Rising rates have sunk bond prices—and sent their yields higher.

The upshot? Now is a good time to add high-quality corporate bonds to your portfolio. And if you do so through one closed-end fund (CEF) we’ll name in a second, you’ll be able to do so with a 13.4% dividend that grows.

To be honest, bonds have already started to rise, and we’ve been taking advantage in my CEF Insider service. In October, for example, we picked up the Nuveen Core Plus Impact Fund (NPCT), which yields 11.3% today. We’ve grabbed a 6.8% return so far, including one dividend payout of 10 cents a share. (NPCT, like most CEFs, pays dividends monthly.)

Don’t fear, though. You haven’t missed the boat here; there are plenty of reasons to think our opportunity has room to run yet. The Fed, for one, is likely to press “pause” on rate hikes early next year, another bullish sign.

What’s more, one of the most successful bond buyers in the business continues to pound the table. This is where our 13.4%-dividend opportunity comes in.

Buy Alongside the “Bond Behemoth”

That would be PIMCO, which has over $2 trillion in assets under management. The company has been around for half a century and has seen just about every kind of market you can imagine—up, down, sideways, boring and irrational. And PIMCO loves bonds now. Here’s what CIO Dan Ivascyn recently said in a meeting with PIMCO analysts and portfolio managers:

“Value has returned to the fixed-income markets. Just thinking about nominal yields, we’ll start here in the United States. Across the yield curve now, you could lock in a very high-quality bond yield today. You could look for very high-quality spread product and very easily put together a portfolio up in the six, six-and-a-half percent type yield range, without taking a lot of exposure to economically sensitive assets.”

In other words, Ivascyn sees a lot of opportunities to get up to 6.5% yields in this bond market with little effort, which suggests that a little effort could push that yield higher. PIMCO itself has done this with that 13.4%-yielding fund I mentioned off the top: the PIMCO Dynamic Income Fund (PDI).

Before we get into specifics on this CEF, we need to ask ourselves if we should trust Ivascyn. After all, he could be “talking his book,” telling us to buy bonds because he’s a bond manager.

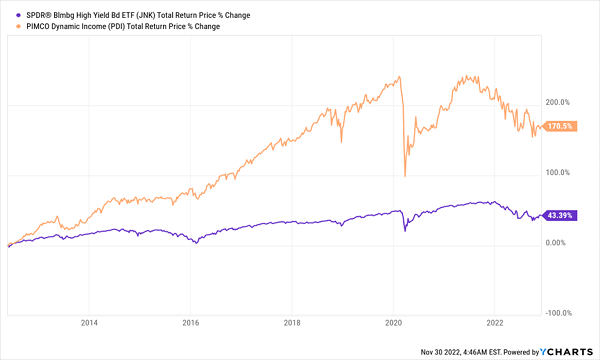

On the surface, this sounds like a fair criticism, but the truth is more complicated. Ivascyn, and indeed PIMCO, have been bearish on bonds in the past and made a lot of money in down years for the asset class. Take PDI’s performance in 2015, shown in blue below, for example.

Bonds Lose, PIMCO Wins

Back then, high-yield corporate bonds, shown in orange by the performance of the benchmark SPDR Bloomberg Barclays High-Yield Bond ETF (JNK), ended the year down, which was a drag on some of PIMCO’s more passively managed bond funds. The reason for this drag is familiar to us today: higher interest rates and fears of inflation had first-level investors trimming their bond positions.

But in funds where PIMCO management could be selective, going long on good-quality bonds and short on lesser-quality issues, they posted strong returns. That includes PDI, which even beat the stock market back then, as we can see in the chart above, and now has many more years of strong performance under its belt.

How Inflation Favors PIMCO’s Bond Strategy

Given that bond prices tend to fall as yields rise, many retail investors just flee the asset class when the Fed hikes rates.

PIMCO is more sophisticated. Since rising rates cause long-term bonds to fall further than short-term bonds, a strategy of short-selling long-term bonds and outright buying short-term bonds can result in massive profits when rates are rising, and there are a lot of opportunities to find mispriced bonds in the $127-trillion bond market. PDI has done a great job finding them and, in turn, providing a huge income stream to investors.

If you think PDI’s yield seems unsustainable, I fully understand; back in 2015, when I was bullish on PDI, many said the same. But not only have PDI’s payouts not been cut, they’ve actually risen since.

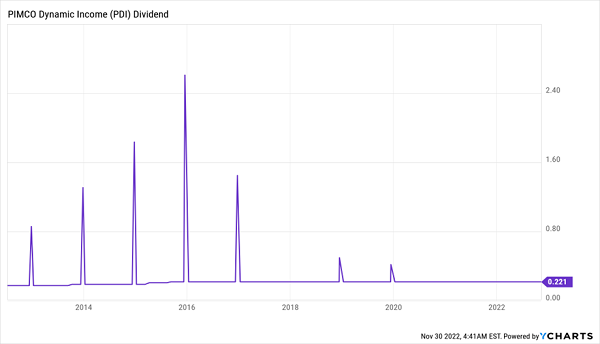

A 13.4% Payout That Grows (and Drops Special Dividends on the Regular)

There are, of course, the hikes to the regular payouts to enjoy, but note all of those special dividends paid out when the Fed was keeping interest rates low in the early 2010s.

PDI wasn’t directly profiting on the Fed’s low rates (which lowered the yields on the fund’s holdings, making them unattractive to first-level investors); it was profiting because less-sophisticated investors fled the bond market, providing tons of profitable opportunities for funds like PDI. And profit they did. As you can see below, PDI (in orange) far outpaced benchmark JNK (in purple).

PDI Laps Its Benchmark

PDI’s “Hidden” Discount

There’s another angle we shouldn’t overlook, either: the fund’s attractive valuation: as of this writing, PDI trades at a 6.7% premium to net asset value (or the value of the bonds in its portfolio). That doesn’t sound like much of a deal until you consider two things:

- Due to the strength of the PIMCO name, backed by years of strong performance, the company’s funds almost always trade at premiums, often well into double digits, and …

- PDI’s 6.7% premium is actually something of a discount in disguise, falling well below the 10.3% average premium the fund has sported in the last five years.

That gives us an additional opportunity for price gains, to go along with PDI’s rich 13.4% dividend.

This Powerful CEF Portfolio Is Backed By Bonds—and Yields 9.1%

Our bond-buying opportunity isn’t just limited to PDI. In fact, the PIMCO favorite isn’t even among my top bond-CEF picks today.

That honor goes to a 10%-payer that, unlike PDI, trades at a healthy discount to NAV. Plus, this fund comes from an even bigger bond buyer with even deeper research resources.

It shows in this fund’s performance: it’s notched a 308% return in its lifespan. I’m expecting strong upside from in the coming months, as more people are lured by the attractive yields available in the bond market.

This pick is part of a 5-CEF portfolio I’ve built for 2023 consisting of funds holding top bonds, stocks, real estate investment trusts (REITs) and the most oversold tech plays out there.

All of these assets are overlooked—and I’m pegging all of them for 20%+ price upside in 2023, to go along with this portfolio’s 9.1% average dividend.

Now is the time to buy these 5 reliable income plays. Click here and I’ll reveal how you can get their names, tickers, best-buy prices, current yields and the rest of my research in a free Special Report.