We contrarians always need to remain a step ahead. That means to find the best deals and yields, we need to be where everyone else isn’t (yet).

Right now, that means we’re taking a trip to the bank—to collect up to 12.3% annually in dividend checks.

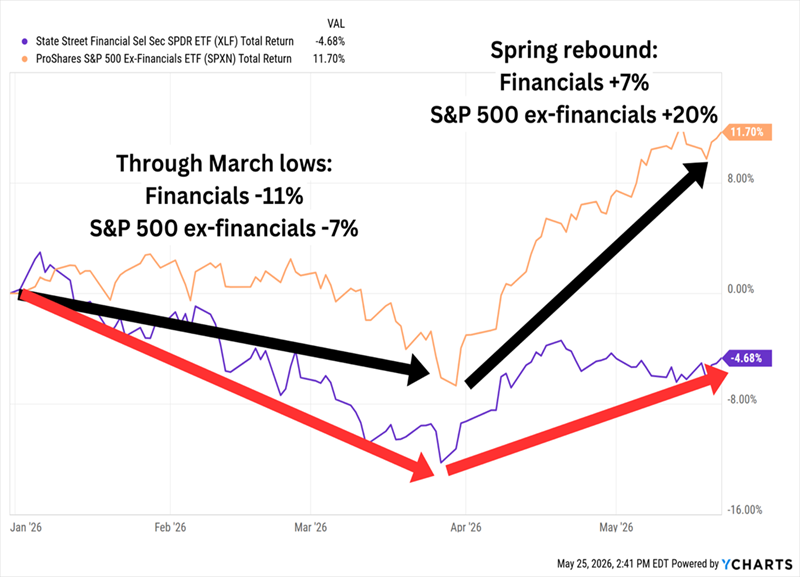

Financials are in the tank. They are the dogs of 2026 thus far. A proposed national cap on credit card interest rates spooked mega-banks like Citigroup (C) and integrated card companies like Capital One Financial (COF). Then, advances in artificial intelligence sent shockwaves throughout the software industry, stoking a panic among private lenders like business development companies (BDCs) as well as traditional banks. So, these stocks are weak:

Weak on the Way Down, Weak on the Way Up

While the broader market bounces on anticipated “good Iran” news, regional banks, insurance companies, and investment firms are waiting their turn.

Generally speaking we don’t buy banks for dividends. XLF—the go-to financial ETF—pays a measly 1.5%. But when we step off the beaten path, past the “Big 4” Wall Street banks and investment centers, we can collect wild yields of anywhere between 4x and 8x that.

The 7 bull-market holdouts I’m highlighting today are paying us between 5.7% and 12.3%. That means on average, a $500,000 investment across this financial mini-portfolio would pay us $44,000 a year in dividend income.

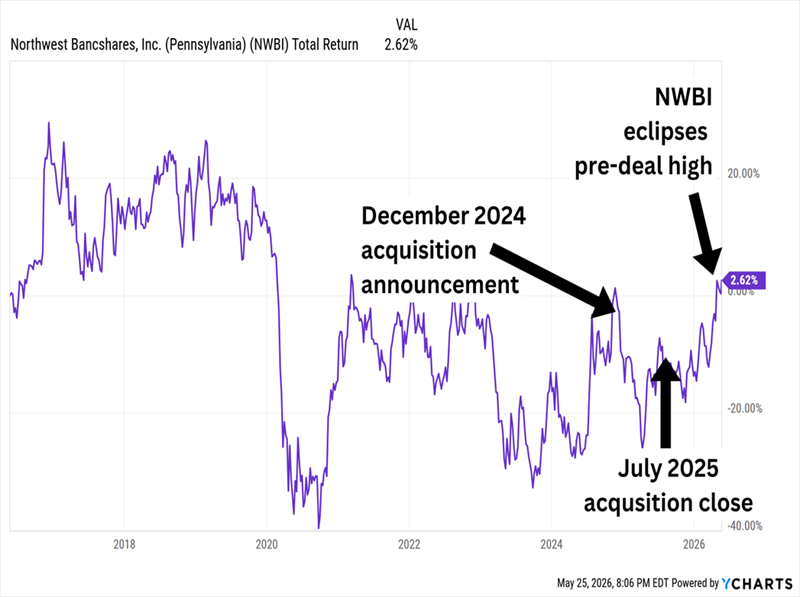

Northwest Bancshares (NWBI, 5.7% dividend yield) is about as unglamorous as banking gets—and that’s exactly the point. The company behind Northwest Bank runs more than full-service 150 branches across Ohio, Pennsylvania, New York and Indiana, and it has built its reputation on one thing: not blowing up. Lower-risk loans, steady capital, low volatility. Boring in the best possible way.

