REITs (real estate investment trusts) are finally starting to get the respect they deserve. As a result, a cool $100 billion is gearing up to chase these soon-to-be-hot issues!

Since its 2004 inception, the Vanguard REIT Index ETF (VNQ) crushed the broader market – returning 192% including dividends versus just 89% for the S&P 500. The market gods have finally taken note.This September, Standard & Poor’s will give REITs their very own sector for the first time.

Which means NOW is the best time to buy them, because before it’s official, large funds will be shoveling cash into REITs as they attempt to “front run” the index as they always do. It’s JP Morgan & Chase reporting that the desire for “equal weight” portfolios will send $100 billion or so into the sector.

If you’re looking to get ahead of the game, Barron’s writes these five stocks will be in the new index…

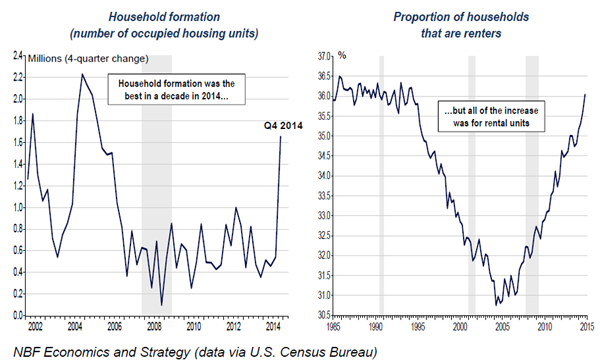

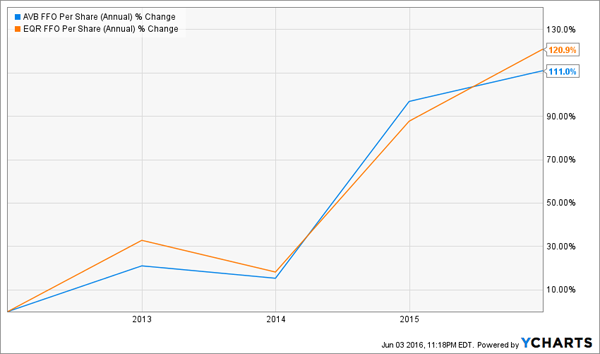

AvalonBay Communities (AVB) and Equity Residential (EQR) both invest in apartment properties, which have been in high demand. New household formation is at its highest levels in a decade – and unlike previous generations, these new familiars are renting rather than buying:

Mortgage? No Thanks

Over the last 5 years, both stocks have increased their payouts by about 50% – and both pay about 3% today. And their funds from operations (FFO) per share have actually accelerated even faster in recent years, providing a solid foundation for future dividend boosts.

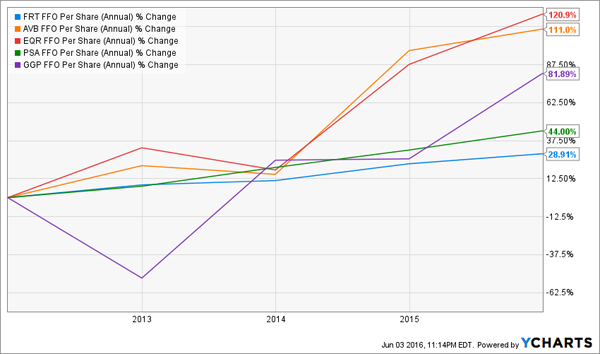

A Good Time To Be a Landlord

As new millennial families rent homes, the boomers continue to rent places for all their “stuff” – which benefits outfits like Public Storage (PSA). Occupancy levels for self-storage facilities are now north of 90%, and PSA raises its rent by about 3% annually. These trends helped drive 89% dividend growth over the past 5 years. And shares pay 2.8% today.

Federal Realty Investment Trust (FRT) develops and rents high-end retail properties, with a focus on large efforts that span several years. It’s grown its payout by 40% over the past five years, and the firm has boosted its dividend every year for the last 50! Shares yield 2.4% today.

Finally General Growth Properties (GGP) owns, develops and operates shopping malls with similar a focus on high end properties in destination locations such as Honolulu, Los Angeles, Chicago and Washington D.C. Retail at large may be hurting, but this “rich niche” strategy is quite profitable for GGP. It’s increased its FFO per share by 82% over the last five years while boosting its payout by 90% over the same time period. Shares pay 2.8% today.

REITs are required by rule to pay out the majority of their earnings to investors in the form of dividends. Rising FFO tends to drop straight to the bottom line, so it’s no surprise these five have boasted big cash flow growth to power their rising payouts:

Rising FFO Makes These REITs Popular

These stocks were good investments over the past five years, with three of them beating the S&P 500 and top performer PSA more than doubling up the index. But positive past performance can weigh on future gains, and PSA’s yield is as low as it’s been since 2010 – the curse of popularity.

In fact four of the five are trading for more than 20-times FFO, with PSA and FRT near 30-times. These issues may get a pop as funds rush to add them before they get indexed, but cheaper REITs with higher yields, similar dividend growth and cheaper valuations should benefit even more.

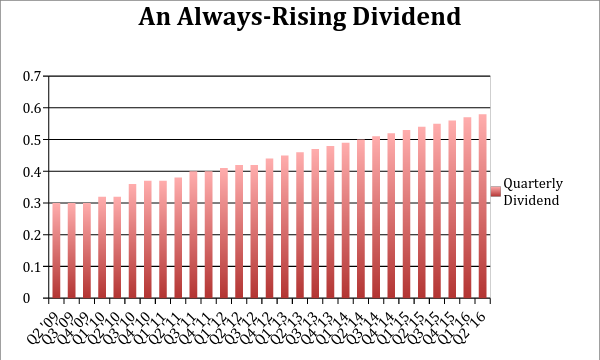

My favorite REIT to buy today just raised its dividend again by another 2% over last quarter’s payout. This marks the 15th consecutive quarterly dividend hike for the firm:

It pays a 7.1% yield today – but that’s actually a 7.6% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times funds from operations (FFO). Pretty cheap.

The headline risk that first-level investors have been fretting over is lesser-competitor HCP (HCP). It’s one of the most widely followed – and poorly run – companies in the industry, with a long history of tears and disappointments.

Long-time HCP investors will brag about their 100% returns over the last 10 years including dividends. But that’s nothing to brag about, as my favorite healthcare REIT returned 400% over the same time period! When looking at HCP’s results, the real question to ask is: “Why haven’t they profited more over the years?”

HCP’s poor earnings reports took down “by infection” this stock by 25% in February and 15% in May. Soon, its superior management will shine – for now, we need to take advantage of the buying opportunity before the funds come rushing in. Click here and I’ll give you the details about this stock and the megatrend that’s driving its relentless dividend growth.