You might think a $500,000 nest egg isn’t enough to retire on, and I wouldn’t blame you. The financial media loves to tout $1 million as the end-all be-all mark of financial security.

But today, I’ll show you how wrong they are, and how secure you can be even with just half of what “conventional wisdom” says you need – as long as you’re in the right kind of dividend stock.

And I’ll also show you exactly what kind of dividend stocks you need to get the job done and the bills paid.

Those bills, by the way, come every month. You and I both know this – for me, the mortgage is due come the 4th, electricity on the 10th, have been for years. But some people somehow forget this when planning out their portfolios. The result? Their motley crew of quarterly dividend stocks results in “lumpy” distributions where some months are heavy, and others are thin.

I prefer a nice, steady stream of monthly income I know I can count on. And you can get that, as the name would suggest, from monthly dividend stocks.

I’m currently targeting a collection of eight monthly dividend payers that yield an average of 7.9% and deliver that income every 30 days or so. So it’s not just consistent income – it’s hefty, retirement-sustaining income. These stocks can deliver roughly $3,300 in dividends every month on a $500,000 portfolio, not to mention upside potential you can use to help grow your nest egg, and thus reap even more in regular dividend checks!

There’s only one cap on my strategy: If you’re already a billionaire, this list can’t help you. That’s because these Goldilocks payers are simply too small to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

But which monthly dividend payers make the grade?

Realty Income (O)

Dividend Yield: 4.5%

Any discussion of monthly dividend companies needs to start with … well, “The Monthly Dividend Company.” That’s the self-given moniker of Realty Income (O), the premier single-tenant real estate investment trust (REIT) with an unimpeachable dividend track record and a steady payout every 30 days or so.

A quick summary for anyone new to this company: Realty Income operates more than 5,400 properties across 49 states and Puerto Rico across 257 tenants spanning several dozen industries. Its tenants take on triple-net-lease agreements, which means they’re not just responsible for rent, but also things such as building maintenance and taxes – something that makes Realty Income’s bottom line extremely predictable.

Moreover, Realty Income is one of several stocks on the precipice of becoming a Dividend Aristocrat, with 24 consecutive years of payout increases under its belt – just one shy of the 25-year mark. That has come in the most impressive of manners: namely, 83 consecutive quarterly increases that no other company can boast.

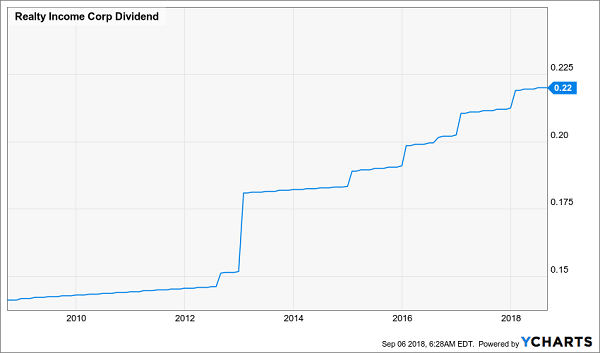

Realty Income (O): A Dividend Chart Unlike Any Other

And yet, there’s still reason for pause in this venerable dividend play.

I warned about Realty Income in 2016, and it’s off about 13% since then while the broader market has sprinted nearly thrice as fast, at 35% gains. O is at least on the rebound this year, with about 3% gains … but still underperforming the market.

Revenues and FFO still are headed in the right direction (up), though the latter has slowed a bit from previous years. No, my concern is longer-term. While O has a pretty diverse tenant base, consider how many names in its top-20 tenants are targets of Amazon.com (AMZN): Walgreens (WBA), Dollar General (DG), Dollar Tree (DLTR), Walmart (WMT), BJ’s Wholesale (BJ), CVS Health (CVS), Kroger (KR), Rite Aid (RAD) and Home Depot (HD). That’s roughly half of its tenants, accounting for almost a quarter of revenues. And again, that’s just in the top 20!

Is Realty Income in existential danger? Of course not. But its path to growth is significantly hindered, which means the dividend is really all you can count on year in and year out.

iShares iBoxx $ High Yield Corporate Bond ETF (HYG)

SEC Yield: 5.6%

Exchange-traded funds (ETFs) are much like stocks in that the majority pay out quarterly, but you can still find some monthly payers, especially among bond funds.

Enter the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) – the most popular junk-bond ETF in the game. It holds roughly a thousand junk-rated bonds, mostly between three and 10 years in maturity, and mostly in the BBB and BB ratings spheres – so it’s junk, but it’s primarily higher-tier junk.

The resulting 5.6% yield is nice. So are the monthly payouts.

That said, there’s better out there. I’ve recently broken down the HYG, exposing a number of flaws, from high concentrations in lousy lenders to a false sense of security in its so-called “liquidity” (it’s not really as liquid as investors would like to think).

I’ll make this short: You’re much better off in closed-end funds for this kind of exposure, monthly dividends or not. Next.