But what Northwest has long offered in fundamental stability, it has lacked in growth prospects.

The 2025 completion of its merger with Penn Woods Bancorp could help. It wasn’t a mega-deal, but it added scale and offered the potential for a bottom-line lift. The bank has also been successfully growing its commercial and industrial lending business.

NWBI Shares Have Returned to Multiyear Highs

Even though NWBI has bucked the financial sector’s 2026 weakness, shares still trade at just 10 times this year’s earnings and yield nearly 6%.

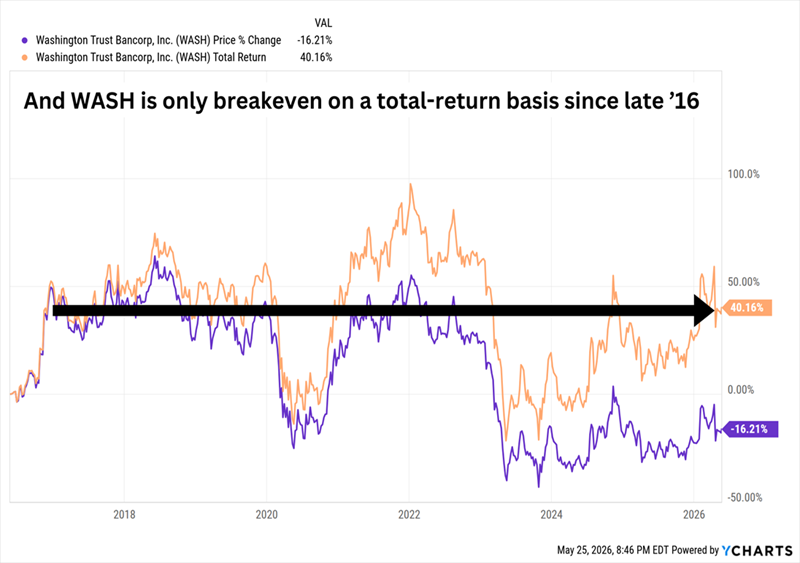

Washington Trust (WASH, 7.0% dividend yield) is another regional bank, and despite the name, we won’t find it in Washington, D.C., nor Washington State.

Instead, this 225-year-old financial institution—headquartered in Rhode Island and also serving nearby Connecticut and Massachusetts—is named after the nation’s first president. In fact, it proudly claims that it was “the first bank to print George Washington’s likeness on currency—69 years before President Washington appeared on the federally issued one-dollar bill and 132 years before the Washington quarter appeared.”

This small-cap dividend payer has ebbed and flowed over the past decade but ultimately trended downward.

WASH Has Only Delivered a Positive 10-Year Total Return Because of Its Dividend

2026 has been a microcosm of the Washington Trust shareholder experience. Earlier this year, WASH shares bounded after the company delivered a Street-beating Q4 report featuring improved net interest margin (NIM). But the stock lost a lot of that ground in April when its Q1 numbers flew in under estimates thanks to lower loans and deposits and two commercial real estate loans being moved to nonaccrual (the borrower has stopped making payments, usually for at least 90 days).

The good news? WASH is still solidly up for the year, profitability is headed in the right direction again, shares trade around 10 times this year’s earnings estimates, and the stock is paying around 7%.

A real tell for this stock will be a positive change in the dividend. Washington Trust delivered years of robust payout growth through early 2023, but the distribution has been stuck in neutral since then.

