One of the best characteristics about dividends is they usually offer a consistent, preferably growing stream of income. However, investors can easily fall into the trap of becoming complacent that future payments will continue to flow in, even when the business isn’t generating enough cash to fund the dividend.

The higher the yield being offered generally means the riskier the dividend is and sometimes losses can outweigh the expected income. For example, Dynagas LNG Partners (DLNG) cut its 16% yield back in April and shares are down 25% since.

With government bonds paying around 2% to 3%, dividends above 10% need to be scrutinized closely and I’ve identified two that are in danger of disappearing.

Dangerous Dividend No. 1 : Poor Earnings Quality

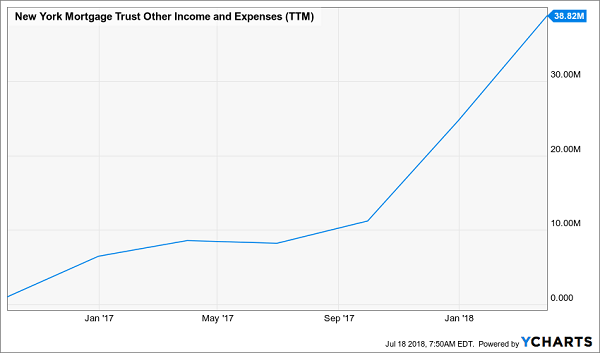

New York Mortgage Trust (NYMT) is a real estate investment trust (REIT) that invests in various types of residential mortgage securities. The company earned $0.20 a share in the first quarter, which is equal to its dividend, but a closer look at the results reveals a more troubling outlook for investors interested in the stock’s 13% dividend yield.

Just a nickel of the reported profit last quarter was from traditional spread income, something that is likely to face continued pressure from further interest rate hikes by the Fed and a flatter yield curve, as mortgage investors want to borrow at low rates and lend at high ones.

The majority of New York Mortgage’s earnings last quarter relied on one-time gains, such as interest rate hedges and the sale of distressed loans. This “other income” is difficult to predict from one quarter to the next, which is not the type of consistency that dividend investors want to see.

No matter how the company is earning its money, consensus earnings expectations are that annual profit will fall short of the $0.80 dividend for each of the next three years, which suggests the current payout is not sustainable.

Dangerous Dividend No. 2: Growing Debt Level

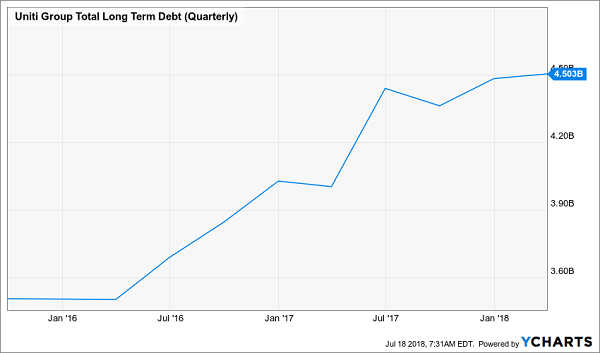

Uniti (UNIT) is a REIT that invests in the fiber and towers that helps move both traditional and mobile Internet traffic. The company was spun out from regional telecom carrier Windstream (WIN) a few years back, but the former parent still accounts for two-thirds of Uniti’s revenue.

Windstream had its own dividend problems in 2017, eliminated its payout entirely and there are signs that Uniti’s own 11% yield could also face the chopping block. Last month, Moody’s lowered its credit rating on the company to Caa1, which means they’re as many steps away from default as they are from achieving an investment grade rating. When push comes to shove, bondholders will receive interest payments before shareholders are paid dividends.

Management’s 2018 funds from operations (FFO) guidance is about $2.20 a share, which is not enough to cover the quarterly dividend of $0.60. When Uniti adjusts FFO for items such as the amortization of deferred financing costs and debt discounts, it has been sufficient to fund the dividend, but not with enough leeway for investors to be confident given the rising debt load.

Don’t chase these high dividend yields where the funding appears unsustainable. There are better bargains to be had, for secure 7% to 8% yields with upside and monthly payouts to boot.

Like These Plays: The 8 Best 8% Dividends with Big Upside to Buy Today

Most Wall Street spreadsheet jockeys say we investors can’t have both the income and safety of bonds and the upside of stocks. We have to choose, or allocate, or whatever.

They’re wrong. They don’t realize that the nine bond funds in our Contrarian Income Report portfolio have delivered average annualized returns of 23.9% (including dividends)!

Our three top picks today are poised to continue the tradition. These funds are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right. Their principal is more than 100% intact thanks to price gains like these!

Which means principal is actually 110% intact after year 1, and so on.

To do this, we seek out closed-end funds that:

- Pay 8% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

And we talk to management, because online research isn’t enough. We also track insider buying to make sure these guys have real skin in the game.

Today we like three “blue chip” closed-end funds in particular. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.5%, 8.7% and even 8.9% dividends.

Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and we’ll explain more about our no withdrawal approach – along with details on our three favorite closed-end funds for 8.5%, 8.7% and 8.9% yields.