Let me take you back to April 2001 for a second. Because that year brought a key turning point for income investors.

I’m talking about the launch of the SPDR Dow Jones REIT ETF (RWR). The fund rolled down the skids with a simple mission: Give investors an easy way to buy a diversified basket of real estate investment trusts (a.k.a. REITs) in one low-cost index fund.

It was exciting because, back then, REITs had outperformed stocks when their high payouts were reinvested. And their dividend yields were much higher than those of the typical S&P 500 name, too.

Backed by reliable rents, as well as the constant need for space to store and sell things (for businesses), as well as places to live, work and have fun (for individuals), the sense was that demand for real estate would never end.

As Mark Twain once said, “Buy land—they aren’t making any more of it!”

How have things played out since the fund’s launch? Pretty much as they had been before, with REITs continuing to outperform (even through the 2008 mess).

That is, until around 2020, when the pandemic threw them for a loop.

REITs have been lagging ever since, but the fact of the matter is, this underperformance has dragged on for far too long. With the economy and corporate profits growing strongly, I see real-estate demand outpacing the fear around the sector (including around interest rates, which we’ll talk about more in a moment) in the coming months and years.

Let’s get into why I feel that’s the case now. I’ll also show you a 7.9%-paying REIT-focused closed-end fund (CEF) that’s been unfairly caught in the downdraft (as well as another 12.9% payer to avoid).

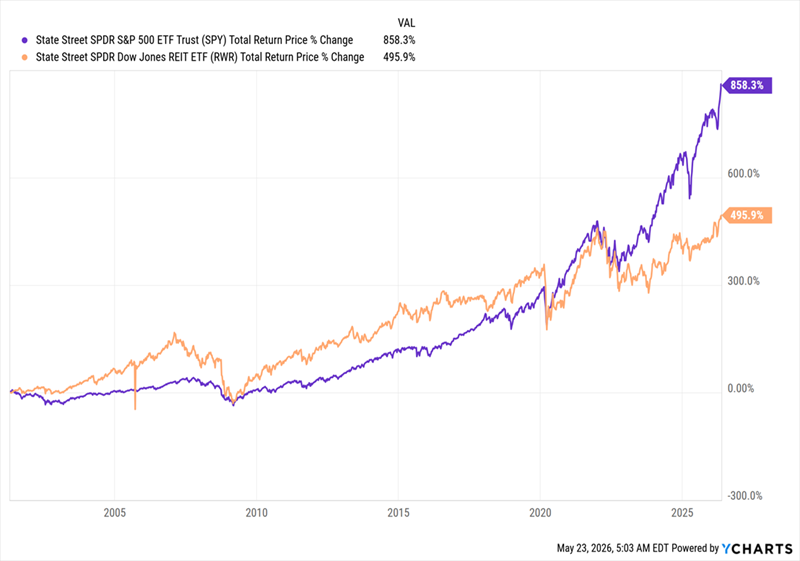

REITs Crushed Stocks—Until They Didn’t

As you can see above RWR (in orange) did well against the S&P 500 for a long time. From 2001 to 2020, the ETF’s annualized total return beat that of stocks: 8.5% versus 7.7% for the S&P 500 benchmark State Street SPDR S&P 500 ETF (SPY).

Also keep in mind that this period includes the subprime-mortgage crisis. RWR fell (and briefly underperformed SPY) in that time, but recovered fast and was back in the black before the S&P 500 was.

