5 Stocks, A 10% Average Yield, And 60 Dividend Checks a Year.

Brett Owens, Chief Investment StrategistUpdated: July 18, 2025

Quarterly payers are the norm. But monthly dividends…. Yeah, that’s that stuff.

Today we’ll chat about five monthly divvies that yield between 5.8% and 16.3% per year. That’s right, these stocks pay early, often and heavy.

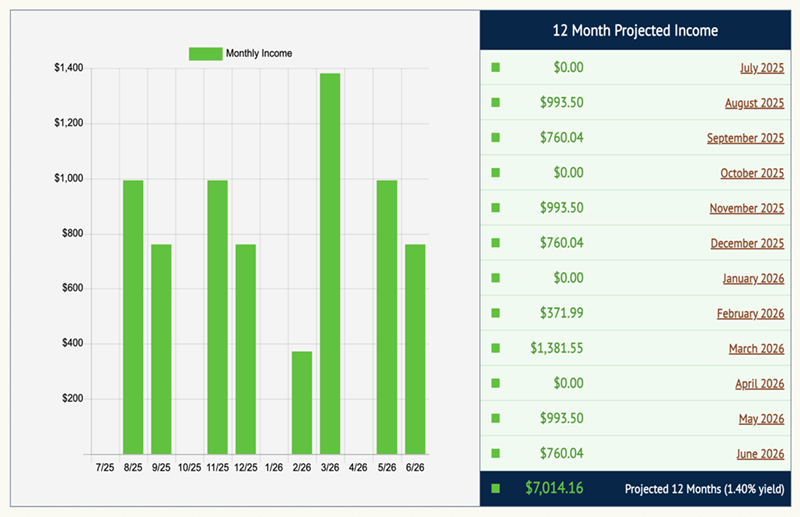

What’s wrong with a plain ‘ol quarterly dividend? Let’s consider using my Income Calendar dividend projection tool. If we put $100K into each of the top five stocks in the Dow Jones Industrial Average, here is the lumpy, inconsistent and sad income picture we are looking at:

Dividends From Top 5 Dow Stocks

Source: Income Calendar

Lumpy and, let’s be honest—lame.

Instead let’s consider our five monthly payers.… Read more