What if you could squeeze, say, a 70% dividend yield from a fast-growing AI stock like NVIDIA (NVDA) or Palantir (PLTR)?

Sounds great, right?

Instead of relying just on these stocks’ prices for your profits (since dividends are, frankly, the furthest thing from their CFOs’ minds), you get their returns as high-yielding dividends.

That’s something a new breed of ETFs is promising. These funds, which are gaining in popularity, hold just one stock—usually a Palantir, Tesla (TSLA) or NVIDIA—and trade options on that one stock to deliver stated yields often way above 50%.

Does it work?

First, let me say that, as someone who has covered 8%+ yielding closed-end funds (CEFs) for over a decade, I get the sentiment behind these funds. Big income streams can create financial independence—who wouldn’t want as big of a yield as possible?

But there’s a line where a dividend goes from appealing to dangerous—and it’s well below the stated 70% distribution rate, as of this writing, on a single-stock ETF like, say, the YieldMax AI Option Income Strategy ETF (AIYY).

That’s because, what these funds’ massive yields give, their share prices can easily take away.

Consider the YieldMax AI Option Income Strategy ETF (AIYY), which aims to deliver that 70% income stream by holding C3.ai (AI), a developer of AI apps for business. As I write this, AIYY investors have seen a total return of nearly negative 50% since the start of the year.

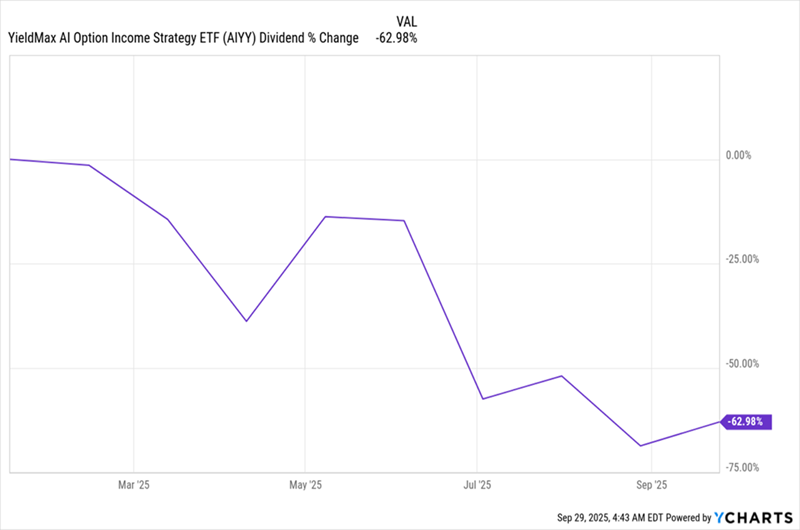

70% Dividend Doesn’t Help AIYY Investors

With nearly half of their capital now lost in 2025 (with dividends included), those holding AIYY must be wondering what went wrong.

Let’s start with that dividend, because there’s a key thing to note here: Even though AIYY’s website says its distribution rate is 71%, it also tells us that the fund’s 30-day SEC yield is only 4.8%. This means the fund’s net investment income (which can only be calculated by a strict SEC-mandated formula and excludes options income, which can be unpredictable) is much lower than that 70%—which is the payout as a percentage of the fund’s assets.

Moreover, AIYY’s distributions keep falling, down 63% in 2025.

Huge Yield, But Shrinking Payouts

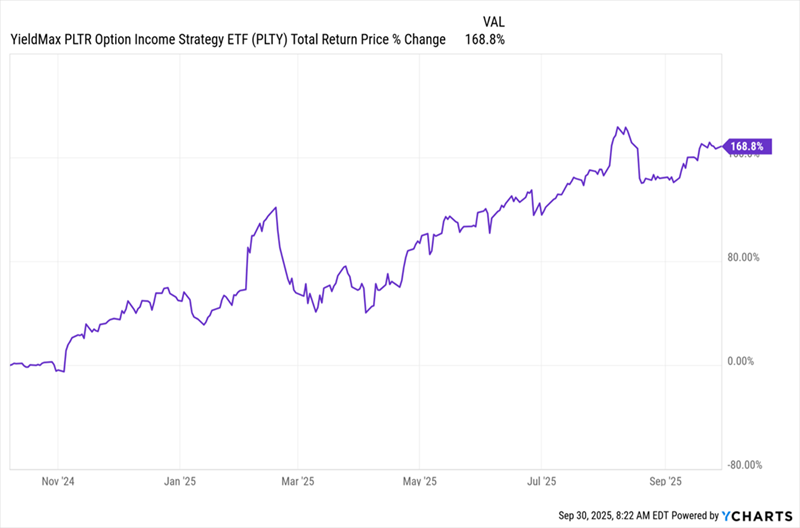

Let me clear—not all of YieldMax’s 57 ETFs are losing money this year. In fact, most are up. The best return goes to the YieldMax PLTR Option Income Strategy ETF (PLTY), with a stated 49.4% yield. This fund has returned 77.9% for 2025 and is up much more since its inception in late 2024.

PLTY Explodes Out of the Gate

So, have we found the secret to financial independence here? After all, with this 49.4% income stream, it takes only about $203,000 in upfront investment to get a six-figure income stream!

Except, well, there’s a lot of risk behind this seemingly impressive chart.

