Real estate investment trusts (REITs) and their typically high dividend yields are a key part of a payout-powered retirement portfolio that’s built to dish out higher and higher dividends every single year.

The five REITs we’ll discuss today will pay you 4% to 7.3% per year in dividends alone. And this income stream will only grow as time passes, because these firms have growing cash flow streams they must pass on to shareholders in order to keep their privileged REIT status.

REITs may not get much mainstream coverage, but the academics are starting to catch on to these dividend machines. Last year, I pointed you to a study from Wilshire Research that showed “dramatic” results when REITs were added to a retirement portfolio.

Let’s also consider recent research from global benchmarking company CEM Benchmarking that shows publicly traded real estate has no equal in retirement-focused accounts:

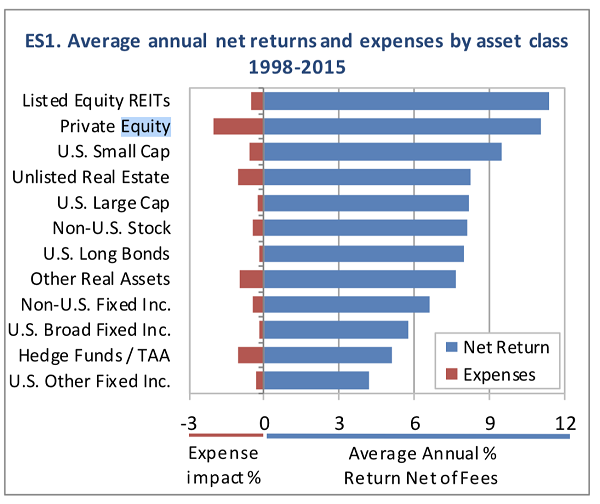

Equity REITs Are the Best of the Best

Source: Alexander D. Beath, PhD & Chris Flynn, CFA CEM Benchmarking Inc.

Their important finding: “Listed equity REITs had the highest average net return over the period, averaging 11.4%.”

Ready to retire? Stick with REITs. They’re the best asset class for retirees who, ironically, aren’t invested in them! More from CEM Benchmarking (emphasis mine):

Although they had the highest arithmetic average annual net return of 11.4 percent over the period, listed equity REITs were the least used asset class covered in the study. Allocations to listed equity REITs averaged just 0.6 percent of total assets.

If you’re looking to live off of dividends in your retirement, you must consider REITs. Here are five candidates that pay 4% and up today:

MGM Growth Properties (MGP)

Dividend Yield: 5.8%

MGM Growth Properties (MGP) is a relatively new kid on the block in the REIT world, spun off of MGM Resorts International (MGM) in 2016. This REIT owns seven Las Vegas properties including Mandalay Bay, Luxor and the Mirage; a handful of regional resorts in places such as Atlantic City and Washington, D.C.; and a right-of-first-offer on an MGM property being built in Springfield, Massachusetts.

I like this regional coverage for two reasons:

- It provides diversification against Las Vegas’ inevitable ups and downs.

- It gives MGM and MGP exposure to the eventual boom that I expect to see across the rest of the U.S. as other states begin to legalize sports betting.

I also like what I see in examining MGP’s dividend: The REIT has hiked its payout four times in nine quarters, and the company has done so with a very reasonable payout ratio of just under 80%.

Just remember: The success of gaming stocks and REITs is heavily tied to a strong economy, so all bets are off if America’s current economic boom starts to peter out.

Until then, game on.

MGM Growth Properties’ (MGP) Price Should Follow Its Dividend Higher

Gaming and Leisure Properties (GLPI)

Dividend Yield: 7.3%

Speaking of the virtues of regional gaming, Gaming and Leisure Properties (GLPI) is intriguing for its “pop” potential.

GLPI is another spinoff, carved out from Penn National Gaming (PENN) back in 2013. The company owns a few dozen regional casino and gaming properties in 14 states and leases them out on a triple-net basis to the likes of Penn National and Pinnacle Entertainment (PNK). Their six Mississippi properties may get a lift from the state’s new legalized sports betting, too.

Management seems to believe in their own stock, too. Gaming and Leisure Properties enjoyed some aggressive insider buying earlier this year. And Wall Street analysts are high on its growth prospects, too, modeling 7% EPS growth this year followed by a 22% burst in 2019.

