Here’s the thing about high-yield closed-end funds (CEFs): sometimes a CEF will seem to have all the earmarks of a terrific investment: high (and monthly) dividends, reasonable fees and reputable management. But it’ll still come up short.

We, of course, love CEFs and see them as the critical pieces of our income portfolios. The portfolio of my CEF Insider service, for example, holds plenty of top-quality buys and yields 9% as I write this.

But when picking these funds, we need to make sure we don’t let a big name, high yield or so-called “low” fees dominate our thinking. We also need to look deeper, at factors like past performance and even management’s track record with its other funds.

Today we’re going to spotlight three CEFs, in particular, we want to steer clear of. All three look like good investments on the surface, but they just haven’t panned out for investors.

Laggard CEF No. 1: BlackRock Core Bond Trust (BHK)

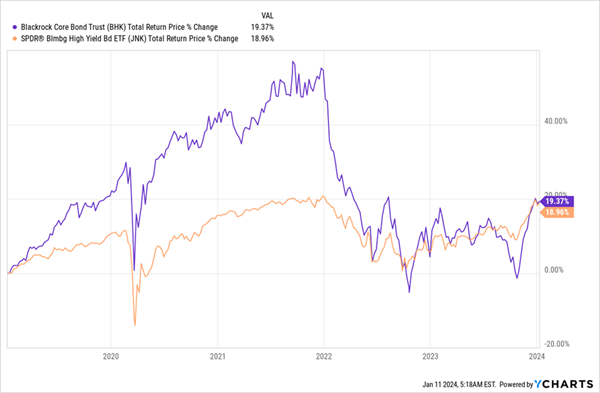

First up is BHK, an 8.2%-yielder whose straightforward name and dominant management firm—BlackRock invests over $10 trillion for investors such as large pension funds and governments—would seem to suggest a strong corporate-bond fund.

But look back over the last five years and you’ll see a meager return that’s only managed to track the high-yield benchmark SPDR Bloomberg High-Yield Bond ETF (JNK).

BHK Barely Budges

That’s disappointing because the vast majority (over 70%) of corporate-bond CEFs have outperformed JNK in that span. That’s because, in bonds, actively managed CEFs have a big edge: since the bond market is relatively small, well-connected managers often get tipped off when attractive new bond issues come out.

That’s something an ETF like JNK simply can’t take advantage of.

But BHK’s management hasn’t gotten those calls, apparently, as its 3.6% annualized total return provided barely any profits for investors. To make matters worse, BHK trades at around par to its NAV (meaning its market price is aligned with its net asset value, or the value of its holdings).

With CEFs, we always aim to buy at a discount. But with BHK, we’re getting the worst of both worlds: poor performance and an overvalued price. Neither bodes well for future gains.

Laggard CEF No. 2: PIMCO Municipal Income Fund (PMF)

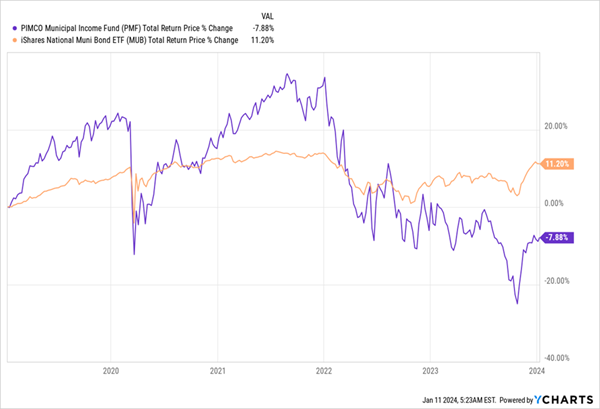

BHK’s performance still tops that of municipal-bond fund PMF, a 5.4%-yielder that has actually lost money over the last five years, even with dividends included. It’s also underperformed its index—in this case the iShares Municipal Bond ETF (MUB).

PMF Loses Money Despite Holding Government-Backed “Munis”

That’s particularly disheartening in light of the fund’s fee of 1.67% of assets. That’s not out of line for a muni-bond CEF—and to be sure, we don’t mind paying higher fees if they result in strong gains. But when we could have bought the ETF and paid a mere 0.05% of assets, PMF’s higher take just doesn’t make sense.