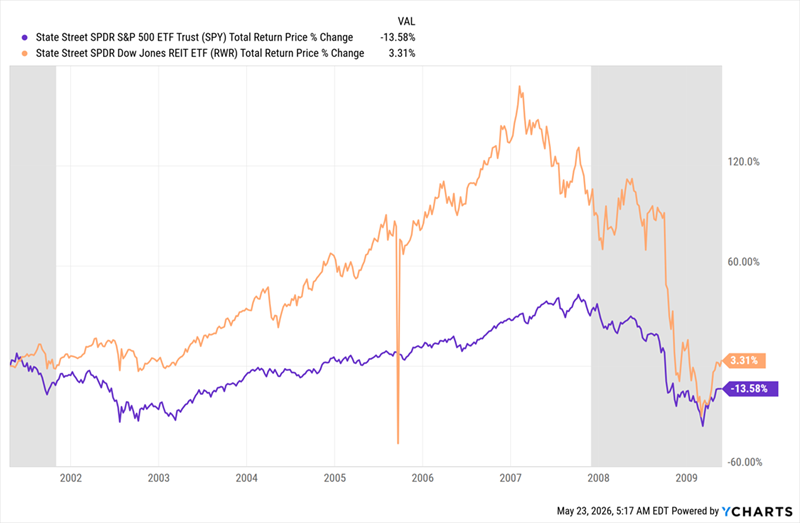

REITs Survive a Real Estate Recession

In fact, on May 26, 2009 (shown at the right side of this chart), while the US was still in the throes of the Great Recession, RWR, in orange, was posting a positive return while SPY (in purple) was negative.

One thing made this possible: dividends.

At this time, RWR’s yield was a little higher than SPY’s: 2.3% versus 1.9%. It climbed from there as RWR’s price fell, since yields and prices move in opposite directions. That cash distribution was a real benefit to investors in those stressful times.

But as we saw a couple charts ago, in 2020, REITs started underperforming, a streak that continues today. Why?

Stocks are part of the reason: Since the pandemic, they’ve been roaring, up 14% per year on average over the last five years, much higher than their historical 10% annualized gain. This is great for stock investors, of course, but it does raise the odds of a correction, so we still want to be sure we’re well-diversified.

REITs Are to Blame, Too

Stocks’ strong performance is only one side of this story, though. On the other, REITs have seen a 5.7% annualized gain over the last five years, far lower than when they were beating stocks. That’s unusual, and it’s particularly strange that it’s lasted so long.

As a result, REITs—and in particular REIT-focused CEFs—are now providing a nice opportunity to diversify some of the profits many investors have made in stocks.

An Oversold 7.9%-Paying REIT Fund With a Solid Monthly Payout

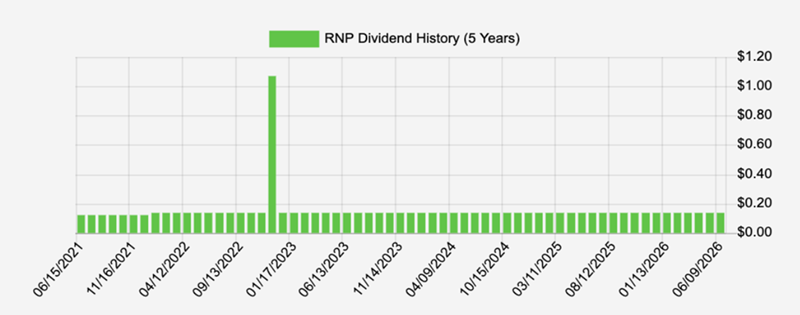

One strong REIT fund to consider is the Cohen & Steers REIT and Preferred Income Fund (RNP), a CEF that yields 7.9% today and, yes, pays monthly, too.

Over the last five years, RNP has returned around 30%—so right around the index fund’s performance. But the key difference has been that the bulk of that return has come in cash. That’s thanks to the fund’s steady monthly payout, which has not only held steady but grown in the last five years, with a special dividend thrown in:

RNP’s “Storm-Proof” Monthly Dividend

Source: Income Calendar

RNP, as the name suggests, holds REITs and preferred shares, the latter of which trade like stocks, but in a narrow range, with fixed dividends. As such, they’re best thought of as a kind of stock-bond hybrid. Those make up around half of the portfolio and bring additional stability (as well as income).

On the REIT side, which is nearly all of the other half of RNP’s holdings (there’s about 1% in cash), we’ve got a diversified set of names. They include healthcare REITs, such as Welltower (WELL); data-center and telecom firms like Digital Realty Trust (DLR) and American Tower (AMT); as well as self-storage, in the form of Extra Space Storage (EXR); housing, shopping-center REITs and more.