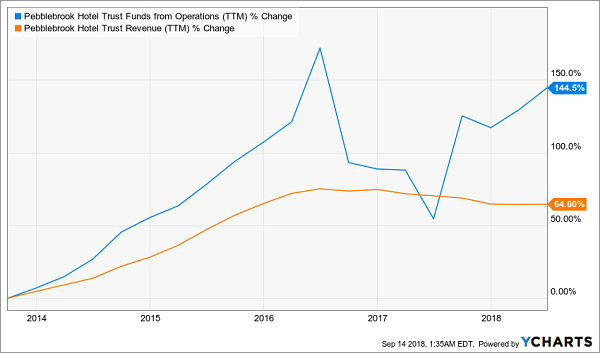

Pebblebrook Hotel Trust (PEB)

Dividend Yield: 4.1%

Pebblebrook Hotel Trust (PEB) is a play on another one of my favorite mega-trends: the “experience economy.” Americans increasingly seem to value experiences more than acquiring a mountain of stuff, and we’re especially seeing this trend play out in the ever-important (and affluent) Millennial generation.

Pebblebrook is a hotel REIT that targets the most important economic class: the rich. The United States’ middle class is shrinking rapidly, meaning you’re either chasing low-income Americans or the well-heeled – and you and I both know which route leads to fatter profits.

Pebblebrook has a tight portfolio of just 28 properties, but most of these house elite properties such as the LaPlaya Beach Resort & Club in Naples, Florida; the Hotel Monaco in Washington, D.C.; and the Hotel Palomar in Los Angeles. There’s some geographic diversity, though PEB’s properties are primarily crowded along the West Coast’s largest cities.

This is a potential turning point for Pebblebrook. This month, the company beat out Blackstone Group LP (BX) to buy up LaSalle Hotel Properties (LHO) for $5.2 billion, which will boost its portfolio of hotel properties to 66 – though the company’s expected to sell at least three LaSalle properties and execute other asset sales to tamp down debt.

This merger is a double-down on the strong U.S. economy. If America keeps it up, Pebblebrook stands to come out smelling like a rose.

Pebblebrook (PEB) Will Try to Spark Growth Through M&A

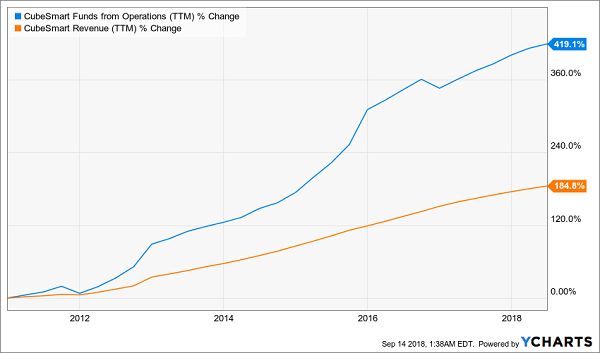

CubeSmart (CUBE)

Dividend Yield: 4.0%

Self-storage REIT CubeSmart (CUBE) is a model operator that continues to grow like a weed. It also has been a serial dividend raiser for years, boosting its quarterly payout by 217% over the past five years.

CubeSmart (CUBE): 419% FFO Growth Since 2010

Unsurprisingly, Wall Street has priced it at a premium.

CubeSmart owns 981 self-storage properties across the U.S., providing not just traditional personal storage solutions, but also business, vehicle and boat storage options. That gives it reach.

Demand comes from the very nature of CubeSmart’s business. Self-storage is an “anytime” industry – economic expansions see a greater need for storage as people accumulate more stuff, and economic contractions usher in a greater need for storage as people need to find a place to store their things as they scale back into smaller living quarters.

But what makes CubeSmart the dynamo you see today is a brilliant set of proprietary systems that help manage inventory and maximize space efficiency, as well as a sophisticated rate-increase system to help squeeze out more profits from customers while still retaining them for the long-term.

That’s how the company has more than doubled FFO over the past five years alone, and why analysts continue to project high-single-digit top-line growth over the next few years. That in turn should keep CUBE chugging higher, rain or shine.