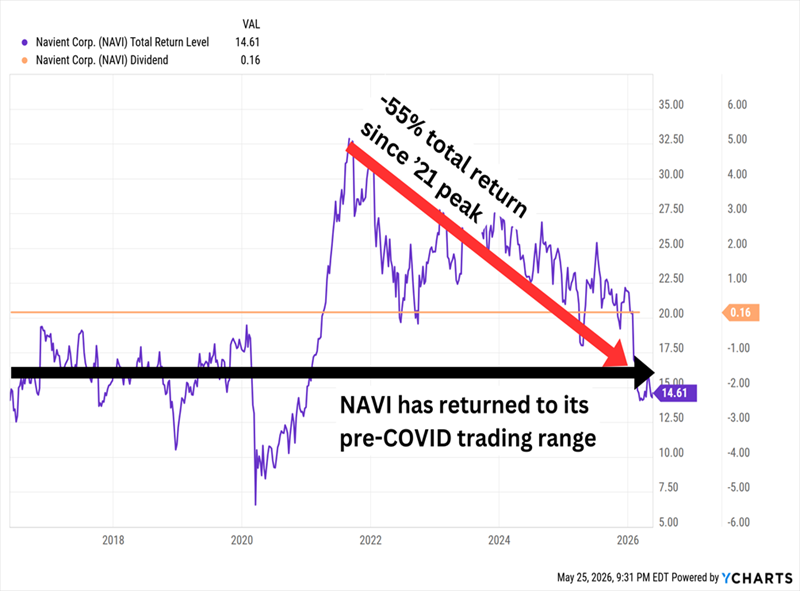

Navient (NAVI, 7.6% dividend yield), an educational loan servicer and collector that was split apart from Sallie Mae in 2014, sounds like a layup. Student debt is an American institution at this point—costs keep climbing, balances keep growing.

But Navient’s share chart would like a word.

The Post-COVID Rally in the Student-Debt Name Has Crumbled

Navient has been through it. In 2024, the company paid $120 million to settle longstanding allegations of illegally servicing federal student loans and was banned from servicing federal student loans ever again. That same year, it sold off its healthcare services business, then it unloaded its government services business in 2025. What remains is consumer lending.

As of April 2026, Navient is being led by CEO Edward Bramson, an activist investor who has served on the board of directors since 2022.

After losing an adjusted 35 cents per share in 2025, the company is expected to return to an adjusted profit of 72 cents this year, then grow the bottom line by more than 30% in 2027. After losing a third of their value in 2026, NAVI shares now trade at 12 times this year’s estimates and 9 times next year’s.

That price, though, is buying a company still mid-reinvention—new CEO, stripped-down business model, and a dividend that has sat frozen for a decade. Navient might be turning the corner. But we need to see some proof before we jump in.

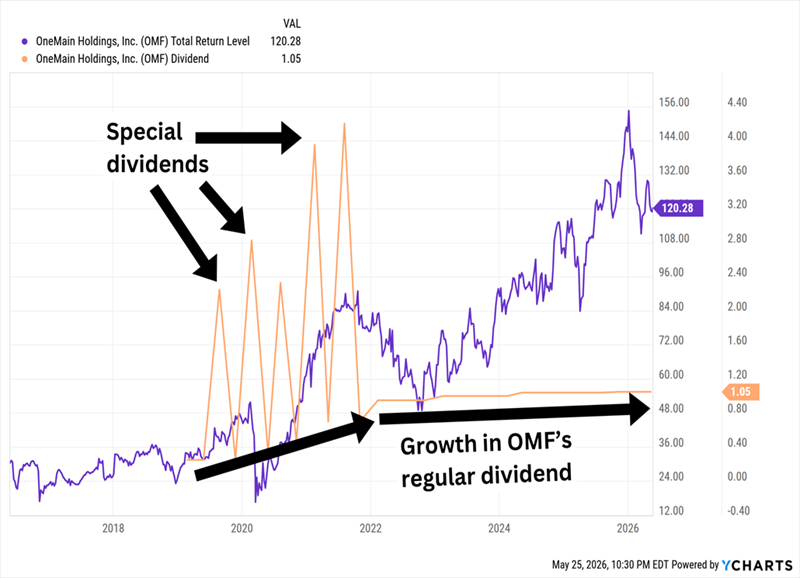

Want a cleaner dividend story? OneMain Holdings (OMF, 7.9% dividend yield) has one. The company didn’t start paying quarterly cash distributions until 2019—but since then, it has raised that payout every single year on an annual basis without exception.

OneMain provides personal installment loans to millions of Americans, many of whom have nonprime credit scores. Its lines include both secured and unsecured loans, as well as auto finance, credit cards and some insurance products. It’s an unconventional financial provider, but its physical footprint—1,300+ branches in 44 states—is on par with a decent-sized national bank.

I wrote a few years ago that OMF grew like a weed during COVID. While the bottom line has been more tumultuous since then, net interest income has continued to climb.

So Have OneMain’s Stock Price and Dividends

That said, OneMain’s clientele tends to be middle- and working-class consumers, and many of its products are on the high-risk end of the consumer finance spectrum. As a result, OMF is much more strongly tied to the economy and sentiment than the average bank. That has weighed on shares, as has a multistate lawsuit alleging the company packed additional products into loans, hiding their true all-in costs.

The flipside of that risk is that any jolt to the economy could benefit OMF more than most within the sector. Meanwhile, shares trade at just 7 times earnings estimates and a nearly 8% yield.

Two more of the sector’s highest yields (outside BDCs and mREITs) belong to Old Republic International (ORI, 9.6% dividend yield), a “special dividend“ specialist, and Western Union (WU, 11.2% dividend yield), one of Wall Street’s most hated stocks right now.

