Inflation forever?

The fear has taken root seemingly everywhere: the media, the bond market, the futures market. They’ve all bought into the idea that scorching price hikes (and high interest rates) are here to stay.

If you’re like me, my fellow contrarian, you’re paying attention—but you also know something else about times like these: When everyone expects something to happen, something else usually does.

That’s what I want to talk to you about today. Because all the data I’m watching tells me the crowd is wrong: It’s deflation, not inflation they should be focused on.

Falling rates, not rising rates.

This disconnect has put some top-quality “preferred” (hint!) 7%+ dividends on the outs, giving contrarians a chance to buy cheap and “lock in” their high yields. Let’s get into it.

Inflation “Groupthink” Runs Deep

Let’s start where everyone looks when talking inflation and rates: the bond market.

The 10-year Treasury yield sits just under 4.5%. The 30-year yield is right around 5%, where it’s been for weeks. That’s a headache for anybody looking to borrow money (including Uncle Sam, with his already bloated credit card!).

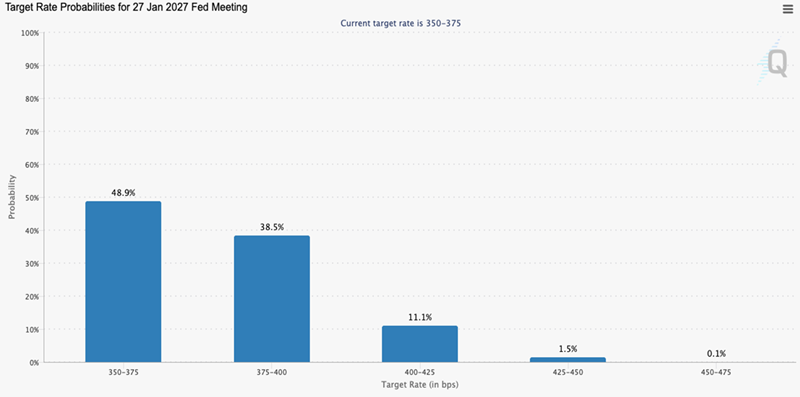

Futures traders, too, have bought in. They see the Fed keeping rates where they are for the next six months or so. Then, by a slim majority, a rate hike in January:

Source: CME Group

That looks like a pretty airtight argument for higher rates, right?

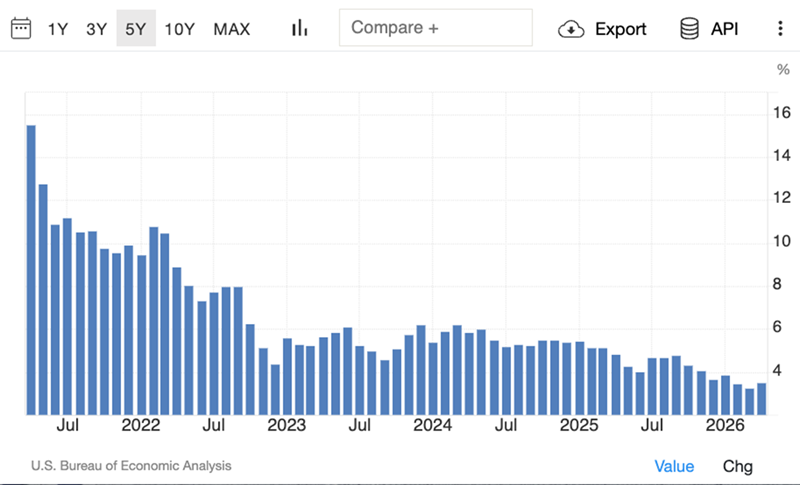

Except, well, here’s the other side of things, starting with wage growth, which has been trending one way since the pandemic: down.

That’s clearly deflationary—and April’s rate of 3.6% fell behind the CPI. When that happens, people do one thing: cut back. The cure for high prices really is high prices!

