That’s a tough situation, made worse by management’s decision to raise the payout.

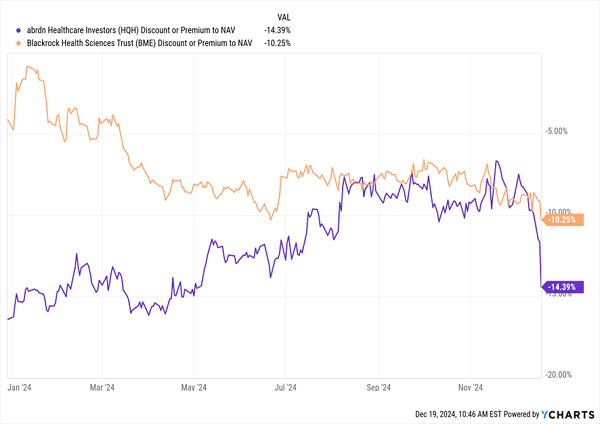

Now let’s consider the BlackRock Health Sciences Trust (BME), whose 7% yield is half that of HQH. BME trades at a less generous 10.3% discount, but the trend in this discount (in orange below) is very different than that of HQH (in purple).

BME’s Widening Discount vs. the HQH “U”

HQH went from being priced at par to a huge discount to going back toward par over the last three years to plummeting last week. BME, meantime, has been on a steady descent toward a bigger discount (although the vector of decline has flattened out significantly in 2024, and it didn’t change all that much with the recent selloff).

This would suggest BME is at risk of getting cheaper, but there’s a key detail: The fund is part of BlackRock’s “discount management program,” under which the company buys a certain amount of some CEFs (including BME) if their average discount is more than 7.5% during a three-month measurement period.

HQH has no such initiative, which is why its discount grew so large late last year and why its discount could grow so massively.

This means BME is unlikely to see its discount go much lower. And even if it does, BlackRock’s discount-management program means the firm will buy back shares on a quarterly basis at a 2% discount. If you tender your shares during this offer after buying at the fund’s current price, the result would be an instant 9.3% profit.

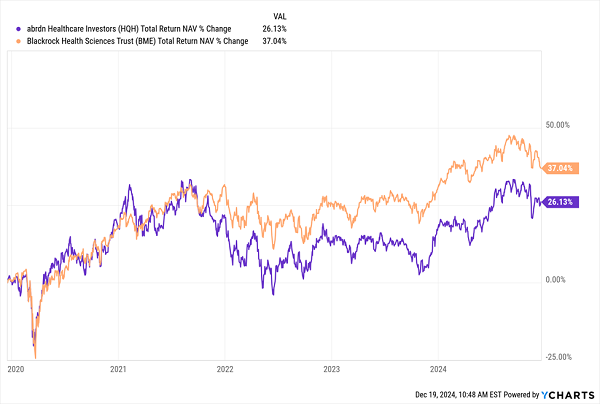

There’s one more reason to prefer BME over HQH, despite its lower yield.

BME’s Higher Returns

Over the last five years, BME (in orange above) has outperformed HQH on a total-NAV-return basis. This suggests it should be priced at a much smaller discount than HQH, on the strength of its stronger management. This also suggests BME is the better buy when its discount gets unusually wide.

Thus, while HQH’s huge dividends make it look like the better choice, if you want to buy and hold a sector fund for the long term, BME is likely to outperform HQH, especially if BlackRock continues its discount-management program. However, if abrdn were to start its own discount-management program, HQH might have the edge. Until that happens, though, my money’s on BME.

Yours Now: A 5-Fund “Mini-Portfolio” That’s Perfect for 2025 (Yielding 8.3%)

CEFs’ outsized dividends and discount-driven gains are, in my view, the key to funding the retirement you want on dividends alone.

You can see it in the massive yields we just talked about—and there are plenty of other CEF options beyond healthcare we can use to bolster our income (and juice our upside, too).

Case in point: the 5 other “hidden” CEFs I’m urging all investors to buy now, as we move into 2025, a year with many opportunities for fleet-footed income investors.

These 5 funds yield 8.3% on average and, as stated, come from across the economy, holding the best blue chip stocks, corporate bonds, real estate investment trusts (REITs) and more.

Put them together and you have an instantly diversified mini-portfolio that’s cheap now, and kicking out that rich 8.3% average dividend, too.