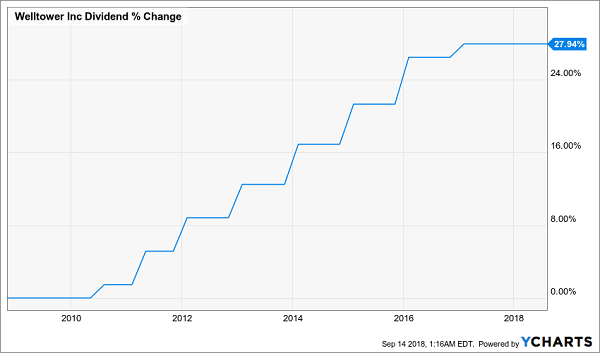

Welltower (WELL)

Dividend Yield: 5.2%

Baby Boomer plays will continue to be an investing gold mine for the next decade or more. America’s 65-plus population is expected to explode by 36% by 2025. In the REIT category, we can primarily play the boomers through either healthcare or senior living.

Welltower (WELL) gives us a little bit of both.

You might remember Welltower as Health Care REIT, but the company rebranded in 2015 (and changed its ticker from HCN in 2018), and has widened its focus over the past few years, too.

This monster of a real-estate company owns 1,502 properties. Importantly, 93% of NOI comes from private-pay sources, so Welltower’s success doesn’t hinge on what the government decides to do with programs such as Medicare and Medicaid.

The wild card to watch right now is a first-of-its-kind joint venture with top-15 U.S. health system Promedica, which includes a 15-year absolute triple-net master lease.

Under that system, Welltower is expected to generate 67% of net operating income coming from senior housing (under brands such as Sunrise Senior Living and Silverado), 16% from outpatient medical, 10% from long-term post-acute care and 7% from health systems.

Just keep an eye on the dividend: While the payout ratio is perfectly healthy at a little more than 80%, the payout didn’t come up at its normal time earlier this year. The company has one more quarter to keep up its streak of dividend hikes.

Income Investors Are Waiting on Welltower (WELL)

My Top 2 REIT Buys: Recession and Rate-Proof Landlords for 7.5%+ Yields with 25% Upside

These five REITs are laudable, but they’re not quite elite – not like my two favorite REITs, which are comfortably positioned in recession-proof industries.

They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what President Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender (a 7.7% yielder!) lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks, and then it sends most of the profits our way as dividends (a legal requirement to have REIT status).

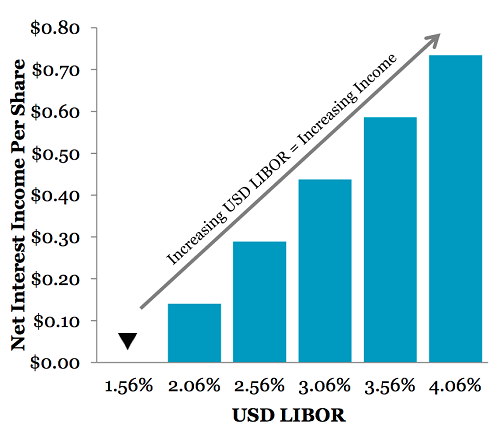

Better still, this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

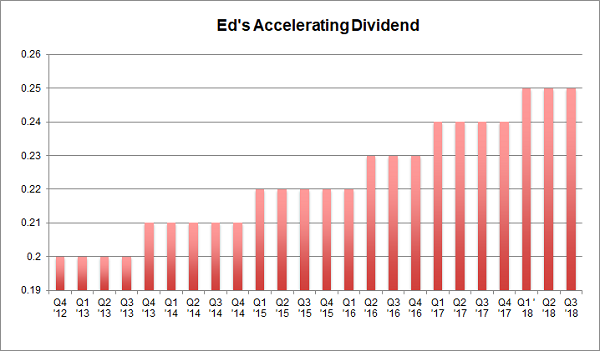

Another REIT favorite of mine is a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

Its founder Ed admitted that, 14 years ago, he had “zero assets, a dream, and a business plan.” Well, his dream and plan were plenty – the visionary entrepreneur parlayed them into more than $6.7 billion in assets!

Right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so it can afford to pay us shareholders more. And an accelerating payout is a flat-out cry for help!

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever. Click here and I’ll share how you can get a complimentary copy of my premium REIT research.