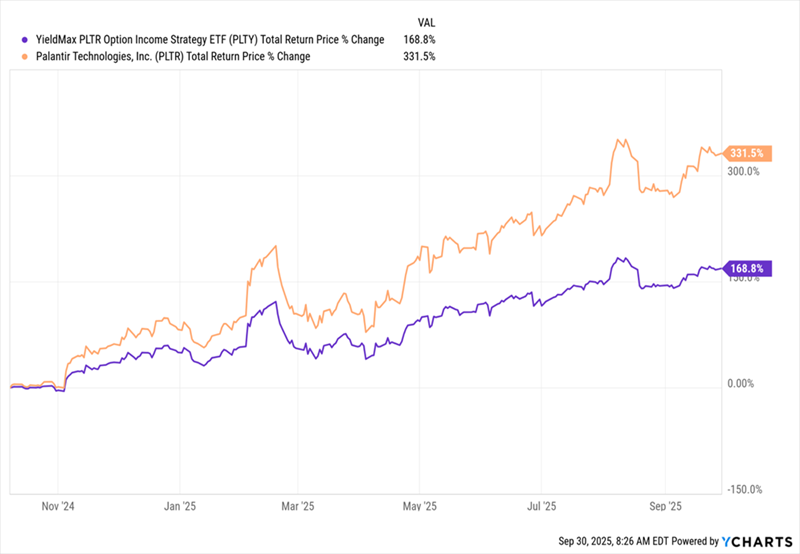

As you probably guessed from the fund name, this ETF tracks Palantir, whose stock has surged as the company wins more government contracts. If you predicted PLTR’s surge, congratulations—that’s impressive. But an investor who knew to invest in PLTR should’ve just bought that stock instead, since PLTY (in purple below) has badly lagged it.

Palantir Tramples the Single-Stock ETF That Tracks It

This problem is endemic to single-stock ETFs: These funds try to “translate” growth stocks’ gains into big dividends, but in so doing expose us to the risks of a single stock, with less upside.

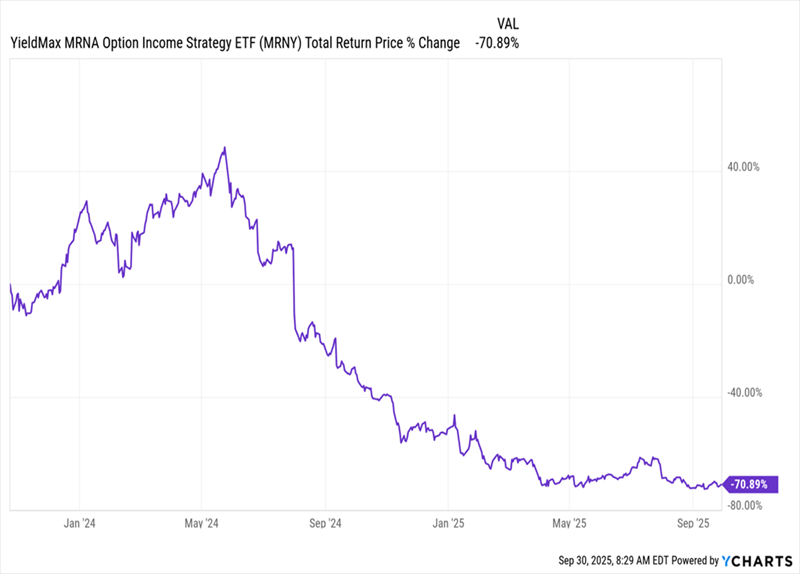

Sure, the income is great when the stock is rising, but that income will shrink if the stock drops. That’s what happened to the 56.2%-yielding YieldMax MRNA Option Income Strategy ETF (MRNY), which holds Moderna (MRNA) and is down 39% in 2025 and down even more since its IPO in early 2024.

MRNY’s 40%+ Dividend Yield Can’t Save Its Stock

Anyone who bought MRNY and enjoyed the huge yields at the start of 2024 probably thought they were really on to something, as the fund’s total return rose into the spring. They then saw their fortunes reverse as the fund’s price fell.

That’s the fate I expect for the aforementioned PLTY if the stock it tracks—again, Palantir—drops. And I see that as likely, since Palantir’s forward price-to-earnings (P/E) ratio is at a stratospheric 278 as I write this.

So what are these funds for, then? To be honest, I’m not sure. As we’ve seen, investors are almost always better off just buying the underlying stocks.

What’s more, some of these ETF issuers are venturing into even riskier territory, like the recently released “Bonk Income Blast ETF,” which doesn’t just invest in crypto, but also in “other crypto ETFs, including non-US crypto-ETFs,” according to its SEC filing.

This means investors will wind up paying the fees for this ETF, as well as fees for the ETFs it owns. Plus they’re exposing themselves to the risks of the crypto market and the risks of foreign markets—including potentially lax regulation—too.

There’s just no reason to take risks like those when you can get predictable, diversified dividends from CEFs. Sure, CEFs don’t offer the mind-blowing yields of YieldMax and its ilk. But we’ll happily take that “lower” payout—bearing in mind many CEFs yield more than 8%, if it lets us sleep peacefully at night. Moreover, we benefit from CEFs discounts to net asset value (NAV, or the value of their underlying portfolios), which hold the potential for future upside. ETFs—single stock or no—never offer us a discount.

I think you’ll agree that this is a far better deal than a 70%-yielder that’s dropped around 50% in less than a year.

Bargain Alert: These 8.2% Payers Get You BIG Dividends From AI (the Right Way)

I hate to see investors take massive risks like these when there’s a much safer way to get a high payout from the AI megatrend.

Like our approach. Right now, we’re buying 4 bargain-priced CEFs paying 8.2% on average. These stealth income plays hold smartly built, diverse portfolios of AI stocks—they’re head-and-shoulders above treacherous “one-stock” plays like PLTY.

Critically, these 4 funds hold shares of both AI developers and companies putting this breakthrough tech to work in their everyday businesses. That’s critical because it gives us a piece of the action as AI slashes these companies’ costs, boosts their sales and helps them get more out of each and every employee.

And because they’re overlooked bargains, these 8.2%-paying funds let us buy their portfolios for less than we could if we bought each of their holdings individually.