Both REITs and preferreds are sensitive to higher rates, which is part of the reason why the fund sports a 5.7% discount to net asset value (NAV, or the value of its underlying holdings) as I write this.

That’s far more than enough to price in today’s “sticky” rates, which are largely the result of the Iran situation. Until that’s resolved, this fund is overly marked down, especially when you consider that it’s traded at premiums many times in the past, including in 2019, 2023 and as recently as last year.

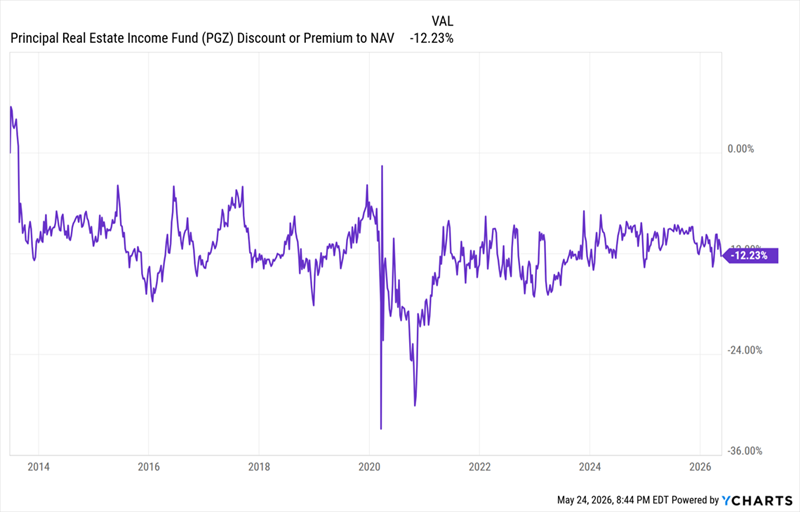

This 12.9% Payer Is Always on Sale

With all that said, not all REIT CEFs are attractive right now. Take the Principal Real Estate Income Fund (PGZ), which has a 12.2% discount and a 12.9% yield. Unfortunately, that discount never closes.

PGZ’s “Perma-Discount”

There are plenty of reasons for this, but past performance is likely the biggest thing keeping investors away: Over the last five years, PGZ has only returned around 11%, or about a third of what RNP and RWR have delivered.

A few bad years can be a sign to buy into a fund, but when that performance trails this badly and management hasn’t changed its strategy much in response, the fund is best avoided. That’s true no matter what the discount, or dividend yield, might say.

This REIT Fund Is an Ignored AI Winner, Pays a Reliable 8.7%

REIT CEFs aren’t just due for a rebound—they’re set to soar. And an unlikely “suspect” is the reason.

I’m talking about AI.

All across the economy, AI is making REITs’ properties hot commodities, including cellphone towers, data centers—even factories and warehouses.

I know we don’t often see “AI” and “factories” in the same sentence, but hear me out here. Because one thing we don’t hear about AI (and we should!) is how it’s set to reinvent the factory floor through robotics.

Sure, robots have worked in factories for decades. But now, with AI, they can do much more, including quickly changing their roles to build new products. These new machines can also make decisions for themselves if, say, a defective part comes down the line.

Before, such a thing would have ground an assembly line to a halt for hours, even days.

As AI-powered robots improve, they’ll slash manufacturers’ costs and boost their output, setting off a factory-construction boom. And the top industrial REITs will be there, ready to cash in.

I’ve handpicked a REIT CEF that’s tailor-made for this trend. It holds top industrial REITs and pays an 8.7% dividend. This smartly run fund also comes our way at an overdone 9.8% discount.

It’s one of 4 funds I’ve picked to profit from 4 overlooked megatrends being triggered by the AI boom. They’re all cheap now, and they pay a solid 10% average dividend.

I call them my 4 “Pivot Point” funds, because they each represent shifts that can literally change the direction of the entire US economy. I want to share them with you now. Click here and I’ll lay out the details and give you these 4 funds’ names and tickers in a free Special Report.