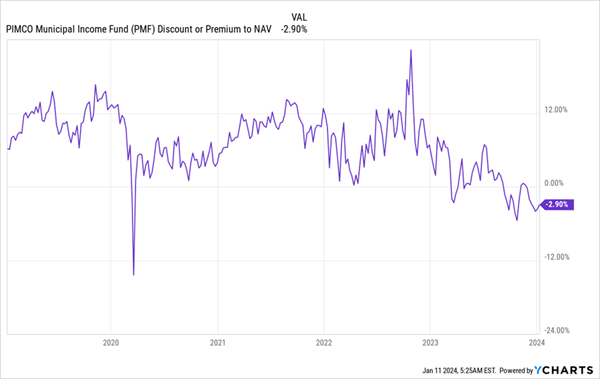

This woeful performance is especially surprising from PIMCO, which is known as one of the best bond-investment firms out there (its founder, Bill Gross, literally invented bond trading in the 1970s). But this chart tells the story behind PMF’s decline:

PMF’s Performance: A Classic Case of “Buy High, Sell Low”

As you can see, PMF traded at a premium to NAV five years ago that has fallen to a near-3% discount, pulling PMF’s price down with it. That’s the main driver of the decline here.

So why aren’t we interested in PMF now, with the fund trading at a discount? Simple: it’s cut its dividend twice in just the last five years, so it’s not even a good buy for reliable income.

Laggard CEF No. 3: MFS Intermediate Income Fund (MIN)

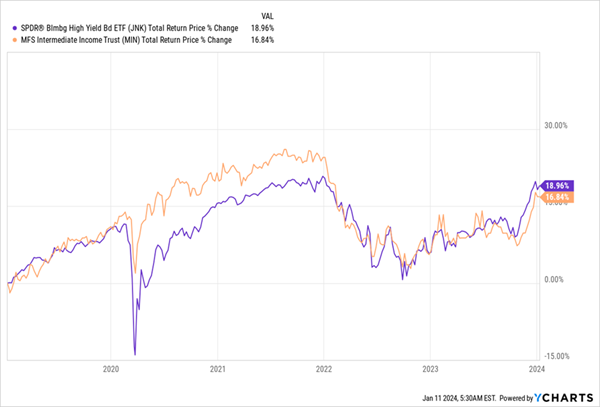

I’m less surprised that the 8.9%-yielding MFS Intermediate Income Fund (MIN) has been a poor performer, although many people might at first glance assume it would be a winner. After all, MIN is well diversified (it holds 194 bonds) and has bought those bonds at an average 7.3% discount to their issuance price.

Plus, MIN’s fees are just 0.69% of assets, less than half the 2.36% average across all CEFs. Still, MIN has underperformed JNK in the last five years, so it’s done worse than BHK, our first laggard CEF, even though BHK has a much higher fee of 1.95%.

MIN’s Weak Returns

It’s worth pointing out that MIN’s dividend has fallen 28% in the last five years, too, so you’re getting declining income and meager returns with this fund.

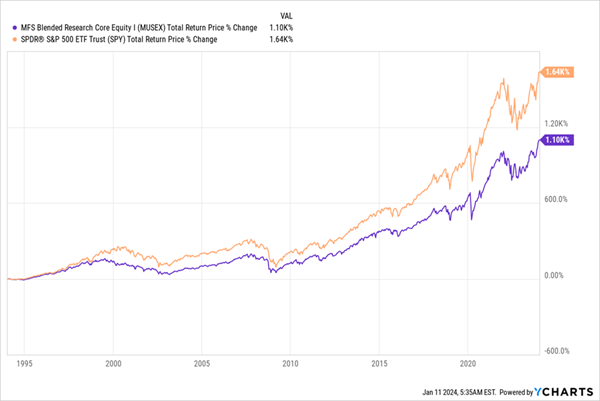

What happened? The fact is, MFS Investment Management (the fund’s sponsor) doesn’t have the best history with most of its funds. Take, for instance, the Blended Research Core Equity Fund (MUSEX), whose inception date was back in 1994. It’s designed to outperform the S&P 500, but in reality, it’s done much worse:

MUSEX Fails in Its Mission

MFS, which set up shop in Boston 100 years ago, commands a lot of loyalty in the Boston area, which helps it attract investors. A long history is an important thing to consider when looking for an investment, of course, but it’s not the only thing—and it doesn’t shield a firm from underperformance, as MIN and MUSEX demonstrate.

These 5 Cheap (for now!) 10.2% Payers Are My Top Buys for January

Now that we’ve talked about what we’re selling (or avoiding!) this year, let’s dive into the high-paying CEFs we’re going to buy right now—this month!

I’ve got you covered here, with a FREE Special Report I’ve compiled revealing 5 of my best CEF picks for the new year. These funds yield 10.2% on average, plus I’m calling for 20%+ price upside as their discounts vanish—and their share prices gain altitude.

I’ve written a full backgrounder on CEFs—and why you never hear about them in the financial press. I urge you to click right here to check it out. It’ll also give you the opportunity to download a FREE Special Report detailing all 5 of these bargain-priced 10.2%-paying funds so you can take advantage of them now, while they’re still cheap.