Then there’s AI, which is an anchor on hiring. According to an April 2026 Goldman Sachs study, AI slowed monthly payroll growth by 16,000 jobs in the US over the preceding year. But the numbers don’t really matter here. Just talking about replacing workers with robots will cause some folks to sit on their wallets.

Iran? Neither it nor the US can afford to let this situation fester. Sooner or later, the strait will reopen. The oil will flow—and inflation will ease when it does.

And let’s not forget, we’ve got Kevin Warsh settling in at the Fed. The administration wants him to cut rates, and he’ll likely do so as soon as he can justify it.

But even with all this, investors still think inflation is here for the long haul. Let’s call that out with two 7%+ paying funds—including one with a payout that’s growing.

Inflation Fears Put These “Preferred” 7%+ Dividends on Sale

A couple weeks ago, we highlighted corporate-bond closed-end funds (CEFs) as timely plays on this situation, and they still are. Now let’s peer into another discounted corner of CEF-land: preferred shares.

The best way to think about preferreds is as stock/bond hybrids. They trade like a stock, and they pay dividends. But like a bond, they tend to trade around a par value, and the payout is usually fixed.

One more thing about those payouts: They’re typically a lot higher than those on a company’s common shares—regularly two or three times higher.

And like bonds, preferreds—or CEFs that hold them—are oversold today. That’s because while bond yields have risen with inflation fears, their prices have fallen (because prices move inversely to yields).

But as is the case with bond CEFs, these discounts have gone too far with preferred funds. That’s our cue.

A “Hybrid” Fund Trading for 12% Off (and Yielding 7.7%)

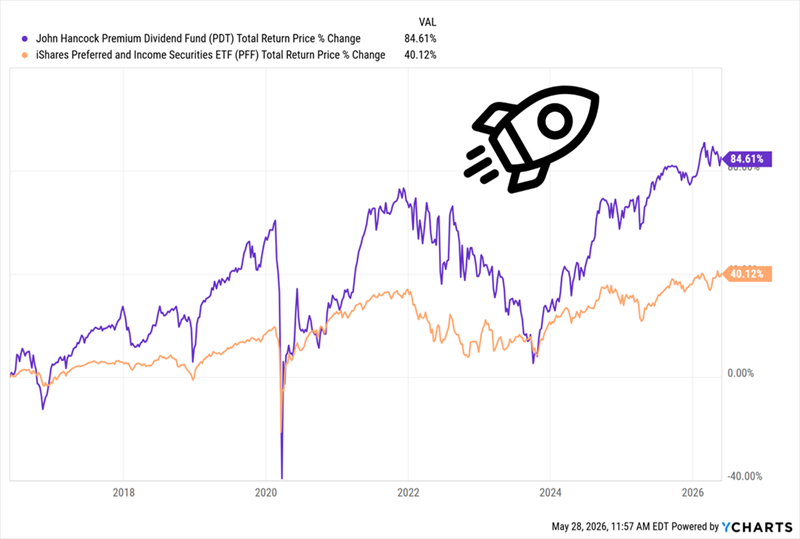

The 7.7%-yielding John Hancock Premium Dividend Fund (PDT) is a good place to start with preferreds because it’s a “hybrid,” investing 43% of its assets in common stocks, 30% in preferreds and 26% in bonds and other income securities.

That strategy has paid off, with the PDT’s common shares helping power the fund’s total return (in purple below) past the preferred-stock benchmark iShares Preferred and Income Securities ETF (PFF) in the last decade:

PDT’s “Hybrid” Portfolio Gives It a Boost

PDT also boosts its returns (and by extension an investor’s dividends and preferred-stock exposure) with leverage, to the tune of around 34% of its portfolio.

That would send many vanilla investors to the exits, with today’s interest rates. But we know this is a feature, not a bug: As rates fall, PDT’s borrowing costs will, too—as that rate decline boosts the value of its fixed-income portfolio.