Shaw Communications (SJR)

Dividend Yield: 4.6%

I firmly believe you can find good yields in international stocks, but I have to admit it’s difficult to find a good dividend schedule abroad. At least most U.S. companies have the common decency to pay at least quarterly – many stocks in Europe, South America and Asian only pay twice a year, sometimes even just once!

From that perspective, Shaw Communications (SJR) is every bit as friendly and accommodating as the good people of its home country, Canada.

Shaw Communications is similar to America’s AT&T (T) and Verizon (VZ) in that it’s a massive, multi-product communications titan that offers not just telephone, but internet, TV and other services across several provinces. That should, in theory, make Shaw fairly dependable … but as AT&T has discovered in 2018, even controlling a significant market share in telecom doesn’t always guarantee consistent stock returns.

SJR is off 15% this year as it tries to navigate a “total business transformation” in which it’s trying to wean itself off reliance on its wireline operations, and instead bulk up its wireless business. That’s far from the only pain Shaw has absorbed in connection to the transition – 3,300 employees have been eliminated via buyouts (that’s about 25% of its workforce!), and the company took a $450 million charge, to boot.

Shaw managed to beat fiscal Q3 estimates when it reported at the end of June, but even still, all is far from rosy. CEO Bradley Shaw detailed a laundry list of issues that hampered the company:

“There are a number of items that impacted our results this quarter, particularly internet, including seasonal student disconnect activity that typically reverses in Q1, a shift in some bulk accounts from consumer to business, and continued market dynamics, including attractive promotions by the competition and our pricing discipline, all of which contributed to our lower sales activity in Q3.”

The monthly dividend certainly is nice, and the yield puts it on par with Verizon and AT&T. But its positioning – it not only must compete against the likes of Rogers Communications (RCI) and Telus (TU) on the ground, but the stock is priced less attractively than those companies – and current state of flux make it less reliable than America’s telecom duopoly.

Shaw Communications (SJR): Monthly Dividends, But Not Much Else

Apple Hospitality REIT (APLE)

Dividend Yield: 6.8%

The “other Apple (AAPL)” is nothing like the trillion-dollar tech company … and yet they share one very attractive investing trait.

Apple Hospitality REIT (APLE) – surely the bane of countless investors trying to get to the ticker page of their favorite iPhone maker – is actually a hospitality REIT whose properties are split between the Hilton (HLT) and Marriott (MAR) umbrellas. That means its 30,700 guest rooms in 241 hotels fall under brands such as Hampton Inn, Embassy Suites, Fairfield Inn and SpringHill Suites, among others.

The businesses couldn’t be more dissimilar. And yet, like Apple Inc., Apple Hospitality REIT is an operational growth machine.

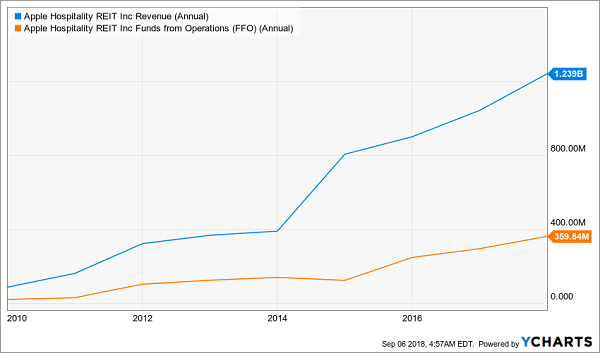

Apple Hospitality REIT (APLE) Is Growing Unchecked

The company has delivered impressive growth over the years. Since 2013 alone, revenues of 388 million and funds from operations (FFO) of $137 million have rocketed to $1.2 billion and $389 million, respectively. FFO has grown every year but one since 2010 – that’s consistent excellence I can get behind!

Shares are essentially flat over the past two years, but they’re bound to gain speed once Wall Street realizes what it’s missing out on: not just growth, but a generous yield despite extremely conservative dividend management. The company delivered 51 cents per share in modified FFO last quarter alone, versus a 10-cent monthly dividend. That’s a payout ratio of less than 60%, meaning investors have no reason at all to worry about the survivability of this dividend.

My Top 8 Monthly Payers for 8.0% Dividends, Plus Upside

My all-star retirement portfolio contains 8 of the absolute best preferred stocks, REITs (real estate investment trusts) and CEFs (closed-end funds) out there. It’s well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, relentless dividend growth means your 8.0% yield will be more like 10% in short order.

You don’t need a million dollars to be comfortable in retirement. In fact, using this portfolio, you can be well on your way to security and comfort with just a half-million dollars to invest! And again, you never need to worry about budgeting around “lumpy” dividend payouts where you’re “rich” in January but get just a trickle of cash in March. These monthly dividend payers will ensure a smooth, steady stream of cash – you know, to tackle that smooth, steady stream of bills.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.