Are you worried that you’re going to outlive your money? It’s a fair concern with interest rates low and heading lower.

To put it bluntly, many well-off retirees are at serious risk of having to pick up a “side hustle” to avoid dying broke. Passive income in the popular retirement “go-tos” is simply no help today, as the average S&P 500 stock pays a skimpy 1.9% now. Ten-year Treasuries? Even worse, at just 1.5%.

So unless you’ve got $2.1 million laying around to invest in the typical blue chip stock—enough to get you a $40,000 annual dividend stream—you’ll likely have to sell some of your stocks to supplement your dividend income.

That’s a very dangerous course right now, because of this:

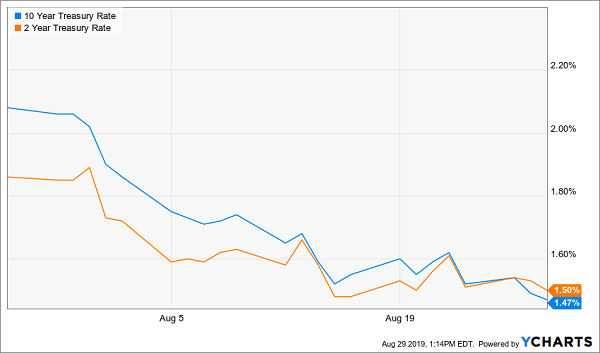

“Recession Alert” Turns Red

We’re looking at the yield on the 2-year Treasury note (in orange) and the yield on the 10-year (blue). When these yields “invert”—as they are now—they’re the canary in the coal mine: this setup has predicted the last seven recessions.

Millions of Retirees About to Get Hit

This indicator is putting millions of retirees on notice. But many will ignore it because they follow a strategy their adviser says is safe, but is, in fact, anything but.

That’s the “4% rule.” You know the one: where you withdraw up to 4% of your portfolio a year to supplement your dividend income.

Sounds reasonable, right? Well, I hope you haven’t fallen into this trap. Because the 4% fiasco can only magnify your losses (and crush your income) when you hit a patch like this:

The 4% Rule Slams Into Reality

This is a snapshot of Apple (AAPL) stock’s 33% plunge during the late 2018 correction, which was much worse than the 20% fall in the market as a whole.

If you were following the 4% rule, you were forced to withdraw money at exactly the wrong time. Apple’s dividend was fine (in fact, the company announced a big hike a few months before the meltdown). But you still needed to sell shares for more income.

Remember the benefits of dollar-cost averaging that built your retirement portfolio? This is the same, but in reverse! You’re selling more shares when prices are low—which hurts your income stream even more—and fewer when prices are high.

It’s a “retirement death spiral” with one outcome: outliving your money!

The Solution: “Pullback-Proof” Dividends

Instead of Wall Street’s flawed 4% rule, we’re going to transition your nest egg into what I call “pullback-proof” dividends. These stout dividend payers have two critical strengths that protect and grow your savings no matter what:

- High, safe dividends of 6.4% and up, so you don’t have to worry about selling into a downturn—you can just pay your bills with your dividend cash.

- Low volatility—Measured through a stock’s “beta” rating—or its movements in relation to the S&P 500 (more on this shortly).

Let’s dive into two dividends that tick these boxes. I’m zeroing in on these two because between them, they give you a ton of diversification, with real estate investment trusts (REITs), blue chip stocks and high-yielding preferred stocks.

Pick No. 1: Tap This “Investor Blind Spot” for Big Gains (and 6.5% Dividends)

Like the proverbial generals fighting the last war, many folks simply won’t touch real estate, because it triggered the ’08/’09 crisis.

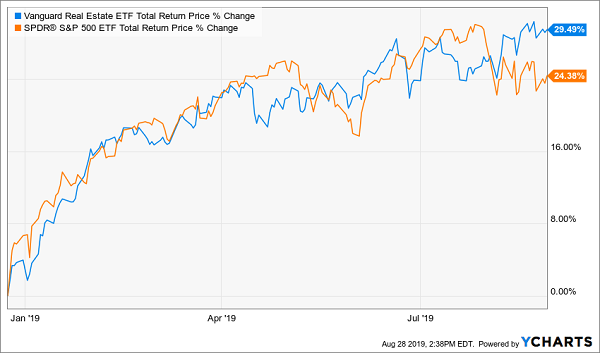

That’s too bad, because they’re missing out on one of the steadiest, highest-yielding corners of the market. Right now, the benchmark Vanguard Real Estate ETF (VNQ), yields 3.3%, nearly double the typical S&P 500 name.