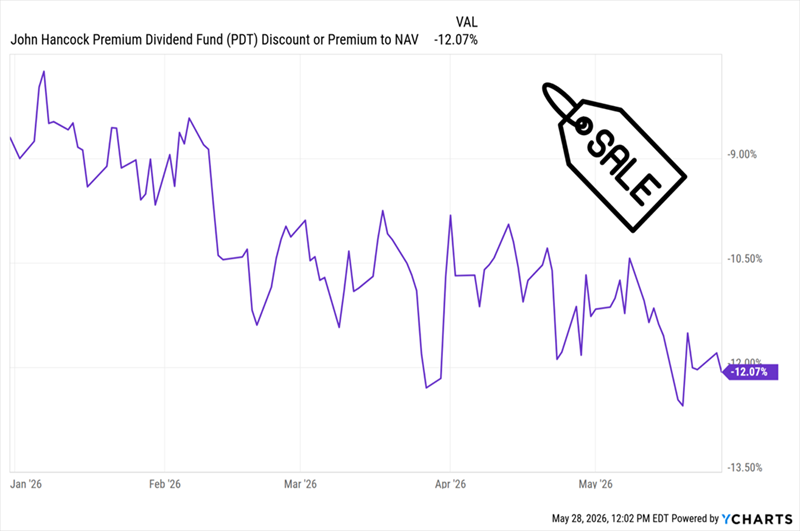

Meantime, this smartly built fund is available at a 12.1% discount to net asset value (NAV, or the value of its underlying portfolio) as I write this. You can see that discount widening as the “inflation forever” mindset took hold this year:

PDT Gives Off a Clear Contrarian Buy Signal

That’s a particularly sweet deal when you consider that PDT has, on average, traded around par over the last five years. A discount this deep is rare, and I don’t expect it to last in light of the steady 7.6%-yielding (and monthly paid) dividend PDT offers.

This 8.6% Dividend Is On a Growth Tear

The Flaherty & Crumrine Dynamic Preferred & Income Fund (DFP) is a “purer” play on preferreds than PDT, with 51% of its portfolio in these shares as of February 28. The rest is 45% bonds and around 4% convertible bonds and cash.

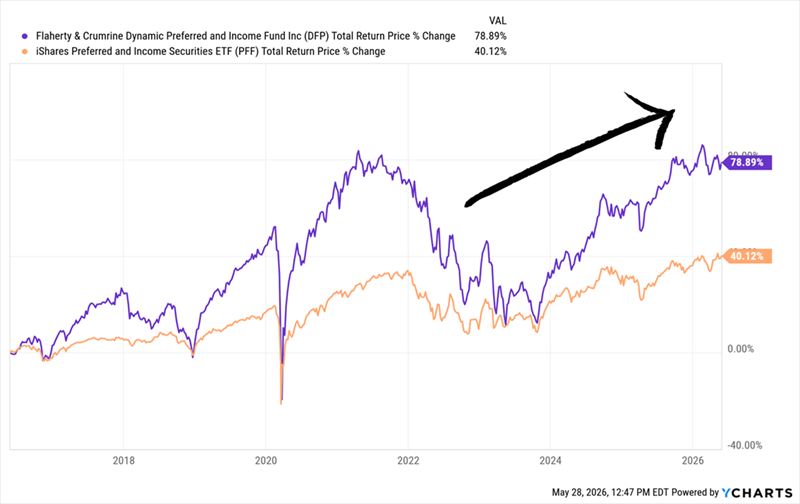

But even without PDT’s common-stock “afterburner,” DFP (in purple below) has still cleanly beaten its benchmark ETF, PFF, over the last decade, by nearly the same margin.

DFP Easily Beats Its Benchmark

This performance shows why “human” preferred-fund managers won’t be replaced by AI. The preferred market is small, and personal connections are key to getting in on the hottest new issues. And F&C, which has been in fixed income for more than 40 years, has one of the deepest contact lists out there.