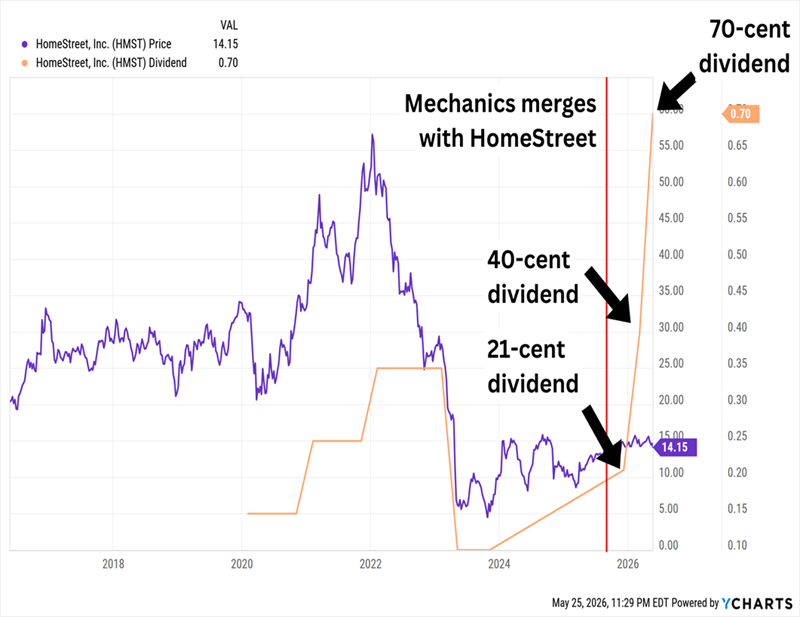

But the top headline yield on my radar belongs to Mechanics Bancorp (MCHB, 12.3% dividend yield), a regional that has been around for more than 120 years, but that has only traded on a major exchange since 2025, when it reverse-merged with HomeStreet.

Mechanics is a West Coast regional bank with 166 branches “spanning from San Diego to Seattle.” It’s a stellar deposit base that MCHB has turned into a profit-printing machine. It’s also majority-owned by Ford Financial Fund, a private equity fund that specializes in community banks and has a great M&A track record. Shares aren’t cheap, but they’re fairly priced at 14 times this year’s earnings estimates and 12 times 2027’s.

Mechanics is now focused on shedding unwanted products and accounts it inherited from HomeStreet, as well as achieving other cost savings from the merger. But management has made it clear that rewarding shareholders is a high priority, too.

HomeStreet Dividends Disappeared in 2023. In 2025, Mechanics Brought Them Back.

Overall expectations for MCHB’s future dividends are high, but fair warning: That 12.3% headline number comes with an asterisk.

Mechanics only reintroduced its dividend in late 2025, and it has moved fast—21 cents, then 40, then 70, all in rapid succession. I’ve averaged those three distributions and annualized the result to arrive at 12.3%.

Why not annualize the 70 cents (for a 19.8% yield)? Because that likely won’t be the payout going forward.

In Mechanics’ Q1 2026 earnings call, management said that longer-term, they’re expecting to pay out about 80% of net income as dividends. Based on 2026 expectations, that would come to about 82 cents for the year, which we’ve already blown past. If it keeps to that target in 2027, we’re looking at closer to 98 cents, which still represents a generous 7% yield with a real growth engine behind it.”

Earn 11.4% Annually, Escape the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

The problem? Every few years, the market will dip and force you to sell more shares when prices are low. That means when shares rebound, you need an even bigger gain just to get back to your original value.

That’s a sucker’s game.

The top 10 payers in my Contrarian Income Report pay 11.4% on average. That means even half a million dollars—much less than the talking heads say you need to retire—will pay out a massive $57,000 in annual dividend income.

And it’s scalable—the more money you have, the larger your paycheck, and the less chance you’ll ever need to touch your nest egg to get by in retirement.

Within a few weeks, even days, your portfolio could be spinning off double-digit dividends with the reliability of a Swiss watch … that’s because many of my CIR recommendations pay us every single month.

Well, imagine your portfolio in just a few days or weeks from now spinning off 8%, 9% and even double-digit dividends with the reliability of a Swiss watch… with many of my recommendations paying every single month no less!

Safe, retirement-sustaining yields are only the beginning. Click here today and I’ll not only introduce you to my favorite dividend payers—I’ll also provide you with two free special reports: Monthly Dividend Superstars and The Perfect Income Portfolio.