What’s more, in the late-2018 crash, REITs fell half as much as stocks. And because of REITs’ higher dividends, owners of these stocks had far less need to sell into the downturn:

REITs Weather the Storm Better Than Stocks …

And Rebound Faster …

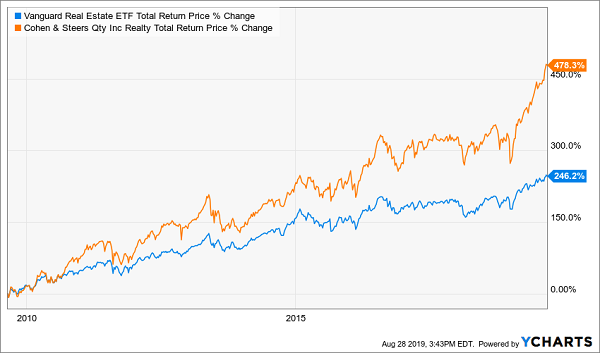

You can swiftly double VNQ’s income stream with our first pick, the Cohen & Steers Quality Income Realty Fund (RQI), which boasts industry-leading REITs like cell-tower owner American Tower (AMT), warehouse operator Prologis (PLD) and healthcare landlord Welltower (WELL).

This fund’s secret weapon is its management team, which boast 75 years of experience between them. They’ve powered RQI’s portfolio (measured by its net asset value, or NAV) to a 9.8% annualized return since inception in 2002, topping the 8.7% returned by the other REIT CEFs.

Just look at what they’ve done to VNQ in the last decade:

RQI’s Curb Appeal

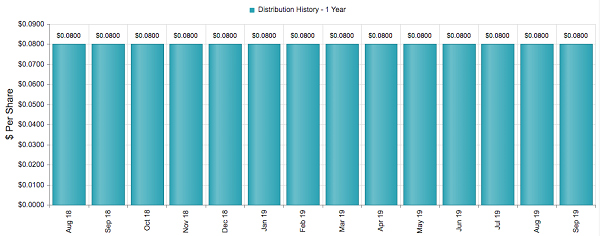

And you can forget about having to sell into a downturn with this fund, because most of its monster return comes in cash, thanks to its 6.5% dividend, which drops into your account monthly—right in line with your bills:

A Rare Rock-Solid Monthly Payout

Source: CEF Connect

Before we move on, I’ll leave you with this: RQI is built for a pullback, boasting a beta rating of just 0.72, making it 28% less volatile than the S&P 500.

Pick No. 2: A 6.4%-Yielder That Shrugs When Markets Panic

Let’s add more ballast to our portfolio with two other corners of the market that are perfect for times like these: utilities and preferred stocks.

But we’re not going to do it through ETFs or by buying these stocks directly.

That’s partly because preferred stocks are tough for individual investors to access, and the ETF options pay less than the CEF I’ll show you shortly: 3% for the Utilities Select SPDR ETF (XLU) and 5.6% for the iShares Preferred & Income Securities ETF (PFF).

I don’t know why you’d mess around with these when you could buy the John Hancock Tax-Advantaged Income Fund (HTD), which pays a 6.4% dividend—every month, no less—and pumps out big special dividends on the regular.

A Steady Monthly Payout, With a Year-End “Bonus”

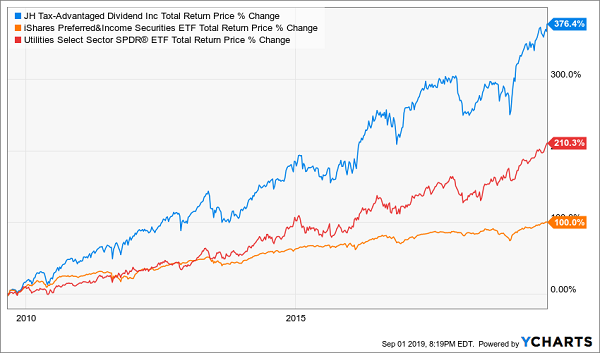

Like RQI, HTD has dominated its benchmarks (PFF and XLU) in the last decade, with more of its return coming in cash, thanks to its outsized dividend:

“Boring” Fund Powers Up

Which brings me to its legendary stability: with a beta rating of 0.54, this one is half as volatile as the overall market.

With our “recession indicator” flashing red, it won’t be long before HTD’s low volatility, high dividend and history of big special payouts prompt the mainstream crowd to bid the fund’s price away from us. That makes now the time to buy in.

5 Even Better “Pullback-Proof” Dividends (Massive Payouts Up to 10.4%)

HTD and RQI are both smart buys for today’s whipsawing market. But neither one made it into my just-released 5-stock “Pullback-Proof Portfolio.”

Why? Even at 6.5%, their yields still aren’t high enough for me! My 5 “pullback-proof” plays pay you much more, offering you:

- A rock-solid (and growing) 8.2% cash dividend, and …

- Steady 7% to 15% yearly price upside while you collect these rich payouts.

And remember, 8.2% is just the average yield I’m talking about here. One of these titans pays a steady 10.4%!

Think about that for a second: buy this incredible stock now and every single year, more than 10% of your original buy boomerangs straight back to you in cash. Fast-forward a decade, and you’ve piled up enough dividends to match your entire investment.

Everything else is gravy!

This is the kind of income (and safety) this powerful collection of investments offers. And I’m ready to spill the beans on all 5 of my “pullback-proof” buys now.

Click here and I’ll give you my complete research on each one: names, tickers, buy-under prices and a thorough look at how each of these 5 urgent buys makes its money. In short, absolutely everything you need to know before you buy.

But you must act now: the latest volatility has already started to drive these 5 buys’ share prices higher (and their discounts lower). I expect that to continue as more safety (and income-) obsessed investors pile in. Don’t miss out!