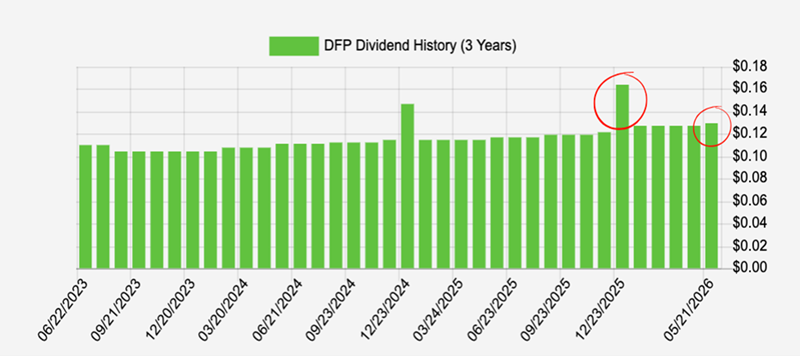

The fund’s strong return also supports its 8.6% dividend (again paid monthly), which has grown since DFP emerged from 2022’s inflation spike.

Management clearly sees through the current rate scare: It delivered a special dividend at the end of last year and hiked the regular payout again with the latest payment:

DFP’s Dividend Grows—and Shrugs Off the Fearmongers

Source: Income Calendar

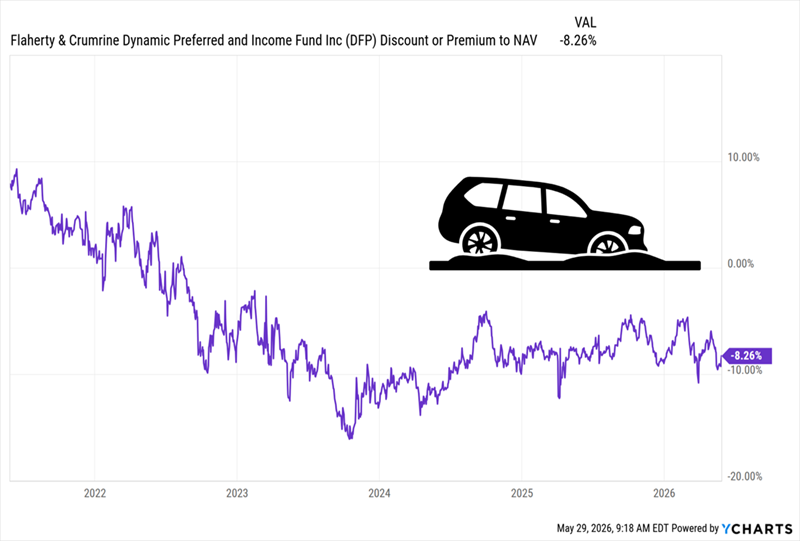

That’s great for DFP shareholders, but what management is likely really trying to do here is narrow the fund’s discount, which has slumped to 8.3% in the last few years and has been stuck there since. Special payouts and dividend hikes are great ways for them to signal confidence and draw more buyers in.

DFP’s Discount Is Spinning Its Wheels (for Now)

My prediction? They’ll be successful—and the fund’s high, and growing, monthly payout will put a floor under DFP’s discount and let investors pocket the fund’s growing income stream in peace.

Then, when today’s inflation scare ebbs, yields on existing fixed-income assets will slide, increasing the value of DFP’s portfolio and pushing its discount back toward par, where it was before the 2022 mess.

An 8.6% Payout Is Fine … But It Pales Next to This 11% Monster

My top play on this overdone inflation panic sports a payout far bigger than even DFP’s 8.6% income stream.

This fund—a top buy from the portfolio of my Contrarian Income Report service—yields 11% now. And its monthly payout has been rock-solid—with management sweetening the deal with two special dividends and a hike on top of that.

I expect this one to surge alongside our two preferred funds when investors see reason on the inflation argument. While we wait, we’ll collect that stellar 11% dividend, in the form of steady payouts every month.

I’ve put further details on this unloved (for now) income play into a special bulletin you can read here. You’ll also get a free Special Report revealing this fund’s name, ticker, and my complete analysis of its portfolio and strategy.

The time to buy this 11% payer is now. The longer you wait, the more monthly income you leave on the table.