The market is soaring to record highs, making all stocks too expensive to buy, right? Wrong. While exuberance is in the air, there are still a few overlooked gems paying dividends nearly 4% with strong growth potential.

We can easily build a portfolio of four stocks with overall strong revenue growth, growing dividends and a 3.9% average portfolio yield. That yield will only grow in the coming years thanks to each company’s moat, making this a durable portfolio for an IRA or for investors eyeing retirement in the next decade or beyond.

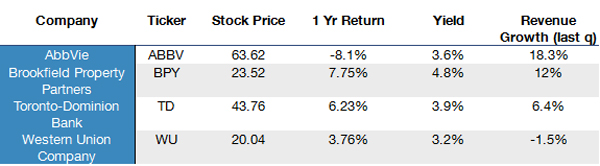

So what’s in it? We’ve got four names: AbbVie (ABBV), Brookfield Property Partners (BPY), Toronto-Dominion Bank (TD) and Western Union Company (WU) – names that have on average gone up just 2.4% in the last year, with none of them at 52-week highs (although some are close). At a glance, our portfolio looks like this:

Note that each of these companies is a large-cap stock with several years of dividend payout history. Why these stocks? Let’s go through them one by one.

Underappreciated Innovation

AbbVie recently received FDA approval for a Phase-2 study of a new treatment for a highly aggressive brain tumor that children sometimes develop. The company has many popular drugs, such as Humira, Biaxin, Survanta and Vicodin.

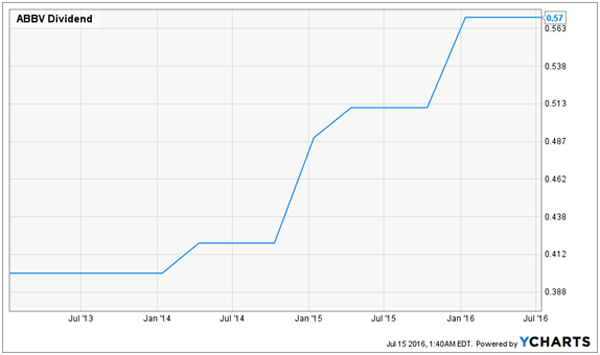

The company’s years of proven research and development of drugs has made it popular in the past, but right now the stock is in a slump. There’s no real good reason for this. Last year, revenues grew 14.6% and operating margins soared from 17% to 33%. The company also hiked its dividend at the beginning of this year—the fourth dividend hike in 5 years:

If AbbVie sustains its 7.3% annualized dividend growth, the company’s dividend will be $1.15 in a decade. At the stock’s current price, that will be a 7.3% annual dividend yield. Since AbbVie’s product pipeline remains strong, it is a great candidate for buy-and-hold retiree investors today.

Durable Retail Presence

Brookfield Property Partners is a REIT that specializes in regional shopping malls. Almost immediately, many investors will recoil with horror for all the same reasons: e-commerce is killing retail, malls are dead now that teenagers have Snapchat, and so on. But this isn’t quite accurate. BPY has been extremely selective and strategic in choosing its properties and geographical footprint in high yielding areas that are resisting these headline-grabbing trends. The fact is that, yes, the internet is booming and teens are glued to their phones, but people are still going to some malls in some parts of the country.

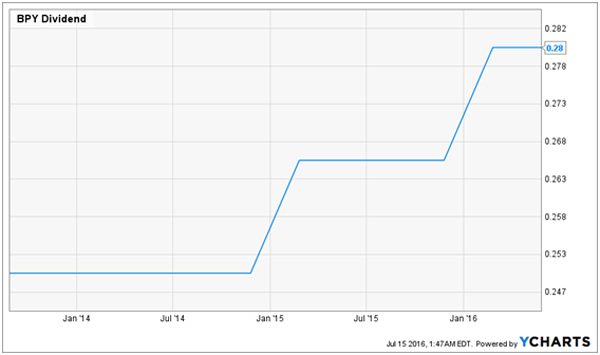

This is why Brookfield’s funds from operations went up 13.6% from a year ago over the last fiscal year, causing dividend coverage to remain a strong 106%. That has also helped the company grow dividends since its IPO in 2013:

Since inception, Brookfield has grown its dividend by an annualized 3.7%. In a decade, our dividends will be 40.3 cents, giving us a 6.9% yield.

