Nobody’s perfect. And in 2022, it’s particularly hard to pretend that you never make a losing trade as the market has been incredibly volatile through no fault of our own.

That said, there’s the old saying that the definition of insanity is doing something over and over but expecting different results. So if you have a habit of making bad trades, maybe the bigger problem isn’t the stock market… but your strategy.

One particularly risky strategy that I see some income investors cling to is the notion of placing a priority on yield above everything else. And like Captain Renault, these investors always seem to be shocked – shocked! – when these high-yield trades inevitably fall apart.

Let’s start with some basic math. Dividend yield is calculated by dividing the annual payouts to shareholders by the current share price. One way for a stock’s yield to double is (obviously) for its payouts to double in kind. However, the easier and much more common way for a stock to double its yield is simply to maintain or even slightly reduce dividends while its share price falls off a cliff.

In 2022, many investors who chase yield are picking stocks in this latter camp. And that’s dangerous, because stocks that slump 30%, 40% or more often do so for very good reasons.

Instead, investors should be looking for quality as well as quantity in their dividends. They should look for long-term dividend growth, even if it means passing on stocks with artificially inflated yields well into double digits.

It’s not an easy balancing act in any market, and that’s particularly true in the challenging environment we’re facing. So let me tell you a story of two popular dividend stocks—one to avoid, and one to buy—as an illustration of what you should look for right now.

Dividend Stock to Sell: Kraft Heinz

By all accounts The Kraft Heinz Company (KHC) is killing it right now. As I write, shares are up 8% since Jan. 1 even as the S&P 500 has lost 18% in the same period. The stock yields 4.1%, which is almost three times that of the typical stock in that large cap benchmark at present. And with a powerful consumer staples portfolio including Heinz Ketchup and Kraft Mac ‘n Cheese, it’s highly unlikely we’ll see disruptions to this stock even if consumers cut back on other purchases amid red-hot inflation.

But here’s my advice: Avoid KHC like the plague. And if you own it, take the money and run.

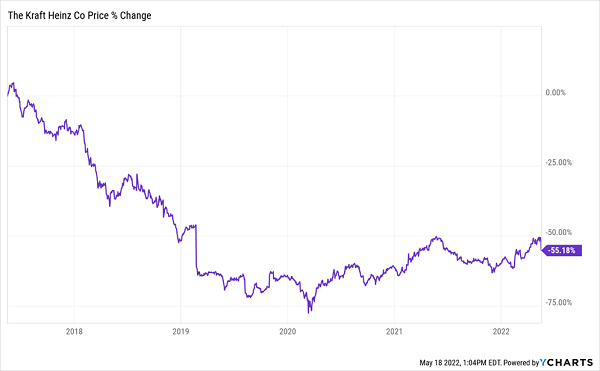

Here’s why: Earnings per share are actually forecast to DECLINE in FY2022. And while the yield is nice, that’s in part because shares flopped from a high above $90 back in 2017 to roughly half that value at present. Just look at a five-year chart and it’s clear that the short-term uptrend is hardly noticeable amid the broader struggles.

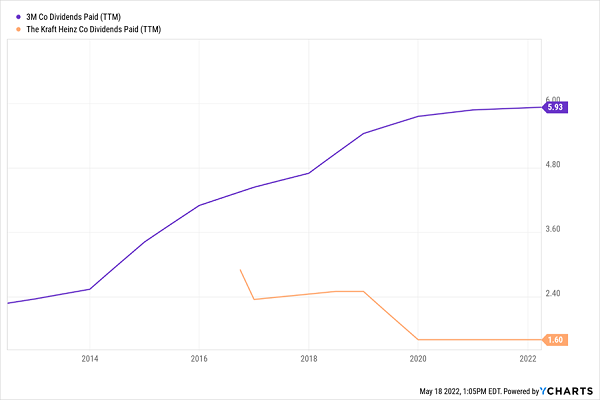

Kraft Heinz is still fighting to pay down more than $20 billion in debt remaining from its bloated 2015 merger, which will certainly impact ongoing performance. And let’s not forget that its dividend hasn’t budged from 2019 when it slashed payouts from 62.5 cents to just 40 cents a share.

Sure, KHC was in the right place for the “risk off” rally this year. But does any of this sound like a quality long-term investment you can believe in for long-term income?

Dividend Stock to Buy: 3M

Let’s instead look at a higher quality dividend stock – even if it’s one that hasn’t done particularly well in 2022. That stock is 3M (MMM).

In February, 3M increased its dividend payout for the 64th consecutive year running. That spans the pandemic, the financial crisis, the dot-com crash and a host of other crises. And the current yield is about 4.0%.

What’s more, 3M’s payout of $1.49 per quarter is only about half of this year’s projected earnings so there’s a good chance of continued increases. That means buy-and-hold investors will only get bigger paydays down the road – in stark contrast to a stock like KHC that has had to cut back just to get by.

Furthermore, thanks to improving margins MMM is seeing high single-digit earnings growth projections both this year and next as it continues to operate efficiently and at scale. This global chemicals giant is valued at more that $80 billion, with a host of innovative products ranging from Command hangars and Post-It notes for consumers to specialty coatings and adhesives used in healthcare, industrial and electronics applications.

Sure, it has taken some lumps including a lawsuit over defective earplugs and normalizing of operations after pandemic-driven demand for its N95 respirators has abated. But this is a dividend stock with staying power, and one that’s incredibly attractive at current valuations. Its forward price-to-earnings ratio is less than 14, while Kraft Heinz is above 16 and the broader S&P 500 is averaging a reading above 17 even after recent declines.

3M isn’t going to win any prizes as the most popular stock on Wall Street right now. But for long-term dividend investors, this hidden gem is just what the doctor ordered.

These “Hidden Yields” are the Best Long-Term Strategy

Some dividend stocks surge thanks to short-term trends, and that’s great if you happen to be invested already. However, chasing these stocks while they are fashionable can often result in heartache as the fair-weather traders abandon these stocks once the winds change.

There’s a real risk of this happening to a stock like KHC.

On the other hand, stocks like 3M can provide investors strong yield now and the hopes for even bigger paydays in the future. This is because they offer sometimes boring but incredibly reliable operations that make them worth hanging on to.

So don’t chase short-term outperformance at the cost of a safe and secure retirement. And don’t chase the usual suspects just because they are making headlines this week.

Instead, look ahead and identify stocks that are likely to grow their dividends and deliver long-term income.

At Contrarian Outlook, our Hidden Yields service provides just such an approach. Our goal is to deliver you 15% every year – every year – for the rest of your life.

The strategy is simple: find companies consistently raising their dividends at solid rates PLUS consistently buying back their own shares. Companies like 3M, which has returned over $14 billion to shareholders through dividends and share repurchase over the last three years alone!

If you are looking for consistent, volatility-proof returns then look no further.