A Competitive Bank

Many Americans don’t know TD Bank is Canadian, but Toronto-Dominion’s quiet emergence in America as a popular retail bank in urban areas is a testament to the company’s ability to expand beyond its borders. Revenue growth is less impressive with this one, at just mid-single digits on a year-over-year basis, but the important metric here is dividends, which have been growing sharply over the last few years (while dividend coverage from cash flow remains solid):

There is just one problem with TD’s dividend payments, as the chart above shows: currency fluctuations are a real risk both to investors and the company itself. As the company accounts in Canadian dollars, the hit to oil in 2014 hit the currency, and thus TD’s dividend as seen in U.S. dollars.

That’s not really a problem over the long term, however, as I’m projecting a 5.7% dividend growth rate over 5 years—and that’s artificially low across TD’s history, due to the oil issue. If we still keep this as a conservative expectation for the next decade, though, in 10 years our dividend yield will be 6.8% of today’s prices. Oil or not, this aggressive high-growth bank is a great pick.

Cashing in on Emerging Markets with Less Risk

Emerging markets are a great growth driver, but low commodity prices hurt them terribly. Then there are issues of corruption, rule of law, unreliable accounting practices (just ask anyone who’s bought Chinese stocks in the last decade about that). Emerging market stocks are not for everyone. There’s a way to get into this market growth without the risk, however, with an old familiar American name: Western Union.

Some first-level types see WU as a fossil, quickly replaced by Paypal (PYPL), Square (SQ) and other high-tech interrupters. But Western Union remains the gold standard for remittance payments in much of the world, and several developing countries have Western Union branches even in the most remote villages where percentage income growth is at its strongest around the world.

Still, Western Union is not showing revenue growth, with income actually falling 2.2% last fiscal year. That doesn’t change the fact that WU remains a highly profitable company with a wide moat in many parts of the world. Operating margins have remained around 20% for the last 3 years, which is why WU decided to buy over $1 billion in shares last year.

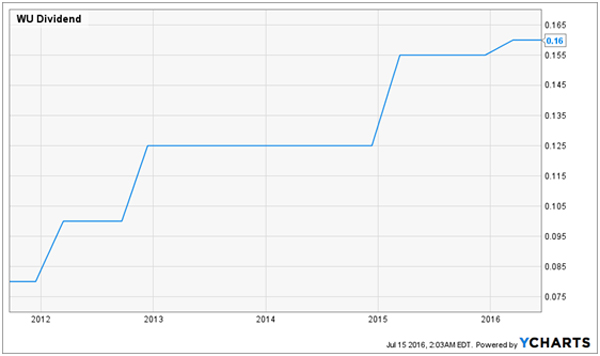

On top of that, WU has one of the highest dividend growth rates out there:

Doubling its payouts in the last 5 years, WU has rewarded shareholders who have stayed with the company despite the technological innovation narrative that drove exuberance in Paypal and Square over the last few years. With a 14.9% dividend growth rate over the last half-decade, WU holders from 5 years ago saw their yield-on-cost soar from 1.6% to 3.2%. Since the stock price is virtually unchanged since then, you can buy WU today and still capture that same yield.

If Western Union continues this pace of dividend payments, we will enjoy a 12.8% dividend yield in 10 years based on the stock’s current price. That seems unreal, absurd, extreme—but it’s there in the numbers. The big question for investors is whether WU can maintain this increase in payouts with flat revenues, which is why the market hasn’t capitalized on the dividend growth yet.

I believe WU can. The company’s buyback plan accounts for over 12% of shares outstanding. After that, the company will still have plenty of net income left over to continue buying back shares if they can’t grow revenues. That’s the beauty of a cash generating operation: even if you’re dead in the water, you’re still rich.

And 3 Big 8%+ Yields Available Today

Yes, the market is at new highs, and many stocks are expensive. Dividend growth investors have essentially been stuck waiting for the market to correct before buying more, but there’s no reason to wait. There are four great dividend growth stocks at reasonable prices right now with tremendous growth potential. It just takes a bit of patience to see those dividend yields really soar.

If you don’t have the patience (or time) to wait, there are some high yield dividend stocks and funds that are still affordably priced and offer a high rate of income today. I’m talking about 8%, 8.4% and 11% annual dividends with up to 15% additional price upside. Click here and I’ll show you what these income investments are along with the names, tickers and buy prices for my three favorites.